Updated on June 4, 2026

Toronto attracts newcomers from across the globe with the promise of robust job opportunities and world-class cultural events. But the cost of living in Toronto can be a major hurdle for those looking to live in the city.

This article digs into what the real cost of living in Toronto looks like, by going through the budgets of (fictional) Torontonians. We dig into finances for individuals and families, and then finish with some tips for saving money while living in Toronto. Let’s go!

Toronto Cost of Living at a Glance

The cost of living in Toronto can vary significantly depending on your lifestyle, housing choices, household size, and the neighbourhood you live in. Rent prices, transportation costs, and day-to-day expenses can differ substantially between downtown Toronto and surrounding areas such as North York, Scarborough, Etobicoke, or Mississauga.

The estimates below represent a typical family of three living in a mid-sized apartment in a central Toronto neighbourhood. These figures should be viewed as broad ranges rather than fixed costs, as every household has different priorities, spending habits, and housing needs.

Use this table as a starting point to understand what monthly expenses may look like before creating a personalized budget based on your own circumstances.

| Expense Category | Estimated Monthly Cost |

|---|---|

| Rent | $2,650 – $3,850 |

| Utilities | $130 – $350 |

| Phone & Internet | $146 – $420 |

| Groceries | $737 – $1,106 |

| Transportation | $320 – $1,000 |

| Miscellaneous Expenses* | $557 – $836 |

| Total Monthly Expenses | $4,540 – $7,562 |

*Miscellaneous expenses include health and fitness, entertainment, banking fees, and other everyday costs.

While these estimates provide a useful benchmark, your actual costs may be higher or lower depending on where you live and the lifestyle you choose. To get a more accurate estimate based on your household size and spending habits, try the Moving2Canada Budget Calculator and build a personalized cost-of-living budget for Toronto.

What are the monthly expenses in Toronto to consider?

Here is the list of the most common smaller costs that add up quickly:

- Mobile phone bills

- Insurance (House insurance, car insurance, Private health insurance)

- Winter services or tools (Snow removal, winter tires, etc)

- winter-appropriate clothing

- summer-appropriate clothing

- child-related expenses

- fees related to building up a Canadian credit history

- Fitness (Gym subscription, equipment and clothing)

What's the real cost of living in Canada? Find out by city

What Are Transport Costs in Toronto?

Transportation costs in Toronto depend largely on where you live, where you work, and whether you rely on public transit, drive your own vehicle, or use a combination of both. While many residents living in central neighbourhoods can comfortably get around using public transportation, those commuting from the Greater Toronto Area (GTA) often face higher transportation expenses.

Toronto’s public transit system, operated by the Toronto Transit Commission (TTC), includes buses, streetcars, and subway lines that connect most parts of the city. For many newcomers, public transit is the most affordable transportation option, especially when compared to the cost of owning a car.

The table below provides estimated transportation costs in Toronto as of 2026:

| Transportation Expense | Estimated Cost |

|---|---|

| TTC single adult fare (PRESTO, debit, or credit) | $3.30 per ride |

| TTC monthly pass (until August 2026) | $156 per month |

| Public transit costs (family of three) | $320 – $470 per month |

| Car ownership (fuel, insurance, maintenance, parking) | $650 – $1,000+ per month |

| Estimated Total Transportation Costs | $320 – $1,000 per month |

Cost of Buying a Car in Toronto

If you live in Toronto and are considering buying a car, but your household income is less than $85,000, money will likely be tight. While the payment plan might seem affordable (you can find plans as low as $500 per month ), remember that adding insurance, gas, storage, parking, parking fines, and maintenance quickly add to the costs of owning a car.

If you’re a newcomer and considering buying a car, it’s worthwhile considering whether rentals could fill that need. Car subscriptions, through companies like our partner, Roam, allow you greater flexibility when it comes to ongoing transport costs without sacrificing on convenience or the quality of your vehicle.

Plus, the Moving2Canada community enjoys $50 off weekly plans, $100 off monthly plans, and $150 off long-term plans. Use coupon code M2CR25 at checkout.

What is the Monthly Cost of living for an Average Individual in Toronto?

