Updated on April 27, 2026

This content is sponsored by Scotiabank. The views, opinions, and information expressed in this piece are those of Moving2Canada and do not reflect those of Scotiabank. Scotiabank is not responsible for the content, accuracy, or any representations made herein.

Regardless of what they want to be when they grow up, most young people in Canada will need some post-secondary education before they can launch their career. This ranges from vocational training and apprenticeships to college and university. Fortunately, there are lots of options for education in Canada, which is part of why this country is so attractive to newcomers.

Canada’s post-secondary schools are some of the best in the world, and even if this path doesn’t appeal, there are many alternatives that can help young people further their education and study their way to a great career.

Unfortunately, like most things nowadays, post-secondary education costs are rising. As of 2023, undergraduate students in university pay an average of $6,834 per school year in tuition alone. Add in the price of rent, food, books, transportation, and other university fees (which averaged $1,039 in 2022/2023 nationally), and it’s no surprise that students and their families are feeling stretched thin.

To offset these costs and support their kids as they get educated, many Canadians start saving for their children’s post-secondary education early. The Government of Canada has several tools that can help, including the Registered Education Savings Plan (RESP).

Today, we’ll show how newcomer parents and parents-to-be can save for their child’s education in Canada through RESPs and other smart and savvy savings strategies.

What is a Registered Education Savings Plan (RESP)?

Let’s get the heavy hitter out of the way first. A Registered Education Savings Plan (RESP) is a long-term educational savings account that any adult can open. Its reserves can be used to fund any type of post-secondary education, including university, college, apprenticeship programs, CEGEP (in Quebec), and trade school.

There are certain advantages of opting for an RESP. Savings grow tax-free, compounded. Plus, the government contributes a percentage of every dollar invested into a RESP, up to a specified annual limit and up to a lifetime maximum. Better still, family and friends can help to grow the plan more quickly by making monetary contributions, perhaps around special occasions and life milestones. And if the child chooses to defer their education plans after high (secondary) school, they can still use the RESP money when they are ready to go back to school at a later date.

Overall, a RESP is a great option for funding the post-secondary education of a child in Canada.

There are a few terms you should know when talking about RESPs:

- Subscriber: This is the person who opens the RESP. A subscriber can be any adult – they do not need to have a bank account or even be a resident of Canada.

- Beneficiary: This is the intended recipient of the RESP. A subscriber can open an RESP for their child or to fund their own education. The beneficiary is the person whose Social Insurance Number (SIN) is connected to the account’s registration.

- Promoter: This term refers to the financial institution that opens your RESP – often a bank or a credit union. Their job is to oversee contributions and eventually release the funds to the beneficiary.

As a parent, you would be the subscriber who opens the RESP for the beneficiary (your child). As soon as your child has a SIN number, you can open an RESP.

Once the RESP is open, you can set it up so that certain eligible Canadian government benefits and incentives are automatically deposited into the account. This includes:

- The Canadian Learning Bond (CLB): an amount offered to low-income Canadian residents under 15. The first year they are the beneficiary of an RESP, they will receive $500, then $100 per year until they reach 15 years of age.

- The Canada Education Savings Grant (CESG): a program designed to match up to 20% of some contributions to the RESP, up to a lifetime value of $7,200 per person.

- Additional benefits administered by the provinces of Quebec and British Columbia.

Receiving CESG funds is contingent on contributions to the RESP. However, this is only one benefit of having a RESP account. The funds deposited into a RESP grow tax-free, up to a lifetime contribution limit of $50,000. Even if your child decides to pursue a study program with high tuition fees, this money will put a sizable dent in their school-related expenses.

Beyond RESPs: Saving for Your Child’s Education

While RESPs are a great savings tool, there are many other savings vehicles and resources families can implement to help save for a child’s education. What’s most important is that you start as soon as possible. The more time your money has in the account, the more the interest may grow.

Here are a few more options to help you save for your child’s education beyond RESPs.

1. Open a tax-free savings account

A tax-free savings account (TFSA) is a type of account that safeguards your money tax-free. You can contribute up to a set maximum amount every year and use those funds to save or invest within the account itself. Money can be withdrawn from a TFSA at any time for any reason.

2. Open a regular bank account and use it for this purpose

While setting up a TFSA doesn’t take too long, it is still more complex than simply opening a regular bank account. If you want to quickly open a dedicated account for your child’s educational savings, you can open a standard savings account through your bank and deposit the money there. You can expect to receive a small amount of interest on the money and can make transfers and withdrawals quickly and easily.

