Updated on April 20, 2026

This content is sponsored by Scotiabank. The views, opinions, and information expressed in this piece are those of Moving2Canada and do not reflect those of Scotiabank. Scotiabank is not responsible for the content, accuracy, or any representations made herein.

Canadians love to own their own homes. And, while many immigrants in Canada might aspire to join the ranks of homeowners, they may need to rent for a while before they can buy property in Canada. Indeed, it might even make sense to rent rather than own a home.

So, should you buy or rent a home as an immigrant in Canada?

For a long time, the majority of Canadians have chosen to buy their homes. As of 2021, two-thirds of Canadians own their home. However, rental household growth of 21.5 percent over 10 years is now outpacing owner household growth of 8.4 percent.

There are significant pros and cons to renting or buying a home in Canada. Today, we’ll outline the pros and cons of renting or buying property in Canada.

Renting as a newcomer to Canada

The rules and practices of Canada’s rental market are largely dictated by your province and municipality. It’s a good idea to know provincial or local rental laws so that you understand what to expect (psst! we’ve a whole guide on renting in Canada right here).

Your rental budget in Canada generally depends on how much money you make each month. One popular rule of thumb states that your monthly rent should be no more than 30 percent of your monthly paycheque before taxes. This is typically easier in smaller cities and towns and may be more challenging in larger cities such as Toronto and Vancouver where the monthly rent for a 1-bedroom apartment can exceed $2,500.

Most of the time, renting a home or apartment in Canada involves signing a lease. The lease will dictate the terms of your contract with the unit’s landlord or property management company. If there are issues, each province has a separate governing body that can offer resources or mediate disputes between landlords and tenants.

Pros of renting in Canada

- Renting offers more flexibility – you can exit your lease and move out if you give the appropriate notice to your landlord.

- Short-term options may be available if you aren’t sure where you want to live.

- Since the landlord is responsible for repairs and maintenance, you — the renter — will spend less time, money, and effort if something in your home breaks or needs to be upgraded. In this sense, renting can be less stressful than owning.

Cons of renting in Canada

- Depending on factors like your location, lease terms, and the age of your rental home, you may be vulnerable to unexpected rental increases.

- You cannot renovate, upgrade, or change your home without your landlord’s approval.

- Renting a home does not build equity or wealth for the tenant. Renters may find it more difficult to build their credit rating.

