Updated on March 9, 2026

This content is sponsored by Scotiabank. The views, opinions, and information expressed in this piece are those of Moving2Canada and do not reflect those of Scotiabank. Scotiabank is not responsible for the content, accuracy, or any representations made herein.

For newcomers to Canada, financial stress is common. You may need to adjust to a new culture (yep – that extends to money), new housing and living costs, an entirely new banking system, and maybe even a change in income.

If you’re feeling stressed about money, you’re not alone—and there are proactive steps you can take to ease financial worries. One key step that some financial experts recommend is establishing an emergency fund.

Here’s why an emergency fund can be essential, especially for newcomers to Canada, and how you can get started building one—even if it feels overwhelming right now.

Key Takeaways About Emergency Funds

- An emergency fund is money you save to spend in case of emergencies, such as a job loss, unexpected home repair, or car accident.

- A fully-funded emergency fund usually has 3-6 months of living expenses – but it’s okay to start smaller.

- You can get advice straight from the Canadian government about emergency funds here.

Why an Emergency Fund is Important

Life can be unpredictable, and unexpected expenses—whether it’s a car repair, a temporary job loss, or medical expenses that aren’t usually free in Canada (like dental)—can happen to anyone.

Without an emergency fund, these costs might push you into debt, which quickly snowball and make financial stress even worse. An emergency fund acts as a safety net.

This is why financial commentators like Paula Pant, Renee Sylvestre-Williams, Ramit Sethi, Mr. Money Mustache, and many others agree that having an emergency fund is important. All of these personal finance personalities advise that an emergency fund can help you handle the financial surprises life throws at you.

Knowing you have a financial cushion can reduce stress, helping you focus on building your new life and career instead of worrying about what might go wrong.

How Much Should You Save?

The Canadian government suggests saving three to six months’ worth of living costs. Living costs include core expenses necessary to maintain a basic standard of living, such as housing, food, transport, insurance, basic phone/internet bills, utilities, and possibly childcare. This does not include ‘wants’ like dining out, subscriptions, renovations, or travel.

Here’s how to calculate what you need for an emergency fund:

Step 1: Calculate Your Monthly Essential Living Costs

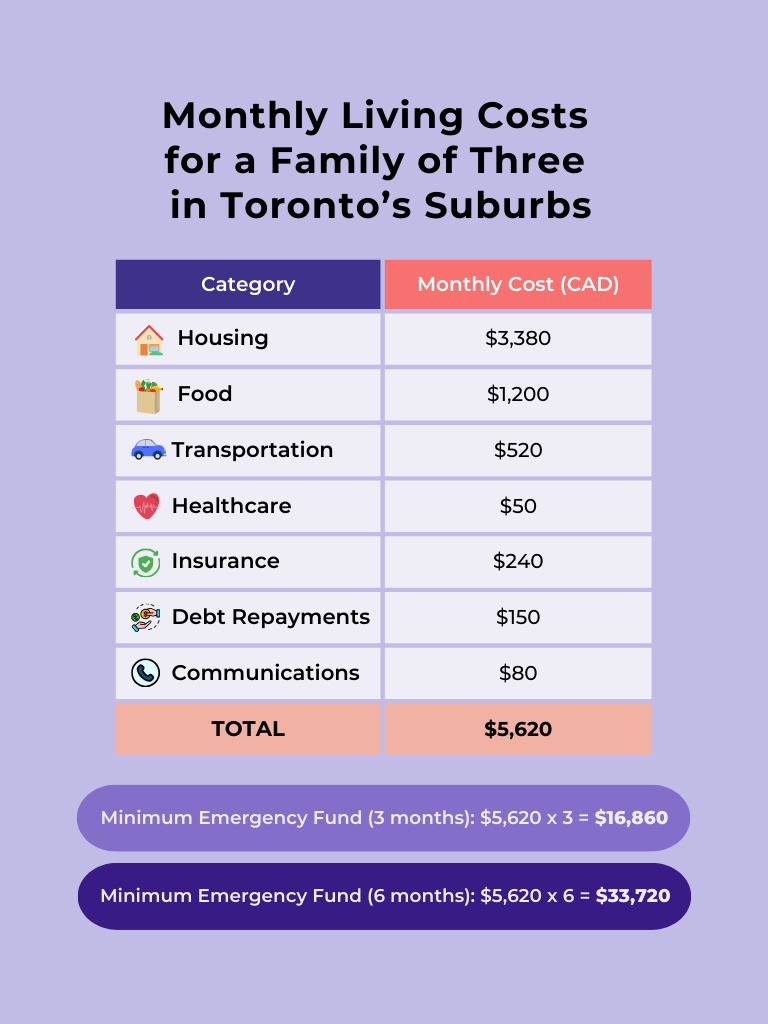

Here’s an example for a family of three (two adults, one school-aged child) living in an apartment in the outskirts of Toronto:

- Housing (Rent and Utilities)

Rent: $3,000

Utilities (electricity, water, heat): $200

Internet and phone (basic plans): $180

Total for Housing: $3,380

- Food

Groceries for three people: $1,200

Total for Food: $1,200

- Transportation

Gas: $100

Metro monthly passes x 3: $420

Total for Transportation: $520

- Healthcare

Prescription medications and over-the-counter essentials not covered by OHIP: $50

Total for Healthcare: $50

- Insurance

Life insurance: $50

Tenant insurance: $30

Car insurance: $160

Total for Insurance: $240

- Debt Repayments

Minimum payments on credit card debt or student loans: $150

Total for Debt Repayments: $150

- Communications

Cell phone plans for two adults: $80

Total for Communications: $80

Step 2: Calculate Emergency Fund Amount

Using the updated monthly total, we calculate the emergency fund to cover three to six months of essential living costs.

Minimum Emergency Fund (3 months of expenses): $5,620 x 3 = $16,860

Maximum Emergency Fund (6 months of expenses): $5,620 x 6 = $33,720

Recommended Emergency Fund Range

For this family, an emergency fund of $16,860 to $33,720 would provide a financial cushion. This range covers their essential living costs in case of unexpected events or income disruptions, helping them possibly avoid debt and maintain stability.

How To Save Your Emergency Fund

If saving three to six months of expenses feels intimidating, don’t worry—you don’t have to reach this goal overnight. Here’s a breakdown of how you could approach it:

Open a separate savings account

If everything is in one account, it’s hard to know what’s daily living costs and what your emergency fund looks like. Setting up a separate account for your emergency fund provides clarity.

Start small and build gradually

Start with a smaller, more manageable goal, like saving $1,000-$2,000 as your initial emergency fund. This amount may enough to cover minor, urgent expenses, like car repairs or a dental emergency.

Not sure how? Discover easy, practical steps to start saving today in our article How To Start Building Your Savings Accounts.

Tailor your fund to your family’s needs

Adjust your emergency fund goal based on your current stability and needs. If you’re just starting out in Canada and still figuring out monthly expenses, a three-month target might be a reasonable starting point. If you feel less financially secure due to being new at your job or because you have a baby on the way, consider aiming for a six-month cushion.

Reassess regularly

Reconsider your emergency fund goal routinely to ensure it still matches your financial situation and comfort level. It could be a good idea to consider it every six months, or at least annually.

Actionable Tips for Newcomers to Build an Emergency Fund

Building an emergency fund doesn’t have to be overwhelming. Here are some simple steps to get started:

- Automate Small Savings

Set up an automatic transfer to your emergency fund each month, even if it’s a small amount. Many Canadian banks allow you to create sub-accounts for specific goals, making it easy to separate these funds from everyday spending. Some even let you set up automated savings plans to put your emergency fund savings on autopilot.

- Track Your Spending to Identify Savings Opportunities

Track your expenses to see where your money goes each month. This can reveal areas to cut back and free up money for your emergency fund. For example, reducing non-essential costs like dining out or subscription services and then saving that money instead can make a big difference.

- Direct Windfalls to Your Fund

When you receive unexpected money, like a tax refund, bonus, or gift, consider adding it directly to your emergency fund. It’s a quick way to grow your savings without impacting your regular budget.

Plus, once you have your emergency fund saved, you might want to start using these windfalls to save for your future.

- Set Micro-Goals and Celebrate Small Wins

Building an emergency fund takes time, so set small goals, like reaching $500 or $1,000, and celebrate each win. Breaking it into milestones helps you stay motivated.

When To Spend Your Emergency Fund

Your emergency fund is there for emergencies – but what counts as an emergency worthy of your fund?

