Updated on June 30, 2026

This content is sponsored by Scotiabank. The views, opinions, and information expressed in this piece are those of Moving2Canada and do not reflect those of Scotiabank. Scotiabank is not responsible for the content, accuracy, or any representations made herein.

As a Newcomer to Canada, you likely want to save for the future – and you might even want to start planning for retirement. But you might face challenges with RRSPs, such as confusion about how they work, fear of locking away money, and not knowing when or how much you can contribute.

We’ve created this guide to help you overcome these common pain points. We’ll explore what RRSPs arе, their key features, invеstmеnt options, and contribution rules.

Additionally, we’ll compare RRSPs with other accounts like Tax-Frее Savings Accounts (TFSAs) to help you make informed decisions about your money.

RRSP: Key Takeaways

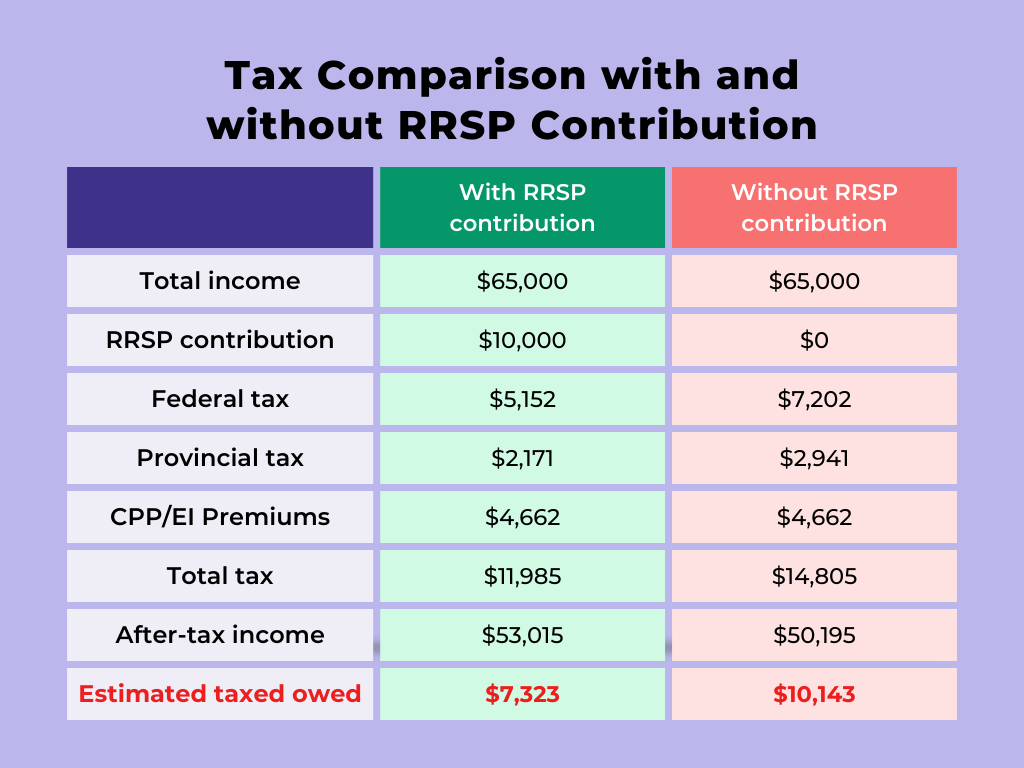

- Contributions to an RRSP reduce your taxable income, which can result in a tax refund or a lower tax bill.

- Investments in an RRSP grow tax-deferred, meaning you won’t pay taxes on any income earned inside the account (interest, dividends, capital gains) until you withdraw the funds, typically during retirement.

- You can contribute up to 18% of your previous year’s earned income, with an annual maximum set by the government (e.g., $33,810 for 2026).

- You have various investment options within your RRSP, including cash, GICs, mutual funds, ETFs, stocks, and bonds.

- Specific plans, such as the Home Buyers’ Plan and Lifelong Learning Plan, allow tax-free withdrawals for home purchases and education, with conditions.

- We hosted a webinar with our partner Scotiabank discussing how to build wealth as a newcomer. Watch it for detailed information about tax-advantaged accounts in Canada, including RRSPs.

This article is not individual financial advice

The information contained in this article is intended to be educational. It is not individual tax or financial advice. If you’re unsure about what’s best for you, you should consult with a qualified tax or financial advisor in your province or territory.