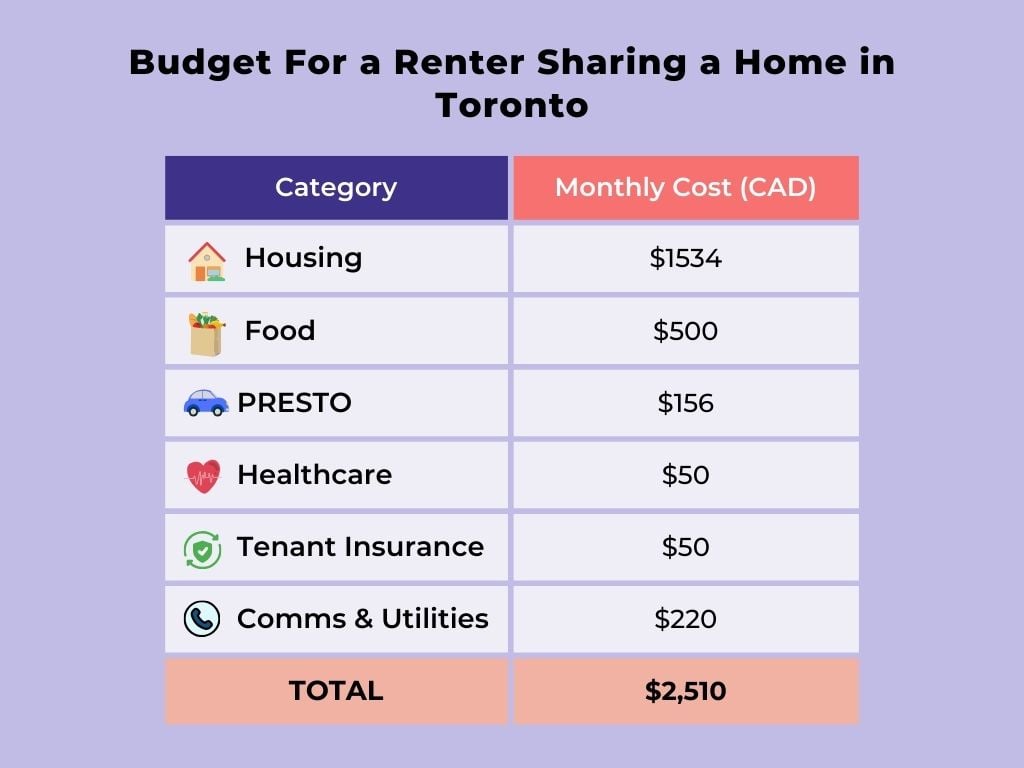

For a single newcomer renting in Toronto’s suburbs, a typical monthly budget might range from about CAD 2,200 to CAD 3,000, with rent often taking CAD 1,000 for a shared house with multiple roommates (using data from Sparrow Share) to CAD 2,300 for a modest one-bedroom or bachelor unit (based on the February 2025 Rentals.ca Rent Report).

We chose $1560 as the price for housing based on a Sparrow Share listing just outside Toronto’s downtown area, but sharing with just one other person. This felt like a happy-medium for this blog post. We recommend checking out the Sparrow Share and Rentals.ca platforms to see your accommodation options across a range of price points.

Plus, CAD 80 to CAD 120 for utilities (depending on usage and season), and around CAD 100 for combined phone and internet, while groceries can hit CAD 375 to CAD 500 if you cook at home frequently and rely on weekly sales or discount grocery stores to keep costs manageable.

Transportation is another key factor; a TTC monthly pass sits at CAD 156, but if you occasionally use ride-hailing services, Go Transit trains to visit downtown, or taxis late at night, this can easily push your transit spend higher, so you need to be realistic about how often you’ll use these services and whether you can carpool to split the cost with friends or colleagues.

What is the average cost of living for a family in Toronto?

