Updated on April 20, 2026

This content is sponsored by Scotiabank. The views, opinions, and information expressed in this piece are those of Moving2Canada and do not reflect those of Scotiabank. Scotiabank is not responsible for the content, accuracy, or any representations made herein.

Do you dream of buying your very own home in Canada?

You’re not alone. Around one in five homes in Canada is purchased by newcomers.

So, how to buy a house in Canada as a newcomer?

The first step to making your home ownership dream a reality is to learn as much as you can about the specifics of buying a home in Canada.

In this article, we’ll go over Canadian mortgages, what to consider when deciding on a location for your home, and a summary of the important steps to buying your first home in Canada.

The first question: What can you afford?

Before you start planning, it’s important to consider your financial situation.

Homebuyers will need to make a down payment on their home. In Canada, the minimum down payment is between 5% and 20% of the purchase price. However, if your down payment is less than 20% of the purchase price, you will need to buy mortgage default insurance. It is also worth noting that if you are buying a home valued at more than $1.5 million CAD, you are required to put at least 20% down.

You should also know when you buy a home you’ll have to budget for things like property taxes, land transfer taxes, and closing costs. You may also want to arrange for property insurance as well.

If you would like to know how much of a mortgage you can afford, Scotiabank offers to help estimate the maximum purchase price you can likely manage based on your financial situation. Contact a Scotiabank Home Financing Advisor for advice on buying your first home.

How to save for a down payment

Putting money aside can be tricky. Thankfully, there are options available to help you save for your first home.

For instance, if you take advantage of a Registered Retirement Savings Plan—more commonly known as an RRSP— you can increase your home-buying power.

Keep in mind, there are annual limits to how much money you can put into an RRSP. In addition, if you take money out of an RRSP, you will be taxed on that amount. However, thanks to Canada’s First Time Home Buyer’s Plan, you can take out up to $60,000 ($120,000 for a couple) and use it toward a down payment on a new home. You will not have to pay taxes on this withdrawal as long as you repay it within 15 years.

The mortgage pre-approval process in Canada

Before you get a mortgage in Canada, you may go through a mortgage pre-approval process. A pre-approval is when a mortgage lender determines the maximum amount they will lend you, based on your finances. The actual amount you get may vary depending on the value of your home, as well as the amount of your down payment.

The pre-approval is typically valid from 60 to 120 days before the offer expires. While a pre-approval isn’t necessary, it may be helpful to know what price range you should consider when you are looking for a new home. It will also help you know how much of an offer you can make on a property.

A pre-approval can also help make the mortgage application process easier since you already shared much of the information at the pre-approval stage that will be required when you apply.

When you are ready, a Scotiabank Home Financing Advisor can help you start the mortgage pre-approval process. Contact Scotiabank to speak with a Home Financing Advisor.

Mortgages in Canada

Although the concept of mortgages is more-or-less the same from country to country, you’ll want to know the specifics of how mortgages work in Canada.

It is important to note that Canada has certain credit and other qualification requirements for mortgages. For you, that could mean that even if you have a similar income as you did in your home country, you might not qualify to borrow the same amount in Canada.

