Updated on June 5, 2026

This content is sponsored by Scotiabank. The views, opinions, and information expressed in this piece are those of Moving2Canada and do not reflect those of Scotiabank. Scotiabank is not responsible for the content, accuracy, or any representations made herein.

We get it now. Building and strengthening a good credit history is crucial when planning on living a comfortable life in Canada. It's the ultimate proof of solvency to banks, which opens many doors. But once the basic steps to build the foundation of a solid credit score are accomplished, how do you continue to strengthen your rating?

Read more: How to start building a good credit score

What is credit?

As a quick reminder, credit is a contract or an agreement where someone borrows money and repays that money to the lender at a later time, generally with an interest charge. The interest is the cost of the loan.

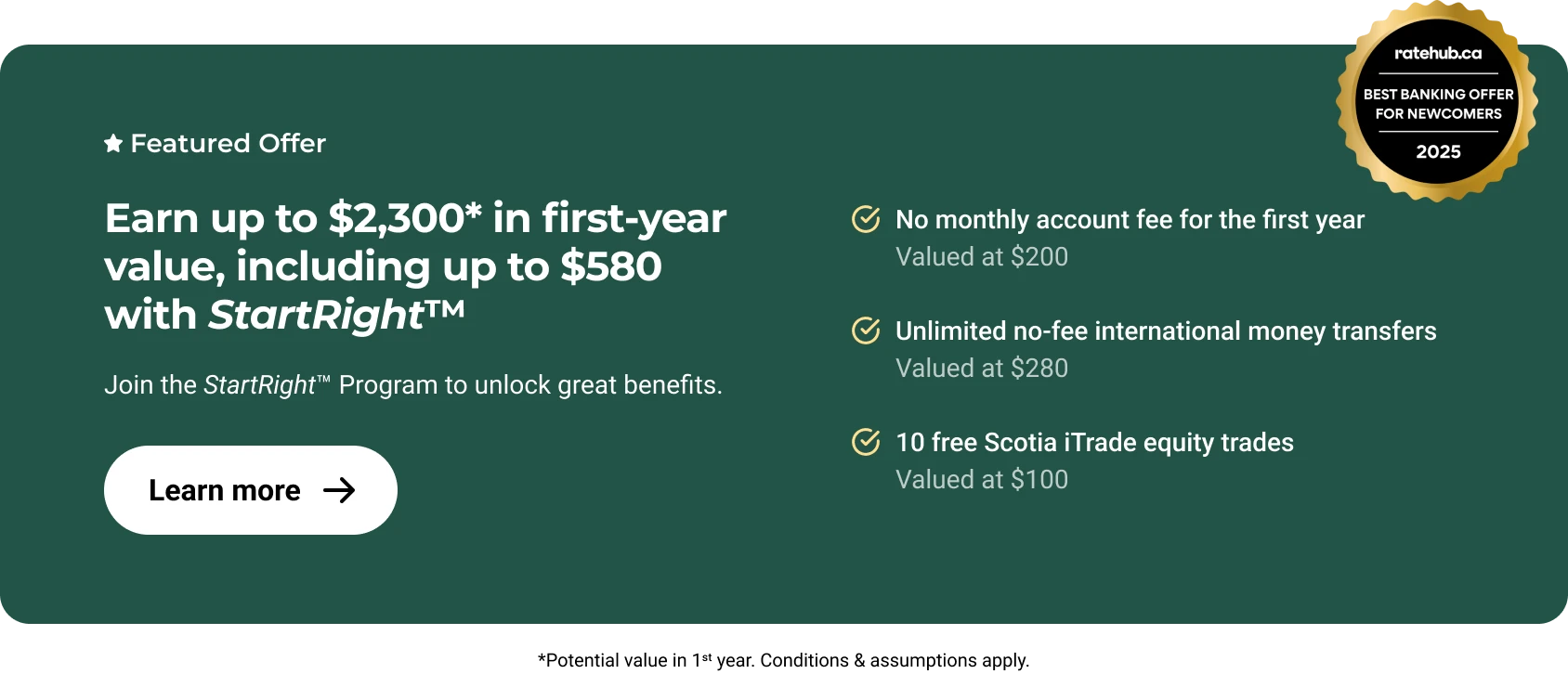

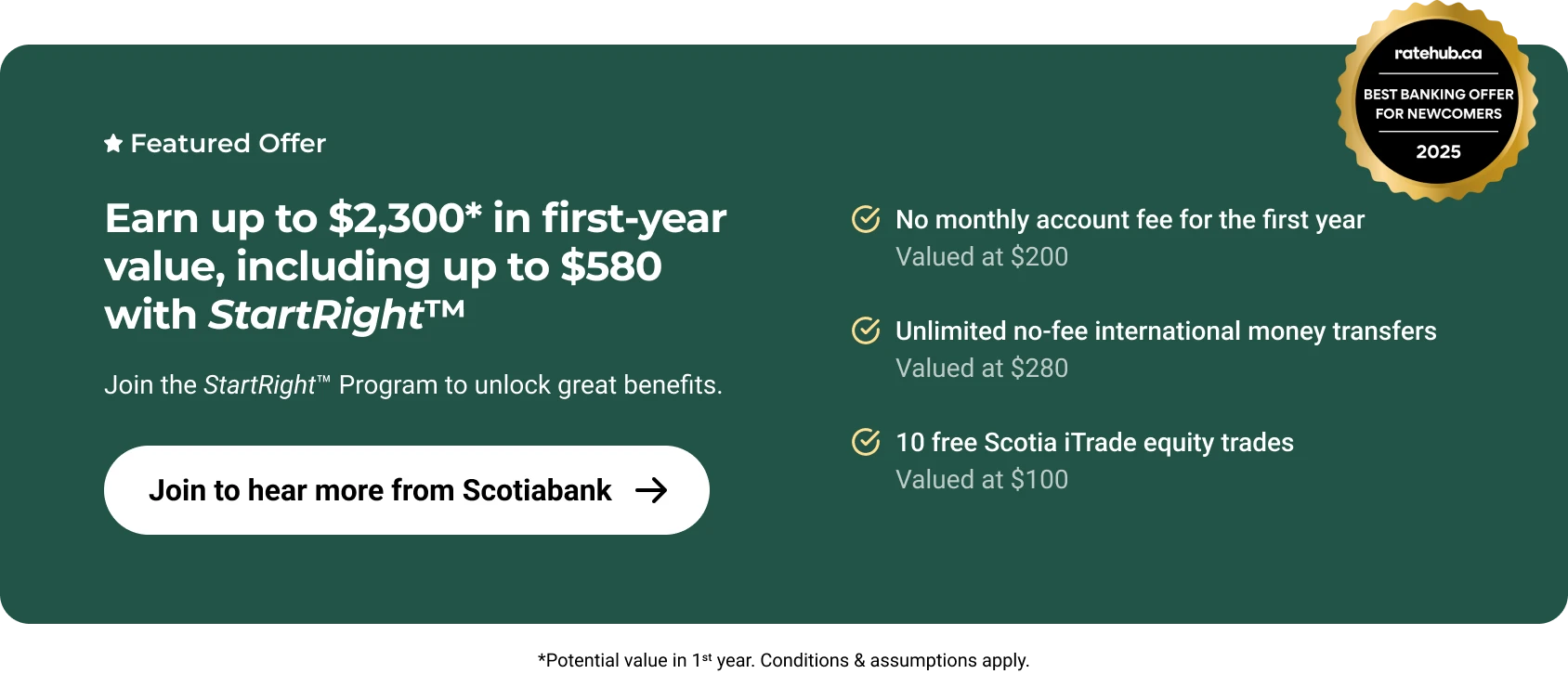

As we introduced in our conversation with Morteza Hessari, financial advisor at Scotiabank, coming to Canada and having the ability to pay for many necessities, including a home, acquiring loans, or paying for everyday items will depend on your ability to receive credit. Building your credit history can take time if you are unfamiliar with the financial landscape of Canada, but there are ways, through the Scotiabank StartRight® Program1, which allows you to build a needed credit history quickly and effectively.