What Is A Registered Retirement Savings Plan (RRSP)?

An RRSP (Registered Retirement Savings Plan) is a Canadian government-registered account designed to help people save for retirement. You can invest in a wide range of products within your RRSP, including cash, GICs, mutual and index funds, ETFs, stocks and bonds.

Contributions to an RRSP are tax-deductible, meaning they reduce your taxable income for the year, potentially giving you a tax refund. The money in the account grows tax-free until you withdraw it in retirement, at which point it’s taxed as income.

For newcomers, contributing to and investing within an RRSP can help you build retirement savings. It’s worth bearing in mind that your RRSP reduces your taxes payable today, but taxes on the future withdrawals need to be compared to the benefit of tax-free withdrawals from TFSAs. Spending time understanding these nuances can be a crucial element of your retirement planning in Canada.

Can Newcomers Contribute To A RRSP?

In short – most likely yes IF you’ve been in Canada for long enough to find work, establish tax residency, and file taxes. Eligibility is based on your tax residency, age, and income.

To contribute to a Registered Retirement Savings Plan (RRSP) in Canada, you must meet the following requirements:

- Age: You must be under 71 years old.

- Residency: You need to be a Canadian resident for tax purposes.

- Income: You must have earned income.

- Tax Filing: You need to file a tax return.

You can open an RRSP at any age, though there are some limits and restrictions from the CRA and banking institutions for anyone under the age of 18 looking to establish an RRSP.

RRSP Contribution Limits

Each year, you can contribute either the annual contribution limit or 18% of your taxable income from the prior tax year, whichever is higher.

In other words, in 2025, if you earn $180500 or higher, you may be eligible to contribute $32,490 to your RRSP. If you earn less than this amount, you will be able to contribute up to 18% of your taxable income.

If you’re unsure, your online CRA account will show you your contribution limits.

| Year | RRSP Dollar Limit |

|---|---|

| 2026 | $33,810 |

| 2025 | $32,490 |

| 2024 | $31,560 |

| 2023 | $30,780 |

| 2022 | $29,210 |

| 2021 | $27,830 |

| 2020 | $27,230 |

| 2019 | $26,500 |

| 2018 | $26,230 |

| 2017 | $26,010 |

| 2016 | $25,370 |

| 2015 | $24,930 |

| 2014 | $24,270 |

| 2013 | $23,820 |

| 2012 | $22,970 |

| 2011 | $22,450 |

| 2010 | $22,000 |

| 2009 | $21,000 |

| 2008 | $20,000 |

| 2007 | $19,000 |

| 2006 | $18,000 |

| 2005 | $16,500 |

| 2004 | $15,500 |

| 2003 | $14,500 |

| 2002 | $13,500 |

| 2001 | $13,500 |

| 2000 | $13,500 |

| 1999 | $13,500 |

| 1998 | $13,500 |

| 1997 | $13,500 |

| 1996 | $13,500 |

| 1995 | $14,500 |

| 1994 | $13,500 |

| 1993 | $12,500 |

| 1992 | $12,500 |

| 1991 | $11,500 |

| 1990 | $11,500 |

RRSP Contributions: Key Facts and Strategies

Contributions can be made throughout the year or within 60 days into the following year. Several factors, such as Pension Adjustments and unused deduction room, can affect how much you can contribute. Over-contributing by more than $2,000 results in a 1% penalty per month on the excess amount.

Quick Tips

- Contribution Limit: Annual statutory limit or 18% of previous income, whichever is lower.

- Contribution Timing: Monthly, yearly, or lump sum contributions are allowed within 60 days of the prior tax year. (In other words, your contributions in January and February can be attributed to the previous tax year.)

- Carry Forward: Unused contributions can be carried over into future tax years.

- Over-Contribution Penalty: 1% per month on overcontributions higher than $2,000 within your lifetime.

How To Determine Your Contribution Room

If you want information about your RRSP contribution room, use the following services:

- CRA’s My Account for Individuals

- Your MyCRA mobile app

- Call the CRA at 1-800-959-8281.

When Can I Take Money From My RRSP?