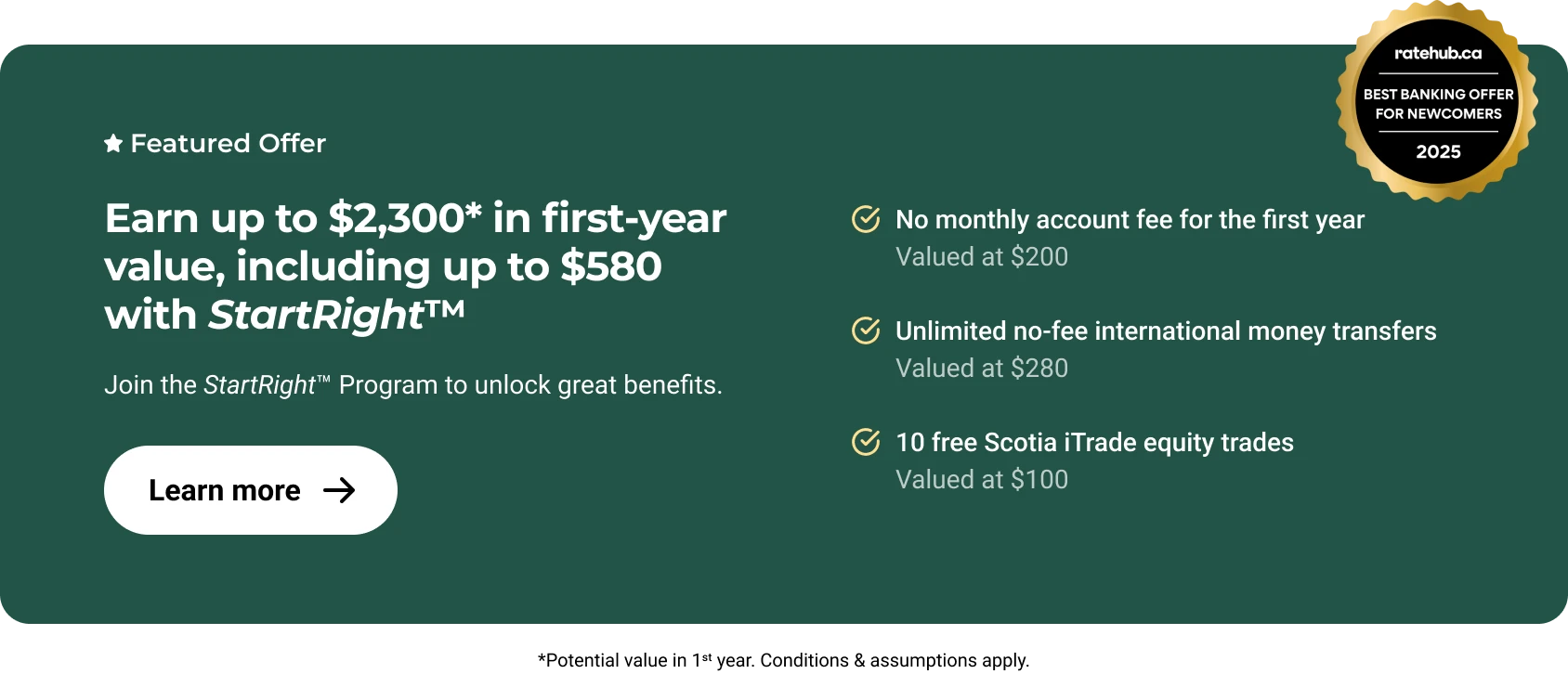

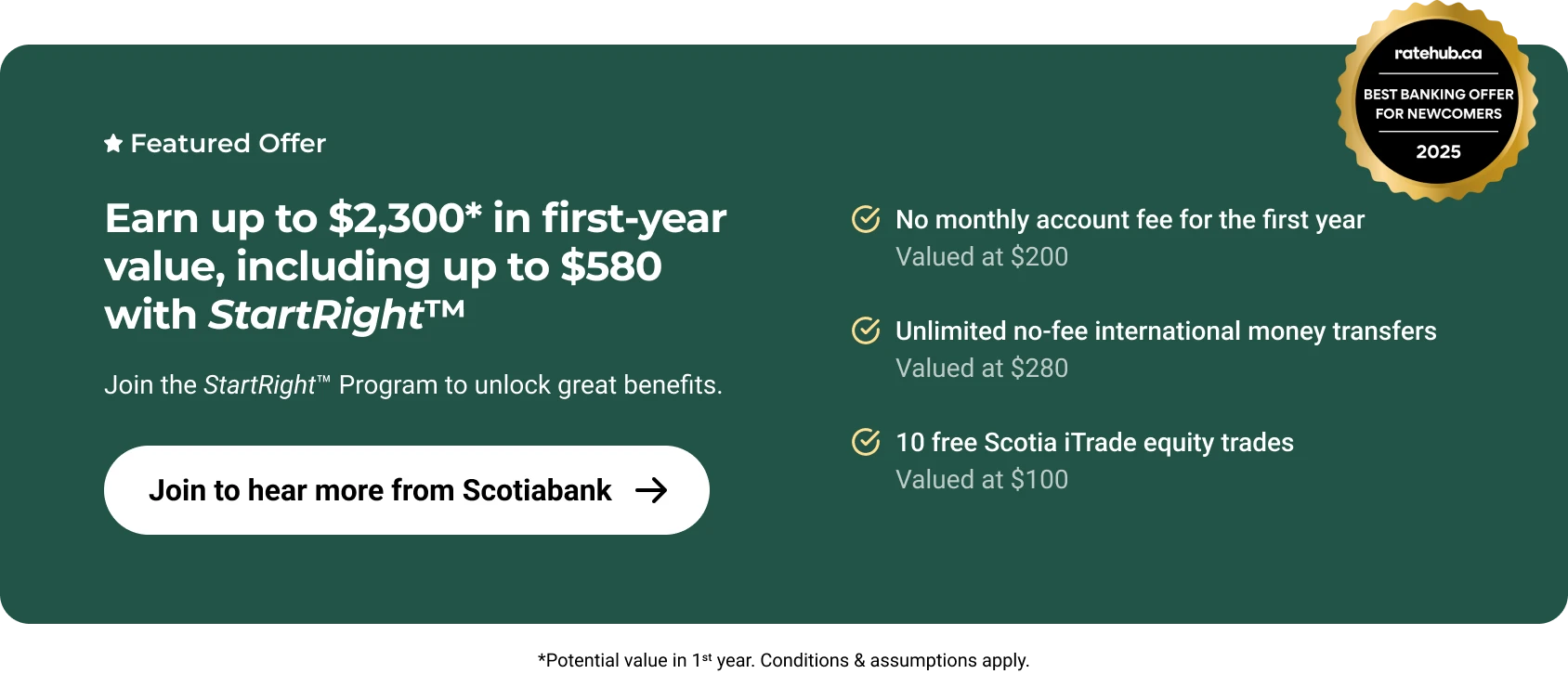

Unlike some countries, Canada has a credit scoring system that determines a person’s credit trustworthiness. One of the ways you can start building credit in Canada is by having a Canadian credit card. With Scotiabank’s StartRight® Program for newcomers, you may be eligible for a credit card without any previous credit history¹. Learn more about Scotiabank’s StartRight® Program. 2

Also in Canada, loans may be amortized up to 30 years, but loan terms are limited to shorter periods of time. While the amortization period refers to the entire lifetime of your mortgage, how long it will take to pay off completely, the term is the length of your current contract, which must be renewed. This is different from the U.S., for example, where your mortgage term may be the same length as your mortgage.

To learn more about mortgages in Canada, contact a Scotiabank Home Financing Advisor

Location, location, location

Part of the process of buying a home includes finding the right community to live in. This will principally depend on your financial situation, as well as your lifestyle preferences.

Big cities will have more expensive housing prices than smaller cities and rural areas. However, homes further away from commercial areas may incur increased transportation costs.

As a newcomer, you will likely want to learn about the neighbourhoods of your new city to determine which may suit your needs. You’ll likely want to research whether living in an urban, suburban, or rural area will make more sense for you. Other factors you may want to consider include public transportation, access to community and cultural activities, and proximity to schools and other facilities for children.

On top of all that, you may wish to know how safe the area is, and about how weather conditions affect the quality of life there. For example, if you would like to buy something that is in a known flood or fire zone, you may wish to consider what steps you may need to take to protect yourself and your property.

Types of homes in Canada

The type of home you are looking for will also affect its price. Here are some of the types of homes you can buy in Canada:

Condo/Condominium: A condo may look like a building or complex from the outside, but each unit is owned by an individual. The structure or complex itself as well as common areas may be owned by another entity. Condos are popular in big city centres.

Single/Detached: A detached home is a single dwelling located on its own property. The house does not share walls with neighbouring properties. If you buy a single detached home, you own the building and the property surrounding it. This is oftentimes the most expensive type of housing in Canada, but it is also highly desirable.

Semi-Detached: A semi-detached home has its own land and entrance but shares a wall with a neighbouring dwelling.