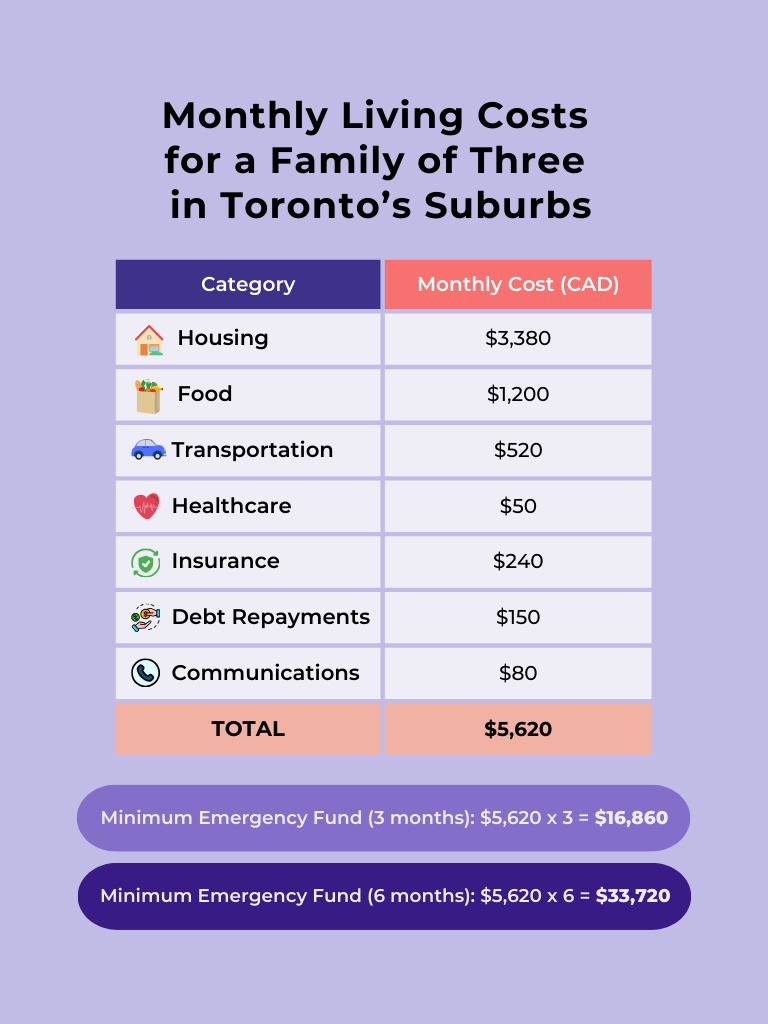

For a family of three renting in Toronto’s suburbs, a typical monthly budget can range from about CAD 4,500 to CAD 7,000 for necessities. In our example, we’ve used a combined CAD 5,620 for ‘needs’, which includes CAD 3,380 for housing, CAD 1,200 for food, CAD 520 for transportation, CAD 50 for healthcare, CAD 240 for insurance, CAD 150 for debt repayments, and CAD 80 for communications. We arrived at CAD 3,380 for housing based on two- to three-bedroom listings in the suburbs, and recommend checking platforms like Rentals.ca to compare additional options.

Groceries are higher for a family than for a single person, so CAD 1,200 reflects the costs for a family that eats most meals at home. Meanwhile, CAD 520 for transportation is based multiple TTC passes for the month. That’s right – this is another no-car family.

How inconvenient, or possible, is it to be “car-free” where you live?

byu/Vagabond_Tea inAskACanadian

More on why we’re choosing car-free budgets in Toronto below.

We also include CAD 50 for healthcare (very bare bones), which covers out-of-pocket expenses not covered by OHIP or private insurance (e.g., some prescriptions), plus $240 for broader insurance which could include tenant’s insurance, life and disability insurance. Finally, $150 for debt repayments and $80 for cell phones round out this family’s essential monthly spending.

So, assuming a budget of CAD 5,620 for ‘needs’, here is a sample look at how different salaries might shake out (approximate 2025 after-tax monthly incomes for Ontario). We’ll use four examples to show how income levels affect what’s left for “wants” and savings:

| Household Salary | After Tax Take Home | Leftover For Wants | Left For Savings |

|---|---|---|---|

| $85,000 | $5,017 | -$603 | $0 |

| $110,000 | $6,308 | $688 | $0 |

| $130,000 | $7,251 | $1,031 | $600 |

| $150,000 | $8,194 | $1,774 | $800 |

Let’s talk about the budget to Live in Toronto

This, of course, depends. Your wants and needs play a major role in how much money you’ll need to get by or thrive in Toronto. If you’re willing to sacrifice a few things for the sake of living in Canada’s biggest city, then you’ll be able to get by on less. Sounds good right? Turns out the things you may need to sacrifice are having a place to yourself (you’ll likely need to share a home) and owning a car.