Here’s some criteria you might wish to use:

- It was an unexpected expense you hadn’t planned for.

- It is necessary (not a want).

- It must be paid for now (it’s not something you can put off until you’ve had time to save for it).

For example, an unexpected dental procedure is only partially covered by your healthcare provider and the pain is unbearable (i.e., you can’t put it off for six months and save for it).

FAQs From Newcomers About Emergency Funds

Building an emergency fund is just one step, but it’s a powerful one for reducing financial stress and increasing confidence. Financial Literacy Month is the perfect time to set yourself up for long-term financial security. By creating an emergency fund, you’re giving yourself the freedom to handle life’s ups and downs without resorting to debt or feeling overwhelmed by every unexpected cost.

Start small, be consistent, and remember that each contribution, no matter how small, brings you closer to financial stability. With a strong foundation, you’ll feel more secure and prepared to enjoy all the new opportunities Canada has to offer.

Got questions about emergency funds in Canada? See our FAQs below to see if we’ve answered yours.

I’m behind on my retirement planning as a newcomer to Canada. Should I invest my emergency fund?

Your emergency fund is usually held separately from your retirement accounts. It’s a safety net, not an investment.

You may want to put your emergency fund in low-risk, accessible accounts, like a high-interest savings account or a cashable GIC. This approach means your money can grow a little without taking on undue risk.

Is it better to pay off debt or build an emergency fund first?

It depends on your situation. Saving a small emergency fund (e.g., $1,000-$2,000) before focusing on debt repayment can give you a safety net for minor emergencies to prevent you from further going into debt. After that, you can balance debt repayment with growing your emergency fund based on your individual risk tolerance.

However, debt can accrue interest quickly, so it may make more mathematical sense to focus on the debt first. (Math is only part of your money equation, though!) It could be worth focusing on paying off debts first, especially if they’re accruing very high interest, like payday loans.

The best approach is usually the one you’ll stick with!

Can I use a credit card as my emergency fund?

Ultimately, it’s your money. But credit cards typically have high-interest rates, and you may end up paying more for your emergencies if you put it on a credit card than if you paid cash.

Our perspective? It’s never fun to pay for car repairs, but we’d prefer not to pay 21% interest on those costs.

For more tips on how to use your credit card, explore What You Can and Can’t Use a Credit Card For to better understand smart spending habits, common pitfalls, and make your credit work for you—not against you.

How do I know when to replenish my emergency fund?

If you need to dip into your emergency fund, make it a priority to rebuild it as soon as possible. Resume regular contributions to your emergency fund until it’s back to your target amount, so you’re prepared for future unexpected expenses.

Can I use my emergency fund for non-emergency expenses?

It’s usually best to reserve your emergency fund strictly for genuine emergencies, such as job loss, medical needs, or essential repairs. If you use it for non-emergencies, you risk not having funds available when a real emergency occurs. Plus, if you only use it for emergencies, you build better money management muscles by saving for your wants instead of always going for gratification.

Legal Disclaimer

¹ Scotiabank StartRight® Program is available only for Canadian Permanent Residents from 0-5 years in Canada and Foreign Workers.

² Subject to credit approval. To be eligible, you must be a participant in the Scotiabank StartRight® Program. To qualify for a credit card, you must be a resident of Canada and the age of majority in your province/territory where you live. Your approval for a credit card and the credit limit assigned will be determined based on Scotiabank’s credit criteria, including your verifiable income and credit history (If available). The credit limit amount of up to $15,000 under the Scotiabank StartRight® Program is subject to change by Scotiabank from time to time without prior notice. A credit history in Canada is not required in order to be eligible for a credit card under the Scotiabank StartRight® Program. Read more terms and conditions.

³ Subject to credit approval. To be eligible, you must be a participant in the Scotiabank StartRight® Program. To qualify for a credit card, you must be a resident of Canada and the age of majority in your province/territory where you live. Your approval for a credit card and the credit limit assigned will be determined based on Scotiabank’s credit criteria, including your verifiable income and credit history (if available). The credit limit amount of up to $15,000 under the Scotiabank StartRight® Program is subject to change by Scotiabank from time to time without prior notice. A credit history in Canada is not required in order to be eligible for a credit card under the Scotiabank StartRight® Program.

® Registered trademarks of The Bank of Nova Scotia.

About the author