Updated on July 23, 2026

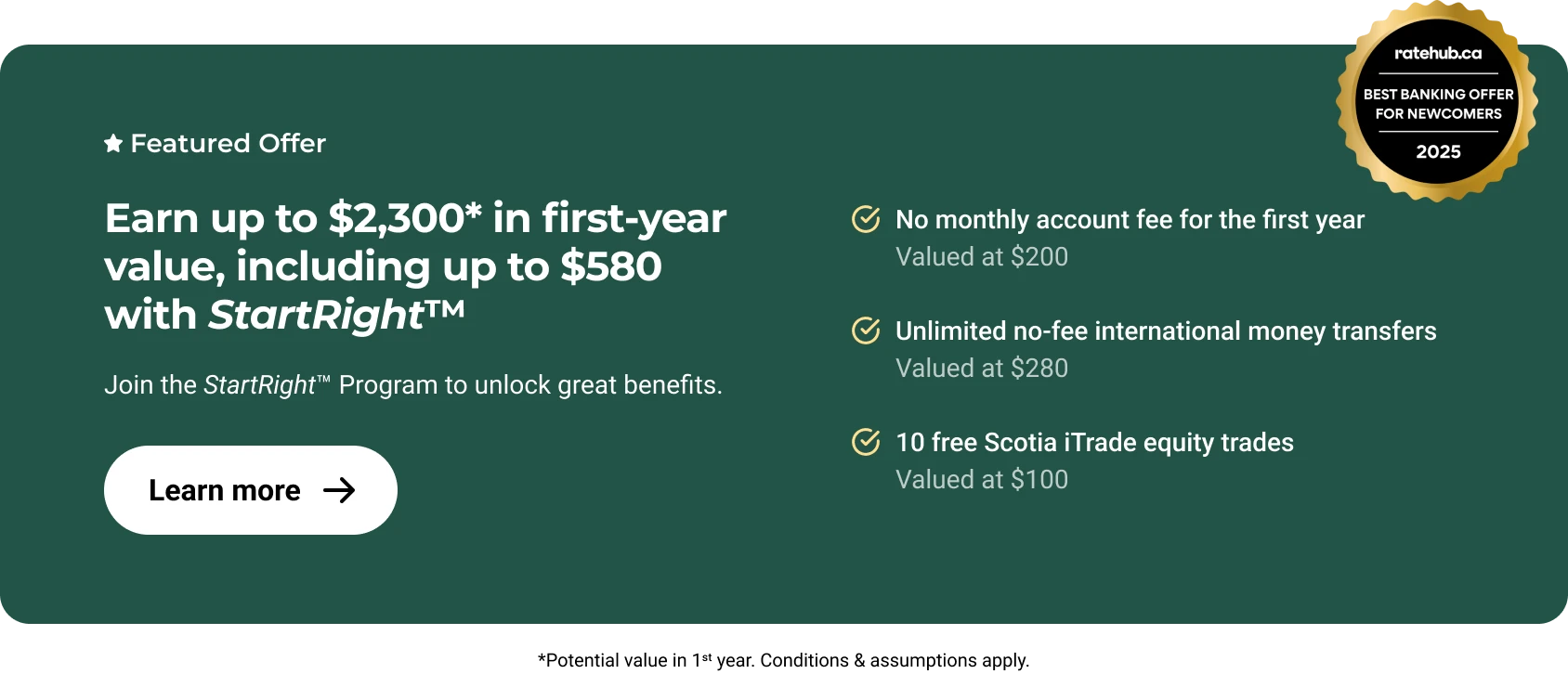

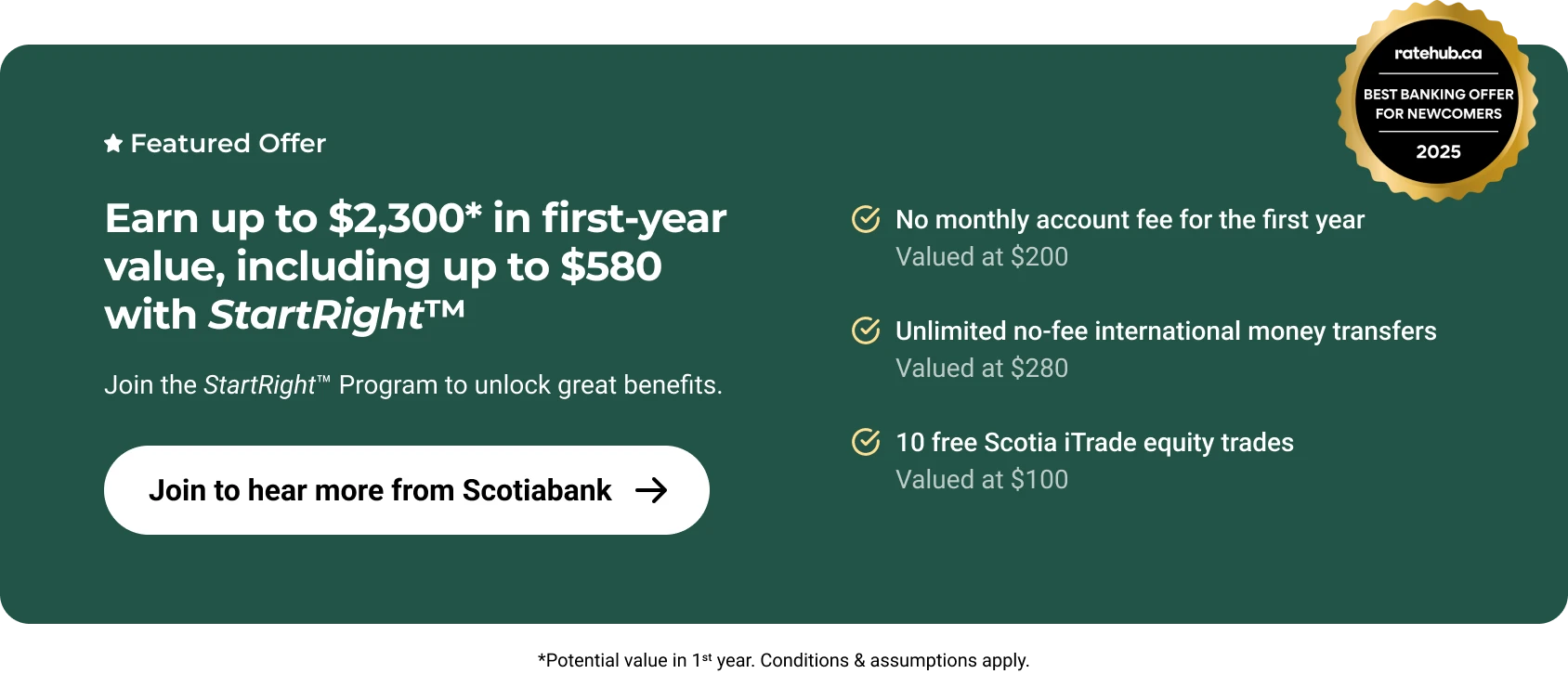

This content is sponsored by Scotiabank. The views, opinions, and information expressed in this piece are those of Moving2Canada and do not reflect those of Scotiabank. Scotiabank is not responsible for the content, accuracy, or any representations made herein.

Moving to Canada comes with big financial decisions. From learning how to budget in a new currency to figuring out where to put your savings, you’ve got a lot on your plate. But here’s the good news: Canada’s financial system is designed to help you grow your wealth, and with the right strategies, you can make it work for you.

Whether you’re saving for a down payment, planning for retirement, or securing your family’s future, investing can help you build financial stability over time. Let’s explore how you can get started, including the best accounts for newcomers, how much to invest, and the platforms available in Canada to help you grow your money.

What Are the Best Accounts for Investing in Canada?

Canada offers many different types of tax-advantaged accounts in which you can invest if you choose, including: the Tax-Free Savings Account (TFSA), the Registered Retirement Savings Plan (RRSP), and the Registered Education Savings Plan (RESP).

Here’s a quick overview:

Tax-Free Savings Account (TFSA): No Tax, More Growth

When you first become a tax resident in Canada, opening a Tax-Free Savings Account (TFSA) should be a top priority. This flexible account is especially valuable for newcomers who may need access to savings as they settle in Canada.

As the name suggests, a TFSA lets your investments grow tax-free. You can use it for any goal—buying a car, retirement, a vacation, or even an emergency fund.

- Annual Contribution Limit: Your annual limit resets each year, with unused room from previous years carrying forward.