For families, you might need to compromise on location if you want to live in Toronto on one income – and making the decision to not have a car can offer major savings for you too.

We’ll dig into the average cost stats for Toronto housing and cars later in this blog post.

Quick Budgeting Overview

Before we do, we want to point to some advice from personal finance expert, Ramit Sethi, from a 2023 interview with CNBC:

“Sethi said, people should aim to spend no more than 28% of their gross income on their rent costs. (These include, he added, utilities, furniture, repairs, etc.)

“If you have no debt, you can stretch the number a bit,” he said. In certain expensive cities, Sethi added, “they might spend 30%, 32%, even 35%.”

However, he cautioned, “above that, you’re exposing yourself to serious risk” in the event you lose your job or experience another setback.”

Despite this, figures from the City of Toronto indicate that 23% of renters pay more than 50% of their income on housing. (This is probably why high rental costs are recognized as one of the top 5 challenges newcomers face around finances and banking.)

In other words, we want to be very clear that the decisions you make when it comes to housing in Toronto are likely to play the biggest role in your financial future in Canada.

We really suggest running the numbers to work out what your budget and lifestyle would look like at certain rental price points before committing to a lease. Other than that, you’ll need to know what your income is (take home, not gross), and make a list of everything else you need to pay for (utilities, transport, and food), before digging into what you’d ideally want to buy in Toronto too (gym membership, dining out, holidays, entertainment, hobbies for yourself or your family).