Having to build your credit history from scratch can be challenging and usually takes time and effort. The good news is, with Scotiabank’s new partnership with Nova Credit, eligible clients can now use their foreign credit history reports to apply for a higher credit limit on their credit card. You can learn more about this exciting partnership and all things related to credit here.

Reinforcing credit history

Our conversation with Morteza showed us that there are a few simple steps we can follow to start building a credit history:

- Always pay your bills on time

- Pay bills in full, as much as possible

- Don’t apply for too many cards at once (this can negatively affect your credit score)

- Keep balances low, if possible

- Don’t go over your credit

Respecting these is a base. But what matters to us now is how to keep on reinforcing our history.

Here are a few actions that will help bulletproof your credit score:

Less is more! Manage credit utilization effectively

Aim to use less than 30% of your available credit. If you’re nearing your credit limit, either reduce your spending on credit or consider requesting a credit limit increase to maintain a lower utilization rate.

Maintain older credit accounts

We’re talking credit history here. Let’s keep in mind that the age of your credit accounts is a factor in your credit score. The older your credit activity is, the more trustworthiness you can prove. Keep your old credit accounts open and active, as this helps to show a longer credit history. BUT! Be careful not to accumulate too much available credit, which can be tempting to overspend.

Diversify your credit types

Having a mix of different types of credit, such as a credit card, car loan, or line of credit, can positively influence your credit score. It demonstrates your ability to manage various types of credit.

Limit new credit applications

It’s all about striking the right balance. Mixing up your credit types is smart, but don’t get carried away with too many applications. Each new credit application can lead to a hard inquiry, which might lower your score temporarily. Be strategic about applying for new credit.

Leverage automated support

To make sure you make your payments on time, you can set up automatic payments or electronic alerts from your financial institutions. This will help you avoid missed payments and keep your credit in good standing.

Remember that your bank is here to help you and there are programs available to support you in your quest for the ultimate creditworthiness. Scotiabank, for example, offers its StartRight® Program.

The Program allows you to apply for a credit card without having any previous credit history in Canada. If approved, once you have your card and make purchases with it, you are on your way to building credit history so long as you are using it responsibly by making the full payments on time. Through the StartRightTM Program, you can bank without monthly account fees for the first year2 and get up to a $15,0003 credit on a Scotiabank credit card. The longer you have a credit card or credit account open and in use, the better it is for your score (but only if you are paying your bills on time).

Different cards to choose from

There is no one-size-fits-all solution for people looking for credit cards. With many options available, it’s easy to find a solution that will fit your needs and spending habits. Scotiabank offers many cards for newcomers looking to build a credit history in Canada.

To learn more about the Scotiabank StartRight® Program and what it offers newcomers, click here.

Quick tip: What is a good credit score in Canada?

A credit score is a 3-digit number that ranges between 300 and 900.

The higher your score, the more creditworthy you are, and the more chance you get to obtain better rates.

According to Equifax, which is at the origin of the credit score, here are the different rate ranges:

- 760 and above is excellent

- 725 to 759 is considered very good

- 660 to 724 is considered good

- 560 to 659 is below average

- Less than 560 is poor

Finally

For newcomers in Canada, there is no universal way of reporting credit scores between countries, so you will start with a Canadian credit score of zero. But through programs like StartRightTM, giving you the ability to build that history by obtaining your first Canadian credit card, you are on your way to improving that score almost immediately. It could take a few months or longer but with responsible repayment and patience, you are well on your way to building a credit history in Canada that will open doors to opportunities to build your new life here.

Legal Disclaimer

About the author