- Superpower: Income earned is tax-free, withdrawals aren’t taxed, and they don’t count as income.

- Best For: Short-term or long-term goals. It’s generally wise to maximize your TFSA contributions if possible.

Learn more about TFSAs for newcomers, or calculate your TFSA contribution room here.

Registered Retirement Savings Plan (RRSP): Save Now, Enjoy Later

If you’re focused on retirement savings, the Registered Retirement Savings Plan (RRSP) is essential. Contributions to an RRSP lower your taxable income, which can mean a smaller tax bill or a larger refund. This can be particularly useful for newcomers building a financial foundation.

- Annual Contribution Limit: 18% of your earned income (up to an annual government-set maximum).

- Superpowers:

- Contributions are tax-deductible, reducing your taxable income.

- Investment growth is tax-deferred until withdrawal, usually at retirement when your income and tax rate are lower.

- You can withdraw up to $35,000 through the Home Buyers’ Plan (HBP) to purchase your first home.

- Best For: Long-term savings, like a retirement plan, especially if you’re currently in a higher income bracket.

Read more about RRSPs for newcomers.

Registered Education Savings Plan (RESP): Invest in Their Future

If you’re thinking about your children’s future, the Registered Education Savings Plan (RESP) is an excellent tool. Contributions to an RESP grow tax-free, and the government matches 20% of your annual contributions (up to $500 per year) through the Canada Education Savings Grant (CESG). Over time, this adds up significantly when paired with investment growth.

- Superpowers:

- The government matches 20% of contributions, up to $500 annually, with a lifetime maximum of $7,200.

- Investment growth is tax-deferred, and education withdrawals are taxed at your child’s (lower) tax rate.

- Best For: Saving for your child’s university or college tuition.

Learn more about saving for your child’s future education.

Types of Investments In Canada

This is one of the biggest misunderstandings we see in Canada (amongst Canadian-born investors and newcomers alike). Many people think RRSPs, RESPs, and TFSAs are a type of investment. They aren’t. They are a type of tax-advantaged account.

You need to invest within the account to take advantage of compounded growth.

Do not make this major investing mistake

If you just put money in a TFSA, RRSP, and RESP or similar account, it won’t automatically grow. It actually won’t do anything. You need to buy investment products within the account for your money to grow over time.

Here’s a quick overview of some types of investments to help you decide which option might suit your goals.

Guaranteed Investment Certificates (GICs): Low-Risk, Low Return

When you invest in a GIC, you’re essentially lending money to a financial institution for a fixed term, and in return, they pay you a guaranteed interest rate.

- Best For: Conservative investors or short-term savings goals (30 days to 5 years).

- Pros: Relatively low risk and predictable returns.

- Cons: Returns are typically lower than other investment options and may not keep up with inflation.

Exchange-Traded Funds (ETFs): Diversified and Cost-Effective

ETFs are baskets of investments, like stocks or bonds, that you can buy and sell. They’re similar to mutual funds but usually come with lower management fees and greater flexibility. ETFs can track specific market indexes (e.g., the S&P/TSX Composite Index) or focus on particular sectors or regions.

- Best For: Investors looking for diversification.

- Pros: Low fees, easy to trade, and can provide diversified exposure to a range of assets, depending on the type of ETF being purchased.

- Cons: Returns depend on market performance, past performance is not a guarantee of future performance, and you need a brokerage account to trade them.

Mutual Funds: Professionally Managed Growth

Mutual funds pool money from multiple investors and are managed by professionals who invest in a mix of securities. They offer diversification and the potential for long-term growth without requiring you to manage the investments yourself.

- Best For: Investors looking for growth but who prefer not to make individual investment decisions.

- Pros: Professional management and diversification reduce risk.

- Cons: Returns depend on market performance, and there can be fees associated with management.

Stock Market Investing: High Risk, Potential for High Reward

Investing directly in the stock market offers the potential for higher returns, but it comes with significantly increased risk. Stocks represent ownership in a company, and the value fluctuates based on the company’s performance and market conditions.

- Best For: Confident and experienced investors willing to take on risk for the chance of higher returns. Ideally, for those who can afford to ‘lose’ the money if the stock doesn’t perform well.

- Pros: Potential for above average growth and flexibility in choosing investments.

- Cons: High risk, low diversification, requires knowledge of the market and time to monitor and balance investments.

