Updated on July 23, 2026

This content is sponsored by Scotiabank. The views, opinions, and information expressed in this piece are those of Moving2Canada and do not reflect those of Scotiabank. Scotiabank is not responsible for the content, accuracy, or any representations made herein.

Buying a home is a huge milestone for newcomers to Canada. And it’s likely that a mortgage will play a role in you buying your first home. But there are a lot of moving parts to manage when applying for your mortgage. So, we’re sharing some key information about getting a mortgage as a newcomer to Canada to help you make sense of the journey ahead.

- Start here if you want a broader overview of everything that goes into buying your first home as a newcomer.

Getting A Mortgage As A Newcomer To Canada

Getting a mortgage is seen as a rite of passage for many newcomers to Canada. Many recent immigrants are quick to realize that dream too, according to government reporting that shows almost one quarter of newcomers had a mortgage in 2023.

For those of you looking to get a mortgage as a newcomer to Canada, there are three distinct phases in your mortgage journey

1: Preparing to get a mortgage.

2: Finding a lender experienced with newcomers.

3: Applying for (and receiving) your mortgage.

We’re going to walk you through these three crucial phases.

Before You Apply For A Mortgage

Preparing to get your mortgage is a process that can take some time as a newcomer to Canada. But, it will all be worth it once you get the keys to your new home.

Here’s what you need to do before you can get a mortgage in Canada:

- Establish credit history: you will generally need to have a good credit history before you can get a mortgage in Canada. This shows Canadian lenders that you are a responsible borrower.

- Save for a down payment: a down payment is an amount of money that you pay upfront to buy a home. Generally, you will need to save between 5% and 35% of the home’s purchase price as a down payment.

- Save around 1.5% of the home’s purchase price for closing costs. This percentage is a rule of thumb to estimate the closing costs for the home, which includes things like land-transfer tax, home inspection, appraisal fees, legal fees, title insurance, and moving costs.

- Gather your documents. You will need to provide a range of documents to buy a home in Canada, including tax returns, bank statements, a letter from your employer to confirm your employment, pay stubs, debt information, and rental history. You might need additional documents, depending on your situation.

- File your taxes. You will need to be up-to-date with your personal income taxes with CRA to apply for a mortgage in Canada.

- Consider how your goals and risk tolerance might impact your mortgage. Mortgages are quite customizable, you can choose different amortization schedules (which refers to the actual number of years (mortgage length) it will take to repay a mortgage loan in full ), interest rate arrangements (fixed or variable), and down payments.

A note about standard mortgage qualifying tools:

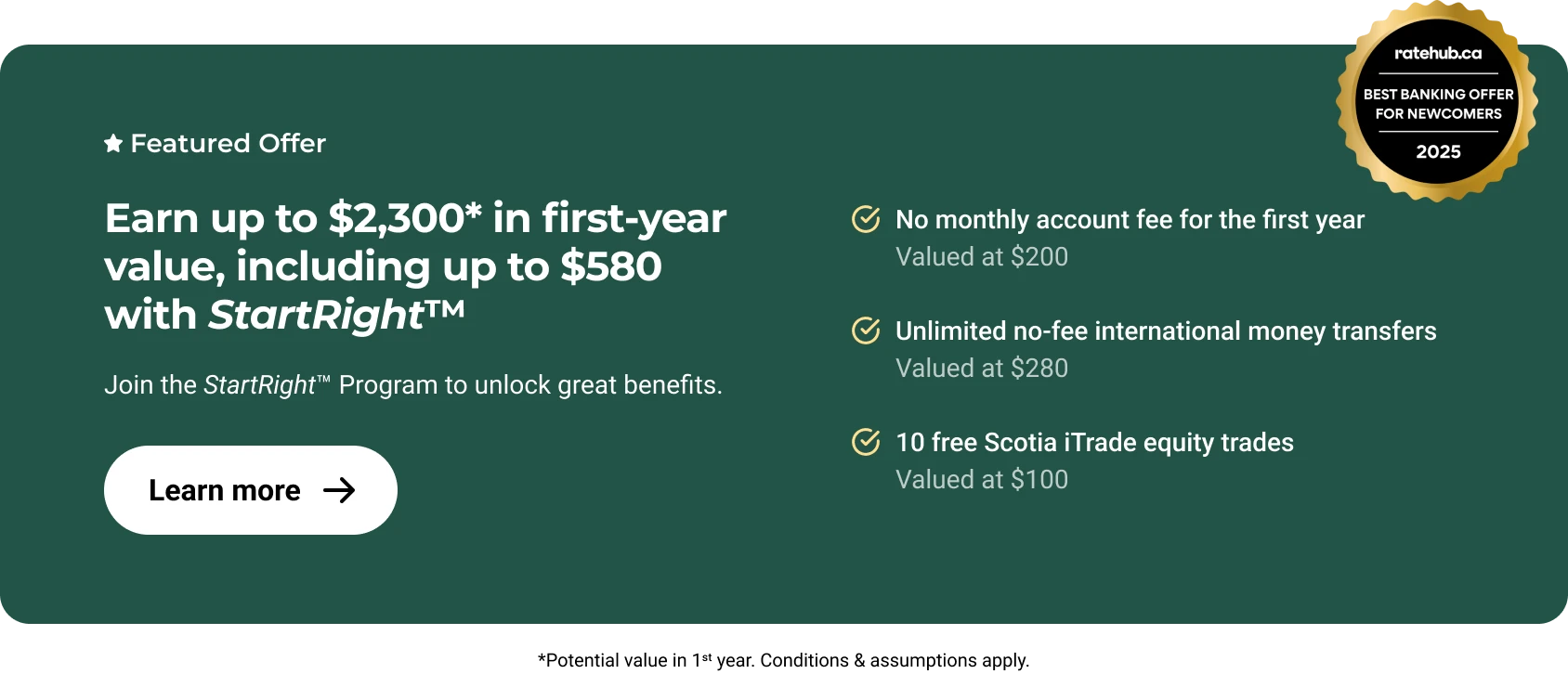

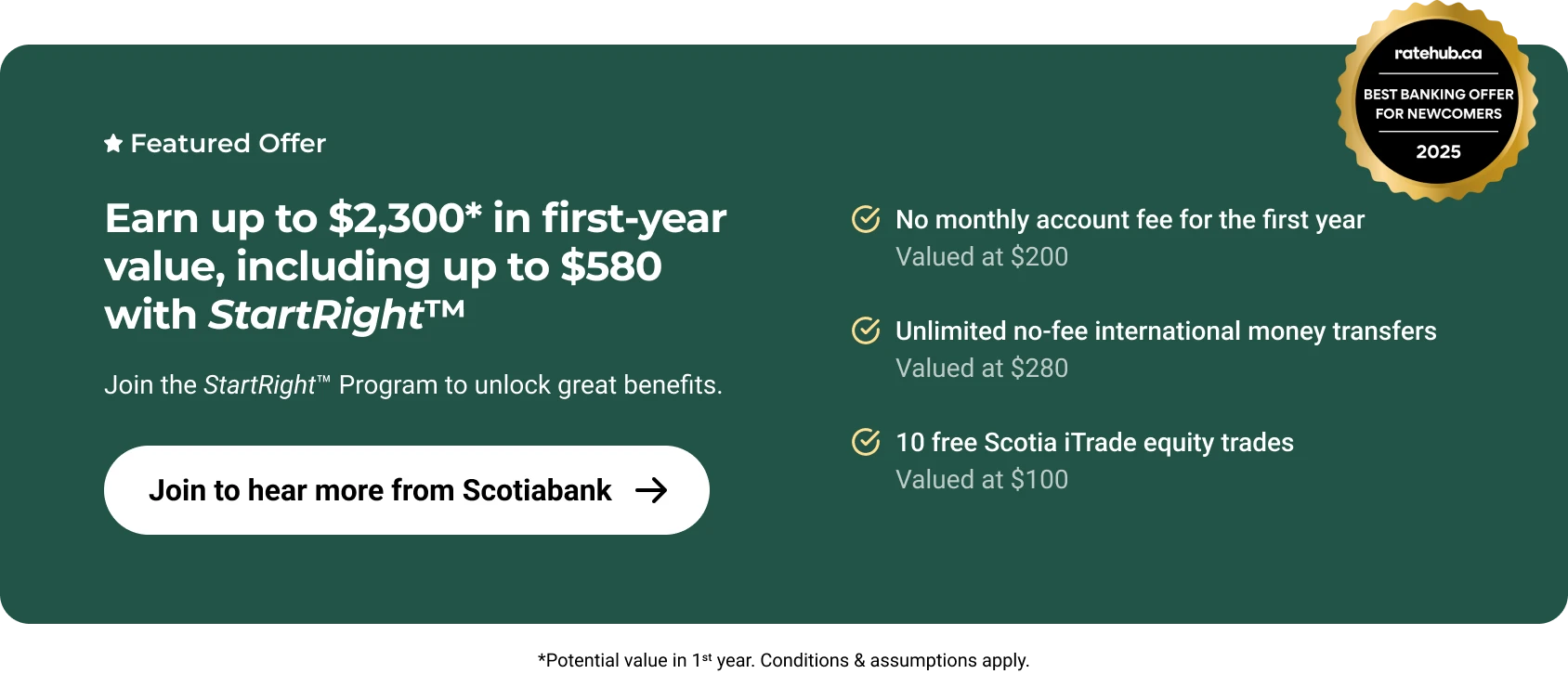

Mortgage tools are based on standard applications, and may not fit your unique situation if you are a newcomer to Canada. If you’re ready to buy a home and you have moved to Canada in the last five years, speak with a Scotiabank Home Financing Advisor for a tailored solution that suits your financing needs.

Find A Lender Experienced With Newcomers

Many newcomers to Canada may not be able to meet standard mortgage qualification criteria due lack of an established credit history, limited employment history, temporary residency status, or other factors.

As such, it is important to find a lender experienced with a newcomer’s unique circumstances to guide you through your mortgage journey. Working with a lender, like Scotiabank, that offers specialty mortgage qualification programs for newcomers is beneficial in helping you along the mortgage qualification process to reach your homeownership goals.

Learn more about Scotiabank’s mortgages for newcomers to Canada online or book an appointment with a Scotiabank Home Financing Advisor.

Applying For A Mortgage

The first step in your mortgage application is usually to get mortgage pre-approval. A mortgage pre-approval means that the lender has pre-qualified you for a certain loan amount based on your current financial situation and typically has locked in an interest rate. This process can be straightforward if you have all your documents and information ready to go.

With your pre-approval in hand and a lender you trust on your side, it’s time to put in an offer on the home you’re interested in purchasing in Canada, and then start the final mortgage application process if that offer is accepted.

If you’ve worked hard and thoughtfully during the pre-application process, this should run smoothly. It will be a matter of you submitting your documents to your mortgage agent to put together your application. This will then be sent for underwriting and processing. That said, a mortgage pre-approval does not guarantee you will get your mortgage. So it’s important to be responsive throughout the process if your lender has any follow-up queries.