Townhouse: Townhouses are attached to other homes on both sides. They are also commonplace in many major Canadian cities.

Duplex/Triplex: A duplex is a single building that has been divided into two units, whereas a triplex is the same but divided into three. These properties can be attractive for some buyers because they can rent out the other units.

Support for home buyers in Canada

You may also choose to work with a real estate professional to help you find your dream home. There are many options in Canada. You may work with a real estate agent, access real estate services online, or buy privately without professional help.

Although the private option is available, many home buyers opt for an expert, such as a lawyer or notary, to go over the paperwork before signing the deal (this may be mandatory in certain jurisdictions). You will want to make sure that you understand the details of your mortgage agreement, especially as a newcomer to Canada. There are scammers in the industry who may try to take advantage of newcomers or who may have limited knowledge of how real estate transactions work in Canada.

Make an offer on a home in Canada

Once you have decided on a home, you or your real estate agent can make an offer. The offer may include:

- The closing date, which is the date that you will transfer ownership and be required to pay for the home;

- The total amount you agree to pay for the home;

- A deposit amount, which you pay when you make an offer to show that your offer is serious. It is usually between 1% and 3% of the sale price;

- A request for a current land survey of the property that shows the bounds of the property you’re buying;

- A home inspection report done by an expert that speaks to the condition of the property; and

- A list of items, such as appliances, that you would like included in the purchase price.

After you submit the offer, the seller may come back with a counteroffer that includes revisions to the deal. This process makes it so the agreement works for both parties.

Get a mortgage in Canada

After the offer is agreed upon, it’s time to get a mortgage.

If you went through the pre-approval process with Scotiabank, you can now go back to your Scotiabank advisor. They will collect the necessary documents required to confirm the information that your pre-approval was based on, such as your income and down payment. They will also confirm the value of your property.

There are many different ways to get a mortgage and a variety of mortgage products to choose from. Talk to your Scotiabank advisor about what’s right for you as a first-time home buyer in Canada.

Get a home inspection in Canada

It is also important to have your new home inspected by a professional inspector. Some of the things a home inspector will look for include mold, roof conditions, plumbing, electrical systems, and more.

Although almost anyone can claim to be a home inspector, most provinces have associations that require inspectors to meet professional standards. The Canadian Association of Home and Property Inspectors (CAHPI) contains more information about home inspectors.

You can find out about inspectors in your province at the following webpages:

- Alberta

- British Columbia

- Manitoba

- New Brunswick

- Newfoundland and Labrador

- Nova Scotia

- Ontario

- Prince Edward Island

- Quebec

- Saskatchewan

Finalize the sale

The final step in the process of buying a first home in Canada is the day you close the sale. Usually, you will meet with a lawyer who will ensure that all legal and mortgage documents are signed, the home is registered in your name, and that the down payment is transferred to the person selling the home.

Closing day is also the day you get the key to your new home.

Step-by-step instructions

To summarize the above into simple steps:

- Save for a down payment

- Figure out what you can afford

- Get pre-approved for a mortgage

- Choose a location

- Decide on professional help

- Make an offer

- Get a mortgage

- Schedule a home inspection

- Finalize the sale

One final note before you go—you do not have to go on your first home-buying journey alone. Scotiabank Home Financing Advisors are available to provide you advice and solutions at any point during the process.

Looking to buy a home in Canada? Speak to a Scotiabank Home Financing Advisor.

Legal Disclaimer

1 Subject to credit approval. To be eligible, you must be a participant in the Scotiabank StartRight® Program. To qualify for a credit card, you must be a resident of Canada and the age of majority in your province/territory where you live. Your approval for a credit card and the credit assigned will be determined based on Scotiabank’s credit criteria, including your verifiable income and credit history (if available). The credit amount of up to $15,000 under the Scotiabank StartRight® Program is subject to change by Scotiabank from time to time without prior notice. A credit history in Canada is not required in order to be eligible for a credit card under the Scotiabank StartRight® Program.

2 Scotiabank StartRight® Program is available only for Canadian Permanent Residents from 0-5 years in Canada and Foreign Workers.

About the author