Other Options to Consider

- Bonds: Fixed-income investments where you lend money to a company or government and receive interest payments. Bonds are generally safer than stocks but offer lower returns.

- Real Estate: Investing in property can provide stable income and long-term growth but requires significant upfront capital and ongoing management.

Choosing the Right Investment as a Newcomer to Canada

The best investment option depends on your goals, timeline, and risk tolerance. If you’re a newcomer to Canada, start by understanding your financial priorities. For example, you might choose to put your money in a GIC while you get more comfortable with Canada’s financial system. Ultimately, you will likely want to move your money into the market (ideally through diversified funds) to make it grow over time.

No matter where you start, educating yourself and setting clear goals are key to making your money work for you. Investments grow over time, so the earlier you start, the better your results.

How Much Should You Invest?

A good rule of thumb is to invest 10–20% of your income, depending on your financial goals. Here’s how to decide:

- Start Small: If you’re paying off high-interest debt or adjusting to new costs of living, start with a small manageable contribution each month. Alternatively, consider paying off high-interest debt before investing, as returns on investments may not outpace debt interest rates.

- Long-Term Goals: Save more aggressively (15–20%) if you want to build wealth faster or bridge the retirement gap that newcomers often face.

- Balance Is Key: If you’re building an emergency fund, paying off debt, or saving for a home, balance these priorities while still contributing to investments.

Not sure how to balance savings—or feeling guilty for not doing enough? You’re not alone. The key is starting where you are and building from there. Read our article How To Overcome Savings Guilt By Mastering the Different Types of Savings in Canada, and take your first step toward confident, guilt-free financial planning.

The Power of Compounding Growth

Inflation causes the cost of goods and services to rise over time. Leaving money in a standard savings account won’t help it grow due to low interest rates that often don’t keep up with inflation. Investing allows your money to grow over time, thanks to compounding.

For example, starting with an initial $5,000 investment and contributing $5,000 annually with an average annual return of 7%, here’s how your money could grow over 30 years:

- After 10 years: nearly $98,000.

- After 20 years: approximately $257,000.

- After 30 years: surpassing $528,000.

This demonstrates how consistent investing and time can transform your savings. As a newcomer, starting early—even with small amounts—can yield results. Use this investment calculator to see how your savings could grow, with different rates of return. But, consider consulting a qualified investment professional for personalized guidance.

Investment Platforms in Canada

Choosing where to invest is crucial. Many newcomers opt for their bank for convenience, as banks offer in-person support and integrated financial systems. However, managed investments through banks typically come with higher fees due to management services.

If you prefer a more hands-on approach, consider self-directed platforms. These platforms allow you to invest in stocks, ETFs, and other securities, but they usually require more financial knowledge and confidence.

Tips for New Investors

- Start Early: The sooner you begin, the more time your investments have to grow. Even small monthly contributions can have a significant impact over time.

- Diversify: Spread your money across different asset types (e.g., GICs, bonds, ETFs) to manage risk effectively.

- Automate Contributions: Set up regular contributions to your TFSA or RRSP to build wealth consistently without needing to think about it.

- Learn as You Go: Take time to understand your investments through online research or by consulting a financial advisor.

- Don’t Take Unnecessary Risks: Investing isn’t gambling if approached wisely. Avoid day trading or single-stock investments as a beginner, as most people (97%) who try day trading lose money. Focus on safer options like ETFs to minimize risks.

Discover easy, practical steps to start saving today in our article How to Start Building Your Savings Accounts.

Takeaway: Investing Is Accessible

Investing in Canada might feel overwhelming at first, but with the right tools and a bit of knowledge, you can transform your income into long-term financial security. Whether you start small with a TFSA or focus on RRSPs for retirement savings, each step brings you closer to your financial goals.

Ready to begin? There’s a famous saying that goes: The best time to invest was yesterday. The second-best time is today.

Legal Disclaimer

Related articles

New Canada Child Benefit Payment Coming August 20. Here’s How Much You’ll Get.

Read more

New Alberta Child and Family Benefit (ACFB) Payment Coming August 27

Read more

New Ontario Trillium Benefit Payment Coming on August 10: What Newcomers Should Know

Read more

New CRA Benefit Payments in August 2026: What Newcomers Could Get

Read more

About the author