When it comes to managing your credit and building a good credit score, most people are familiar with the dangers of over-using credit cards. There’s an increased risk of late payments, which can hurt your score, and using a high amount of your overall credit limit also hurts your score over time. Plus, paying interest can harm your overall financial health. But under-using your credit can also hurt your credit score.

Credit utilization—the percentage of your available credit that you use—is a critical factor in determining your credit score. Striking the right balance between under-utilization and over-utilization is key to maintaining a strong financial profile. Here are some practical tips to help you manage your credit utilization responsibly.

Get, and Stay, Canada Ready with our Newsletter

This content was inspired by a recent webinar we hosted in conjunction with our partner, Scotiabank. You can watch the webinar replay here:

- Not too familiar with credit scores? Check out our earlier piece covering myths about credit scores to learn more.

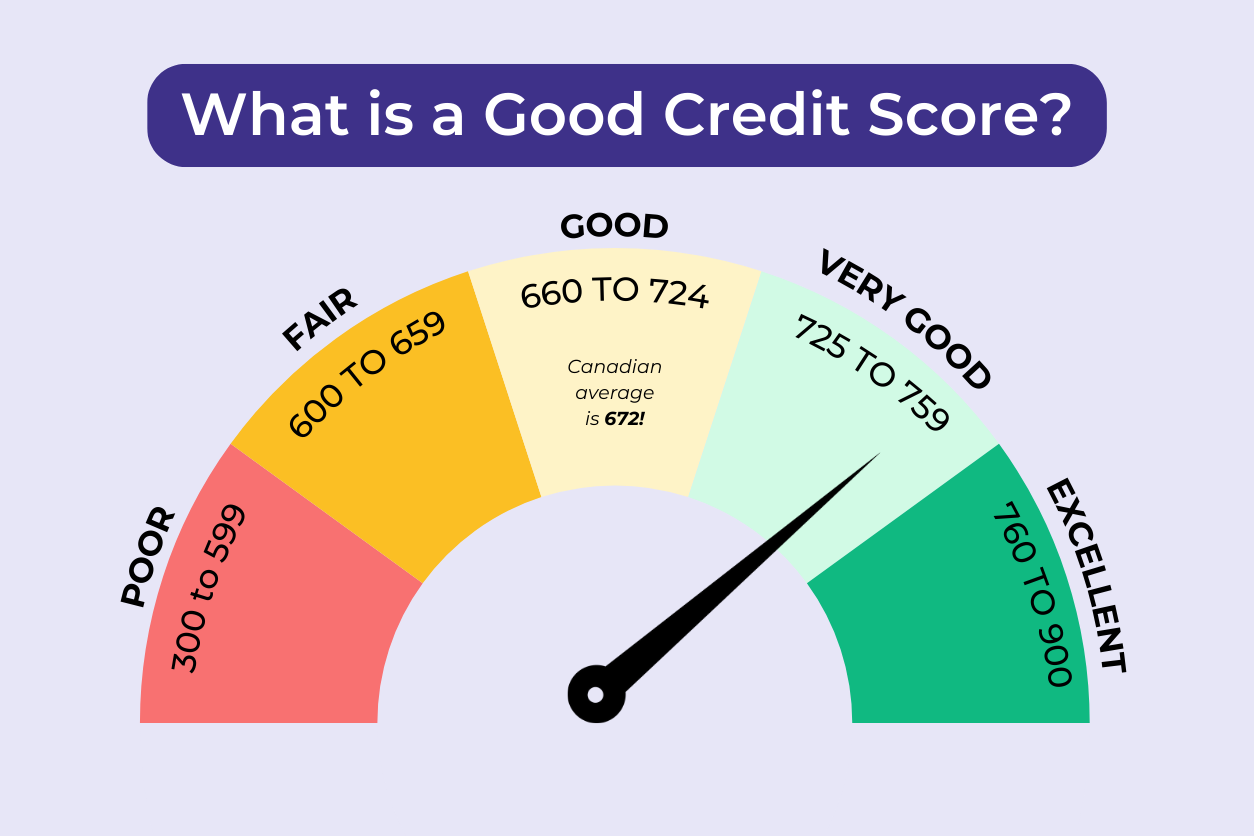

What Is Your Credit Utilization Ratio?

Credit utilization is the percentage of your available credit that you’re using at any given time. Think of it as how much of your “credit pie” you’re eating.