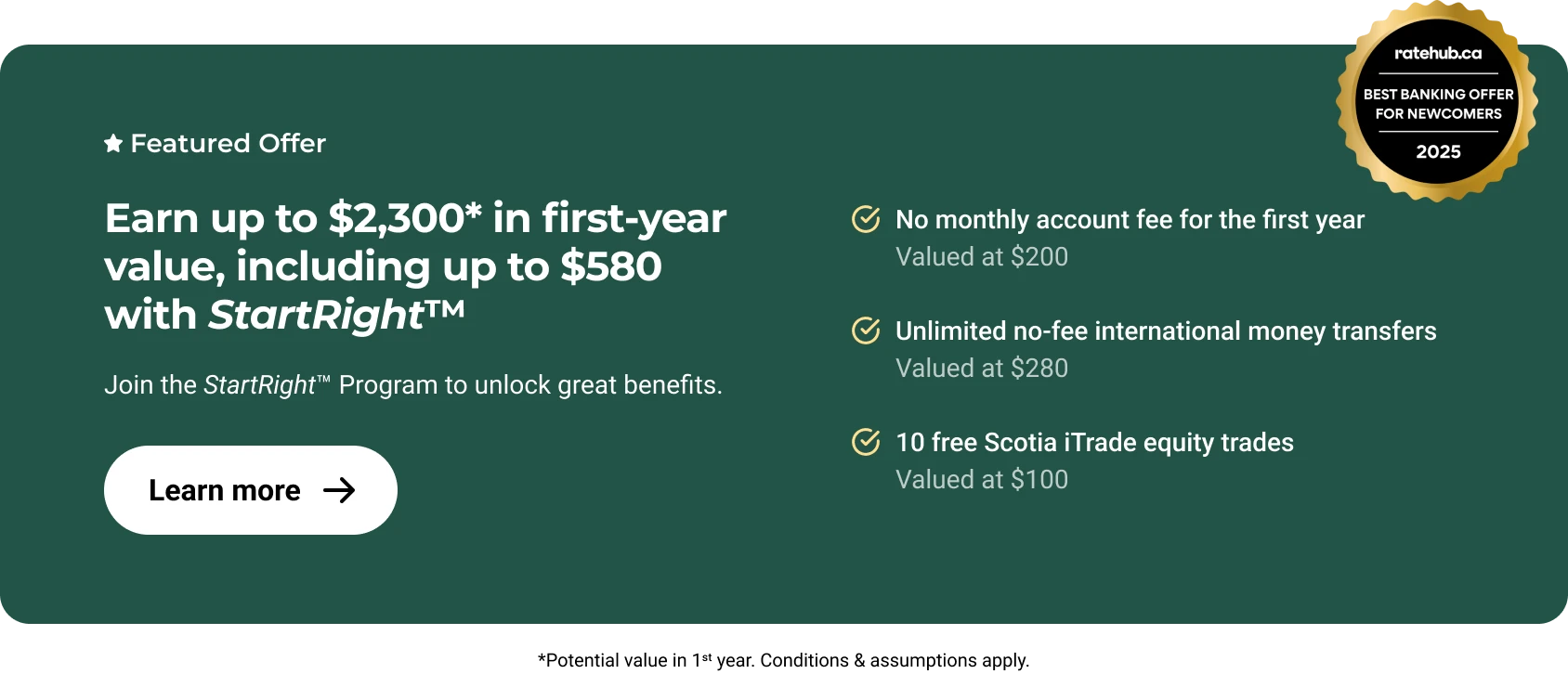

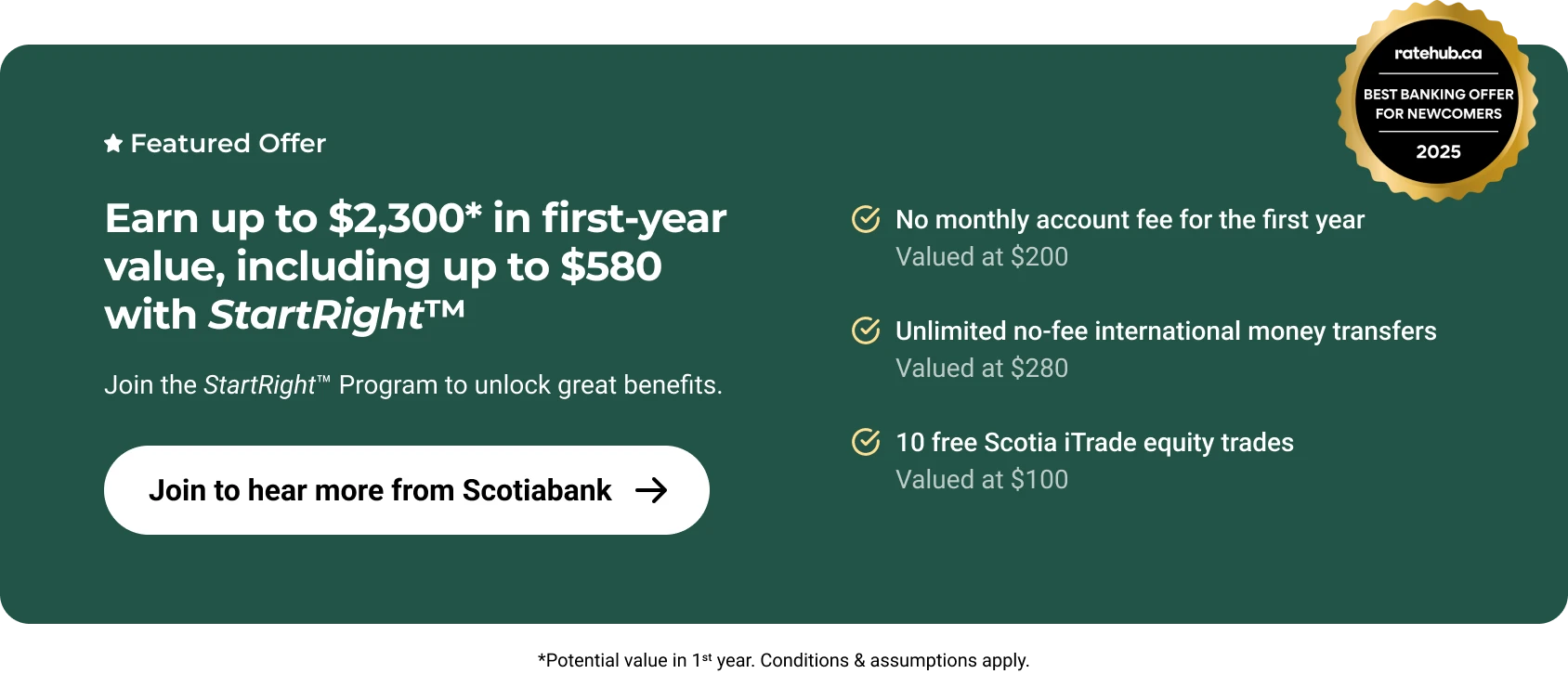

Having to build your credit history from scratch can be challenging and usually takes time and effort. The good news is, with Scotiabank’s new partnership with Nova Credit, eligible clients can now use their foreign credit history reports to apply for a higher credit limit on their credit card. You can learn more about this exciting partnership and all things related to credit here.

Buying a home in Canada as a newcomer

So much goes into buying a home in Canada (psst! we’ve a whole guide on that too, right here). There are a few basics you need to know to get started on buying property in Canada

In Canada, home buyers need a cash down payment to purchase a home – usually between 5 and 20 percent of the purchase price. Once you have money saved for a down payment, you must secure approval for a mortgage from a bank or mortgage lender. This is called the mortgage pre-approval process. At the end, you’ll know exactly how much the lender is willing to loan you, which will determine how much you can afford to spend on your home.

As you’re looking for homes, you can strike out on your own or work with a real estate professional (often called a realtor or real estate agent) to help guide you in your search. Depending on where you live, hiring a lawyer to review the final paperwork may also be mandatory.

Pros of buying a home in Canada

- Your purchased home is a legal asset that you own. As you pay off your mortgage, you build equity that can benefit you and your family later in life.

- A home provides stability and security as long as you can pay your mortgage and property taxes on time.

- Buying a home means that you can choose exactly how to decorate and make aesthetic and structural choices to suit your needs.

- As an owner you choose if the property is subsequently sold, while renters may need to move out if the owner decides to sell.

Cons of buying a home in Canada

- Home maintenance and upgrades are entirely your responsibility.

- If you ever want to move from your home, it may be more complicated to leave a home you own rather than one you rent.

- Factors out of your control, like high interest rates, can impact the value of your home or make mortgage payments more expensive if on a variable rate.

- Homeowners are typically responsible for paying property and other taxes, which may increase with the value of the property.

- While property values may increase over time, the value of a home may also decrease.

Start your journey off right with Scotiabank

Renting or buying a home in Canada is affected by many factors, including location, budget, family size, and employment. While many professionals can advise you on your rights and responsibilities as a homebuyer or tenant, the best decision is the one made with your personal or family circumstances in mind.

To ensure you know as much as possible to guide your decision, contact an advisor at Scotiabank. The Scotiabank team can provide guidance and advice at any point, working with you to ensure you have the financial support you need to navigate the process of finding your home in Canada.

Book an appointment today.

Legal Disclaimer

About the author