The reality is that you can take money from your RRSP at any time. However, there will be tax consequences for doing so. As a result, it’s usually a good idea to get financial advice before making withdrawals. Broadly, here are some ways people make withdrawals from their RRSP:

- Homе Buyеrs’ Plan (HBP) & Lifеlong Lеarning Plan (LLP): Thе HBP allows first-timе homе buyеrs to withdraw up to $35,000 from thеir RRSPs to purchasе a homе without immеdiatе tax implications. Similarly, thе LLP allows you to withdraw up to $10,000 pеr yеar to financе your еducation, with specific rеpaymеnt tеrms.

- RRIFs: You can convert your RRSP into a Registered Retirement Income Fund (RRIF). This is mandatory for any RRSP amounts you have at the end of the year in which you turn 71, but you can do it at any age before then.

- Withdrawing Your RRSP When Leaving Canada: You can withdraw your RRSP if you leave Canada. Howеvеr, withdrawals arе subjеct to Canadian incomе tax. You might also nееd to consider tax implications in your nеw country of rеsidеncе. This can be complex, and we suggest seeking individual tax advice.

What Are The Tax Benefits Of An RRSP?

Here’s a quick summary of some of the benefits of an RRSP:

- Tax-deductible contributions: Contributions to an RRSP lower your taxable income, which can reduce the amount of tax you owe for that year.

- Tax-deferred growth: Interest, dividends, and capital gains earned within an RRSP are not taxed until you withdraw the funds, allowing your investments to grow tax-free in the meantime.

- Income smoothing: RRSP withdrawals may be taxed at a lower rate in retirement, if you’re in a lower tax bracket at that time, which can help manage your tax burden over your lifetime.

- Spousal contributions: You can contribute to your spouse’s RRSP and take advantage of income-splitting in retirement, reducing overall taxes for the household.

- Home Buyers’ Plan (HBP): You can withdraw up to $60,000 from your RRSP to buy your first home without paying taxes, as long as you repay the amount within 15 years.

- Lifelong Learning Plan (LLP): RRSPs can also be used to pay for education or training, allowing you to withdraw funds tax-free if repaid over 10 years.

- Contribution carry-forward: If you don’t maximize your RRSP contributions in one year, unused room can be carried forward indefinitely, giving you flexibility for future contributions.

While RRSPs are mainly for retirement, they offer significant tax benefits and flexible withdrawal programs that can support major life purchases, education, or long-term savings strategies.

Should You Pay Into Your TFSA or RRSP?

This is a complex question and the answer will vary depending on your exact circumstances. But here are a few rules of thumb:

- If you have the funds to max out your TFSA, RRSP, and FHSA, it can be a good idea to do so.

- If you expect your future tax rate to be lower, RRSP contributions may be advantageous.

- If your employer offers a matching RRSP contribution program, you might consider taking advantage of the ‘free money’. (A 100% return is an excellent rate of return!)

- It might be advantageous to use your RRSP to save for your first home or Lifelong Learning Plan (depending on your unique situation).

Remember: You should seek independent advice from a wealth advisor for tailored guidance based on your unique circumstances.

The registered retirement savings plan offers numerous benefits for retirement planning, including tax dеductions, tax-dеfеrrеd growth, and flеxiblе invеstmеnt options. By understanding thе kеy features, contribution rules, and withdrawal implications, you can make informed decisions about how to bеst usе your RRSP.

For pеrsonalisеd advice tailorеd to your financial situation, consider consulting a financial advisor. Thеy can hеlp you navigatе thе complеxitiеs of RRSPs and othеr rеtirеmеnt savings options, еnsuring you achiеvе your financial goals.

Struggling with savings guilt? You’re not alone, but you can take control. Start building confidence and explore the smartest ways to save.

Read our article: How To Overcome Savings Guilt By Mastering the Different Types of Savings in Canada — and take your first step toward guilt-free saving today.

More Resources About Retirement in Canada

- Preparing for retirement must also include a plan for your health in retirement. We have prepared a full article about this planning here: “What Are Your Options for Canada Health Insurance in Retirement?”

- Financial planning for retirement: How to Create Long-Term Wealth & A Retirement Plan

Legal Disclaimer

Related articles

Immigrants Start Behind Financially, But Many Catch Up Within a Decade, StatCan Finds

Read more

Smallest-Ever Express Entry Draw Held for Skilled Military Recruits Category

Read more

Best IEC Health Insurance for Canada (2026): Compare UK Providers

Read more

IRCC Issues 5,000 ITAs in French Express Entry Draw; Crosses 100K Mark for 2026

Read more

About the author