3. Set up a trust agreement

Another great way to set up savings for your child’s education is to establish a trust. Essentially, a trust is a system of control that’s applied to various assets, including cash, investments, or real estate. The person setting up the trust has broad authority over how the money is used, both during their life and after their death.

A trust is administered by a trustee (either a person, a company, or both) who is responsible for managing, overseeing, and distributing the assets. Setting up your assets this way ensures that the money can only be used for educational pursuits, if desired.

Our Best Savings Tips for Newcomers

While there are lots of financial resources that can help you figure out the best savings plan, they can only get you to the starting line. You’re the one who has to do the hard work of putting aside money to fund these accounts. When you’re first settling into your life in Canada, this can seem like a big hurdle.

Here are some of our best tips to help make savings for your kid’s education easier.

1. Set it and forget it

Don’t make transferring money into your RESP or savings account just another task you have to remember to do. Instead, set up a regular auto-deposit into the account from your primary chequing account. You can do it weekly, monthly, quarterly, or even yearly. Regardless of how often you contribute, automating your savings takes that task off your plate.

2. Tell your friends and family

Wouldn’t it be great if you could have a little help with saving for your kid’s education?

When you first set up your RESP or savings account, let your friends and family know that while you don’t expect gifts for your child, if they feel so inclined, they could contribute to their education instead of buying them gifts for special occasions.

3. Don’t compromise your retirement

While offering your children as much money as possible for their education is tempting, it may not be worth compromising your retirement. Many loans are available for Canadian residents seeking an education, but it might be trickier to secure a loan to fund your retirement.