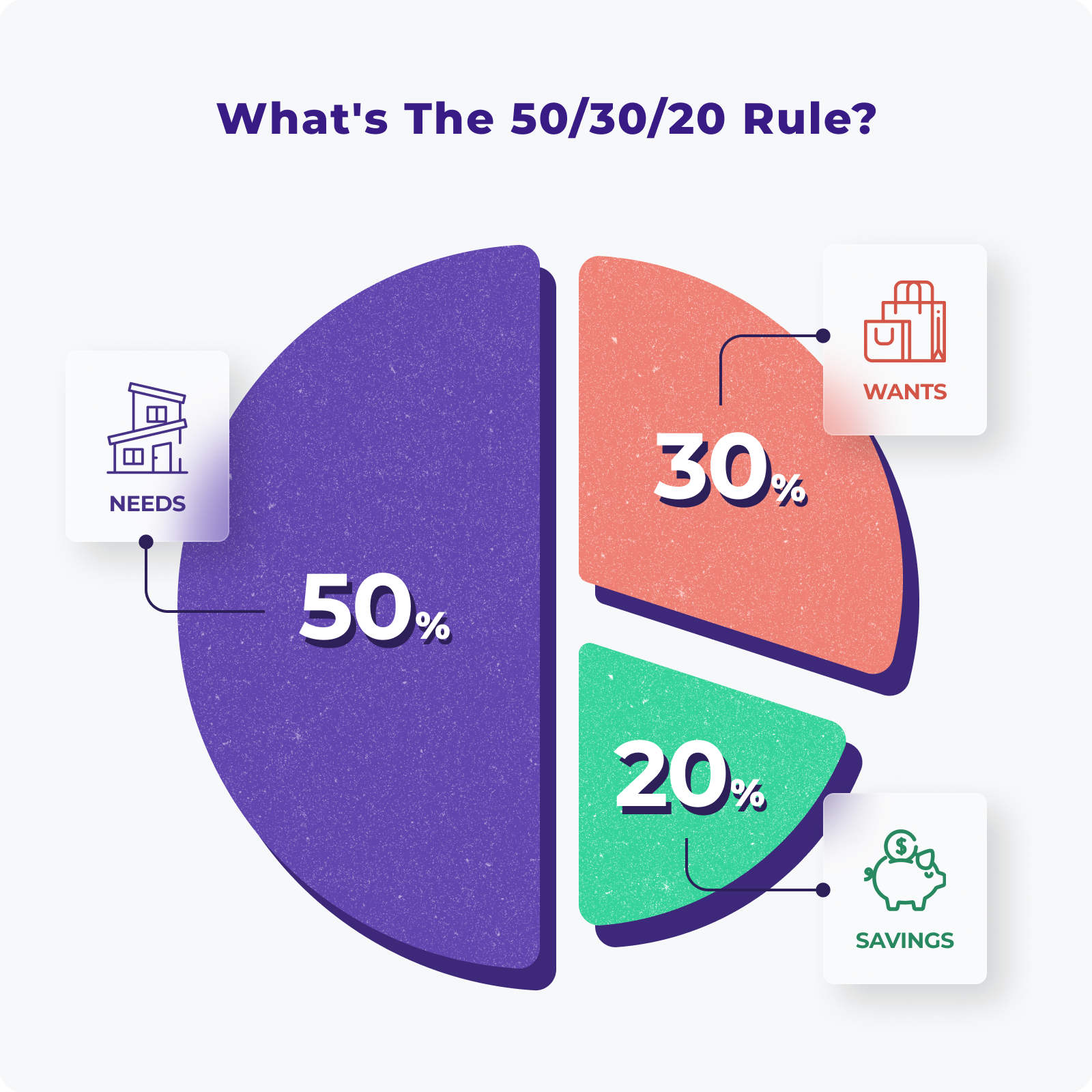

And when you’re choosing where you live in Toronto, the usual wisdom says 50% of your income should go to ‘needs’, 30% to ‘wants’, and 20% to savings or debt. So you might need to adjust your expectations accordingly.

How do entertainment costs affect your budget in Toronto?

Entertainment can be the hidden budget-buster: a simple night out at a mid-range restaurant can cost CAD 25 to CAD 40 per person, movie tickets average around CAD 15, and a bar tab can climb quickly if you’re not careful, so a good guideline is to designate a fixed amount (like 5-10% of your income) for “fun” spending, which ensures you can still enjoy Toronto’s incredible nightlife, cuisine, and multicultural festivals without feeling guilty or pulling money from more critical areas of your budget. (Bear in mind that this is only if you don’t overspend on accommodation.)

How to Live Comfortably in Toronto?

Many people do manage to thrive in Toronto by crafting realistic budgets and making strategic lifestyle choices—like looking for cheaper suburbs rather than the downtown core, shopping smart for groceries, taking advantage of free cultural events, and prioritizing job opportunities in sectors that offer competitive pay.

It’s important to understand that although the cost of living may be high, Toronto also comes with significant rewards: a dynamic social scene, career advancement potential, and an environment that helps newcomers grow both personally and professionally if they manage their money and resources wisely.

What is the secret to managing living costs effectively?

The reality is that your finances will always be a maths problem – no matter what you feel about money.

You might want to live in the shiny new apartment with the gym facilities on-site. You might even tell yourself that you’re saving money in reality because you don’t have to pay for a gym membership. But if the numbers don’t line up for your accommodation costs, you’re robbing yourself of a stronger financial future by signing that lease.

The secret to budgeting in Toronto is to run the numbers, realistically, and understand what impact your choices will have on your lifestyle.

Remember, the 50/30/20 rule can help!

What jobs can help sustain a high standard of living in Toronto?

Ultimately, income is a big factor in how comfortable you’ll be in Toronto. The higher your earnings, the easier it is to handle the city’s costs. So, what kind of jobs or careers put you in a good position to live well here?

Toronto is Canada’s largest job market, with opportunities in many industries. Some sectors tend to offer higher salaries that can sustain a higher standard of living:

- Technology (IT jobs): Toronto has a booming tech sector (sometimes nicknamed “Silicon Valley North”). Jobs like software developers, data scientists, IT project managers, etc., are in demand and often pay well above the city’s average salary. For example, a software developer with a few years’ experience can earn $80,000-$100,000+. These incomes allow one to comfortably rent (though, they’ll do better to share a home) and still have money for savings and leisure.

- Financial Services: As home to the Toronto Stock Exchange and many banks, Toronto’s finance sector is big. Jobs in banking, investment, accounting, and fintech can provide solid incomes. A financial analyst or accountant might earn $60k-$80k, while more senior roles or specialized fields (like investment banking) can be six-figures. Finance and accounting professionals with certifications (CPA, CFA, etc.) are well-compensated.