Lenders look at your credit utilization ratio to gauge how responsibly you manage credit. A lower utilization rate tells them you’re not maxing out your credit, which suggests you’re financially reliable. Ideally, you want to keep it under 30% of your total credit limit (Check out our example below to see what this looks like in the real world).

Credit utilization is one of the biggest factors in your credit score. The only factor given more weight in determining your credit score is your payment history. This means keeping a lower credit utilization rate can help you build or maintain a strong score.

Tips For Using Your Credit Card To Build Your Credit Score

Keep Your Credit Card Accounts Active

While maintaining a $0 balance doesn’t harm your credit score, never using your card could lead to account inactivity or closure by the issuer. This reduces your total available credit and increases your utilization ratio. Keep your account active by making occasional purchases, such as groceries or subscription services, and paying them off promptly.

Pay Off Your Balance in Full Each Month

Contrary to a common misconception, you don’t need to carry a balance on your credit card to improve your score. Keeping a balance only results in unnecessary interest payments. Instead, pay off your full balance every month to maintain a positive payment history without accumulating debt.

Diversify Your Credit Accounts

While managing one credit account responsibly is a good start, a diverse credit profile demonstrates that you can handle various types of debt. This includes credit cards, personal loans, phone bills, and lines of credit. A mix of account types adds depth to your credit history and can boost your score over time.

Embrace Higher Credit Limits

Higher credit limits are not harmful if you manage them responsibly. They can even benefit your score by lowering your credit utilization ratio.

For example, if you have a $5,000 credit limit and you use $2,500 then your utilization ratio is 50%. Whereas, if you have a $10,000 credit limit and you use $2,500, then it’s only 25%.

However, it’s very important that you don’t over-use your credit card if you get a higher limit. You don’t want to get into a situation where you can’t pay off your balance in full or where you are missing payments because this will harm your score.

Focus on Avoiding Over-Utilization

Using more than 30% of your available credit has a significantly negative impact on your score. While it’s important to show some activity on your accounts, over-utilization signals financial strain to lenders. Stay well below the 30% threshold to show lenders that you are able to use your credit responsibly.

Looking to Get Smarter with Your Credit Card?

Using your credit card wisely is just one part of building strong financial habits. Whether you’re picking your first card or trying to boost your credit score, there’s more to know.

Check out our article What You Can and Can’t Use a Credit Card For to learn how to choose the right card, avoid common mistakes, and make your credit work for you—not against you.

An Example of Good and Bad Credit Utilization Ratios

Since it’s usually best to aim for a credit utilization of 1-10%, here’s what that looks like in practice:

Meet Emma

Emma has lived in Canada for three years and has established enough trust with her bank to have a $10,000 credit limit. She wants to increase her credit score so she can buy a home in the next five years. She knows that credit utilization ratio will play a role in building her credit score.

Emma has two credit cards:

- Card A: $5,000 limit

- Card B: $5,000 limit.

- Total Credit Limit: $10,000

Good Credit Utilization Ratio (10%)

Emma is diligent about keeping her credit utilization low. This month, she has the following balances:

- Card A Balance: $500

- Card B Balance: $500

- Total Balance: $1,000

To calculate her credit utilization ratio:

Why It’s Good

A 10% utilization rate is excellent and well below the recommended maximum of 30%. This shows Emma is using credit responsibly, which can positively impact her credit score and demonstrate to lenders that she manages her finances well.

Bad Credit Utilization Ratio Example

Imagine Emma has an unexpected car repair and uses more of her credit:

- Card A Balance: $4,000

- Card B Balance: $3,500

- Total Balance: $7,500

Why It’s Bad

A 75% utilization rate is significantly higher than the recommended level if 1-10%. This signals to creditors that Emma might be over-reliant on credit, which could hurt her credit score.

How To Use Your Credit To Build Your Credit Score

Managing credit isn’t about avoiding it altogether or using it excessively. It’s about finding the right balance. Regularly using a small portion of your available credit, keeping your utilization ratio low, and paying off your balance in full each month are the best ways to maintain a healthy credit score.

Remember, credit isn’t just about access to borrowing—it’s also a reflection of your financial habits. By understanding how credit under-utilization works, you can make smarter decisions that strengthen your financial future.

You might also be interested in:

- How to build a good credit score

- What is credit history (hint: it’s another factor that contributes to your credit score)

- Using your rental payments to build your credit score

About the author