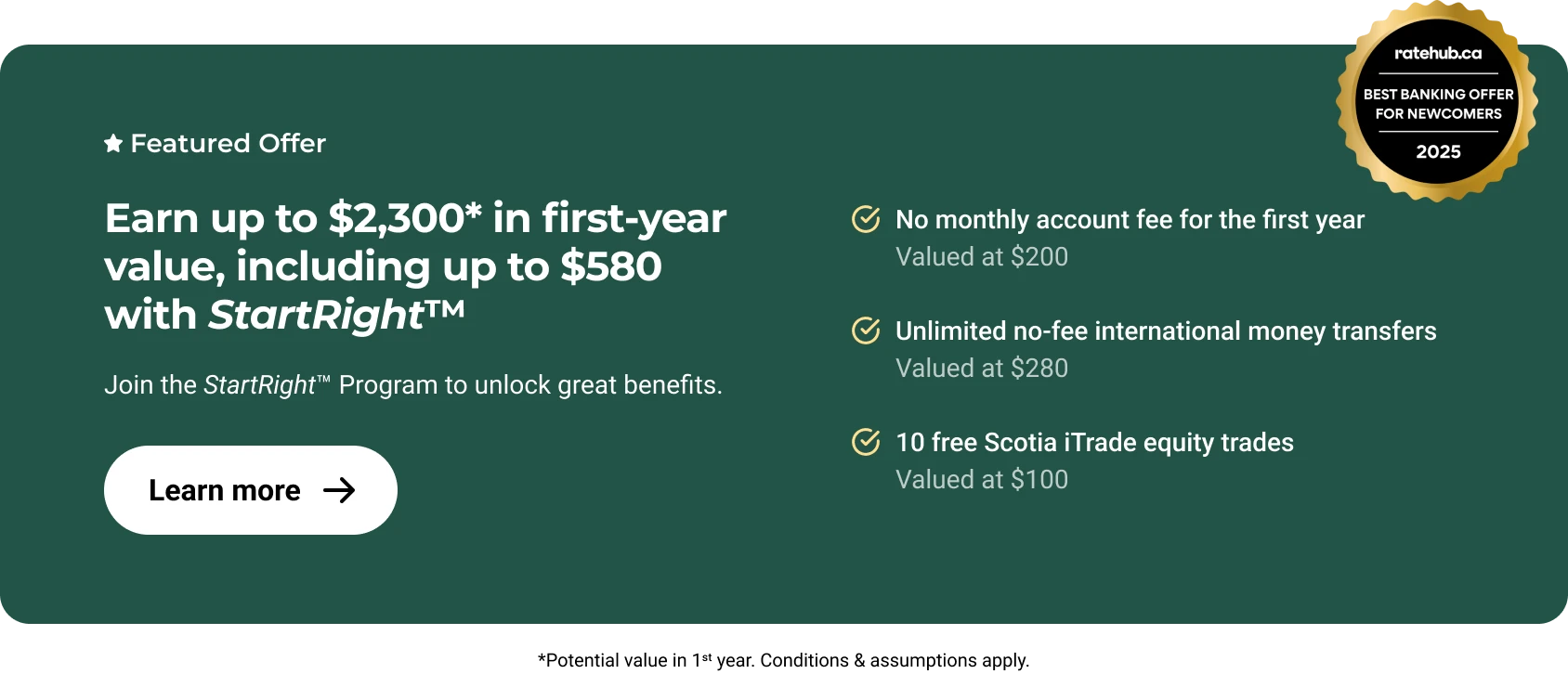

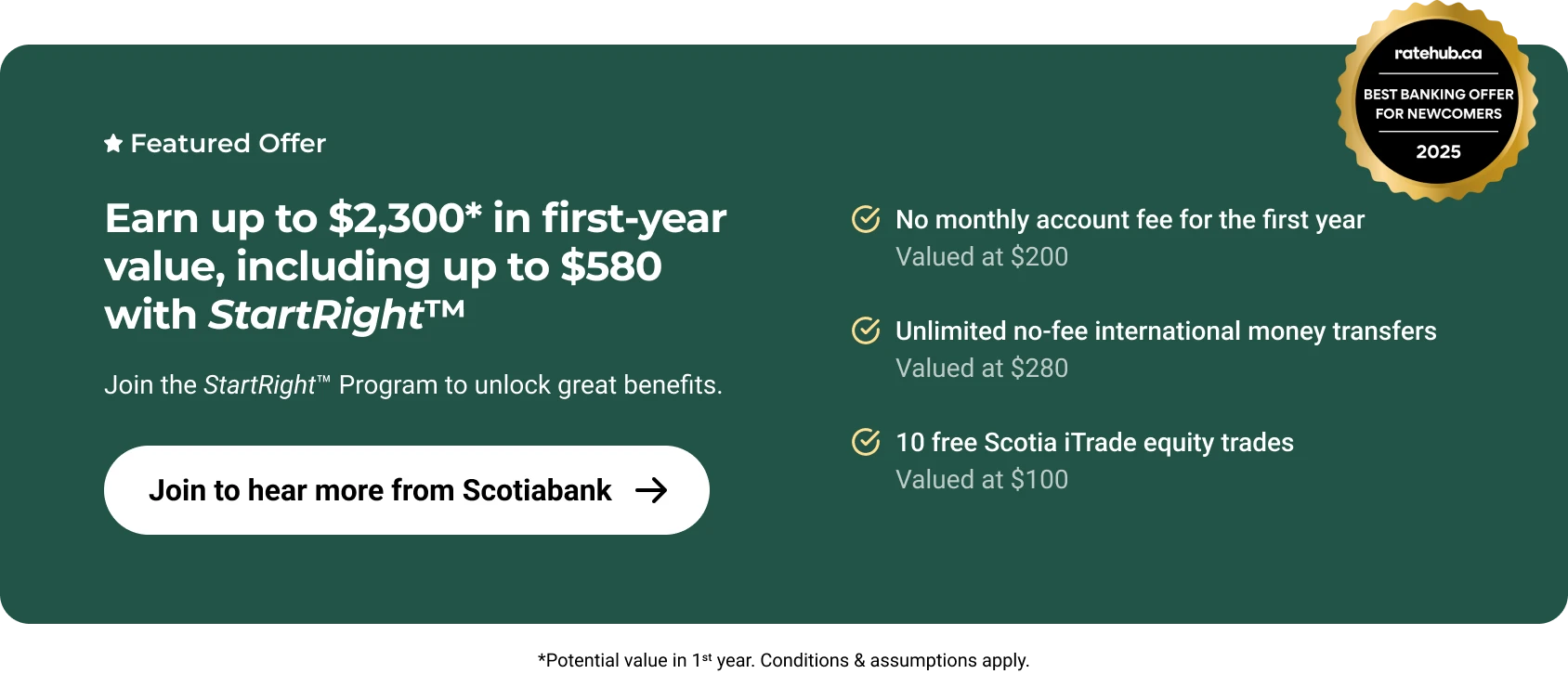

Save for Your Child’s Bright Future with Scotiabank

If you’re ready to open a RESP, TFSA, or other financial vehicle to help you save for your child’s education, it’s wise to evaluate your options and make decisions that suit you sooner rather than later. The earlier you establish your account, the easier it will be to start saving slowly and surely to make it possible for your child to pursue higher education.

The advisors at Scotiabank are available online, over the phone, and in person to talk you through the process. They can offer personalized advice based on your unique needs and will work with you to set up a savings plan that offers as many advantages as possible.

Reach out today to book your appointment.

Legal Disclaimer

About the author