- Healthcare and Life Sciences: Healthcare jobs (nurses, radiologists, pharmacists, etc.) offer stable, good incomes. A registered nurse in Toronto, for instance, can earn around $75k annually. Doctors and dentists, once established, earn well into six figures (though it takes many years and expenses to get there). The biotech and pharmaceutical industries also have roles in Toronto (especially with many hospitals and research institutions) that pay competitively.

- Engineering and Skilled Trades: Professional engineers (in civil, electrical, mechanical fields) are in demand for Toronto’s constant development and infrastructure projects. An engineer might start around $70k and go up from there with experience and P.Eng licensure. Don’t overlook skilled trades either: electricians, plumbers, HVAC technicians, elevator mechanics – these tradespeople are needed and can earn a strong income, often in the $60k-$100k range after a few years, and with less student debt than white-collar paths. The city has a shortage of some trades, pushing wages up.

- Business Management and Sales: Climbing the ladder in corporate roles or excelling in sales can yield high pay. For example, an experienced sales manager or a business development executive in a large company might earn a base salary plus commission/bonus that puts them well over $100k if they perform well. Similarly, project managers or consultants in high-demand fields can do very well.

- Creative and Specialized Professions: Toronto is a hub for media, film, and design in Canada. Some of these jobs (e.g., UX designer, marketing director, film production manager) can pay decently, though creative fields often have more variance. There are also lots of public sector and education jobs (government, universities) which may not pay sky-high but have good benefits and stability, which contributes to living comfortably in a different way.

- Entrepreneurship: Some newcomers start their own businesses – from restaurants to tech startups. Income here can be very high or very low depending on success. It’s higher risk/higher reward. But Toronto’s large market can be lucrative for entrepreneurs who find a niche.

While precise data is hard to find, anecdotally, the average salary in Toronto is around $62,000/year. So jobs that pay at or above the city average will obviously make life easier. Many of the fields above have average salaries that meet or exceed that. For instance, many tech and finance jobs start at or quickly reach the $60k+ range, whereas in retail or hospitality you might earn much less.

How much do you need to earn for a higher standard of living in Toronto?

Now, what is considered a “high standard of living” income-wise? As a rough guide, an individual probably would start to feel more comfortable in Toronto on anything above $75,000 per year (which after tax might be around $50k-$55k take-home, or about $4,500/month). With that, you could rent a decent place and still save or travel occasionally. Though, some data says that you’d want to be earning $85,000 as an individual before buying a car in Toronto.

A household with two earners making say $60k each (so $120k combined) would be in a solid position to maybe start saving for future goals, especially if they’re in a one-bedroom apartment. At 2-bedrooms with a child, a couple earning $120,000 still has some breathing room, but may find it harder to save for their future.

If you’re just starting out or your profession isn’t in a high-paying field, don’t be discouraged. Many newcomers begin with survival jobs (e.g., working in a cafe or store) which might pay nearer to minimum wage. It can be tough to save or get ahead at ~$30k/year in Toronto; in those cases utilizing all the cost-saving tips we discussed is crucial. But Toronto also offers lots of opportunities for upskilling: you can take courses, attend networking events, and gradually move into better-paying roles. Even moving from a low-wage job to a middle-wage job (say, $40k to $50k) can significantly improve your comfort level.

Cost of Living in Toronto as a Couple

Dual-income advantage: two incomes make a huge difference. For example, two people each earning $45k (a pretty average wage) together bring in $90k, which usually is enough to rent a moderate apartment, run a modest car, and raise a child with careful budgeting. Many families in Toronto rely on dual incomes to afford their lifestyle. If only one partner works, a single income often needs to be quite high to maintain the same standard.

Managing the Cost of Living in Toronto

Moving to a new city like Toronto is exciting, and while the cost of living can be daunting, proper planning goes a long way. To recap,

- Budget generously for housing because rent is the single biggest expense (consider sharing or living a bit outside the core to save money).

- Keep an eye on transportation costs – the TTC is your wallet’s friend, and cars are a luxury.

- Food and entertainment are within your control: cook often and enjoy Toronto’s free or low-cost attractions to keep those in check.

- Healthcare, thankfully, won’t break the bank thanks to Canada’s system, but remember to plan for what it doesn’t cover.

- Work to stretch your dollars further whenever you can.

About the author