- You can get a bird’s eye view about the home buying process in Scotiabank’s content about how to buy a home as a newcomer to Canada. This includes information about other services you’ll need to buy a home, such as legal services and a realtor.

Newcomer Tips For A Smooth Mortgage Application Process

As you can see, the mortgage application process can seem overwhelming at first. But with careful planning, you’ll be in the best position to get into your new home. These tips will help you:

- Start building your credit as early as you can.

A good credit history can help you get a mortgage as a newcomer to Canada. So, it’s helpful to start building your credit as early as possible in your journey.

- Keep your documents up-to-date.

Finding a home in Canada can take some time, and it’s important to keep the documents you need to apply for your mortgage up-to-date during the process, including filing your taxes in a timely manner. As we said above, a pre-approval isn’t a guarantee that you will receive that mortgage. So, you should update your lender if your circumstances change during the process.

- Avoid applying for other debt during the mortgage application process.

Your monthly debt repayments impact how much you can borrow when you get your mortgage. It’s usually best to avoid taking on other debt if you plan to buy a home soon.

- Keep your long-term financial goals in mind.

Home ownership may come with additional, even unforeseen, costs. While getting into the real estate market in Canada may be an important part of your long-term financial plan, it’s important to make sure you can afford the upkeep of the home as well as your other goals.

Apply For A Mortgage With Scotiabank

Learn more about Scotiabank’s mortgages for newcomers to Canada online or book an appointment with a Scotiabank Home Financing Advisor.

Legal Disclaimer

Related articles

New Canada Child Benefit Payment Coming August 20. Here’s How Much You’ll Get.

Read more

New Alberta Child and Family Benefit (ACFB) Payment Coming August 27

Read more

New Ontario Trillium Benefit Payment Coming on August 10: What Newcomers Should Know

Read more

New CRA Benefit Payments in August 2026: What Newcomers Could Get

Read more

About the author