Updated on March 9, 2026

This content is sponsored by Scotiabank. The views, opinions, and information expressed in this piece are those of Moving2Canada and do not reflect those of Scotiabank. Scotiabank is not responsible for the content, accuracy, or any representations made herein.

Moving to a new country comes with many challenges, and understanding the financial system may be one of the most crucial challenges you’ll face. But myths and misinformation can make it difficult to know what’s true or not when it comes to your credit score in Canada. Therefore, let’s debunk seven of the most common credit score myths to ensure you start off on the right financial foot.

Key Takeaways

- When you arrive in Canada, you won’t have a credit score.

- Myths and misinformation about credit scores could hurt your chances of improving your credit score.

- Fortunately, there are steps you can take to improve your score – starting with understanding what actually affects your credit score in Canada.

Credit Score Myths In Canada

At a glance, there are 7 myths about credit scores that you may have especially if you are a newcomer to Canada:

- Myth: Checking your credit score hurts or lowers your score.

- Myth: Carrying a balance on your credit card helps to improve your score.

- Myth: No debt = a good credit score.

- Myth: High income guarantees a good credit score.

- Myth: You have one credit score.

- Myth: Paying bills on time = good credit score.

- Myth: Increasing your credit card limit hurts your score.

Do you learn best through video? Check out this video covering tips to build a good credit score in Canada.

Myth: You Shouldn’t Check Your Credit Score, It Will Hurt It

Fact: Soft checks don’t affect your credit score

There are two different types of credit check: hard checks and soft checks.

Hard checks are the only checks that could (temporarily) decrease your score. These checks are usually completed when you file for a loan, mortgage, credit card, phone plan, or other accounts like these.

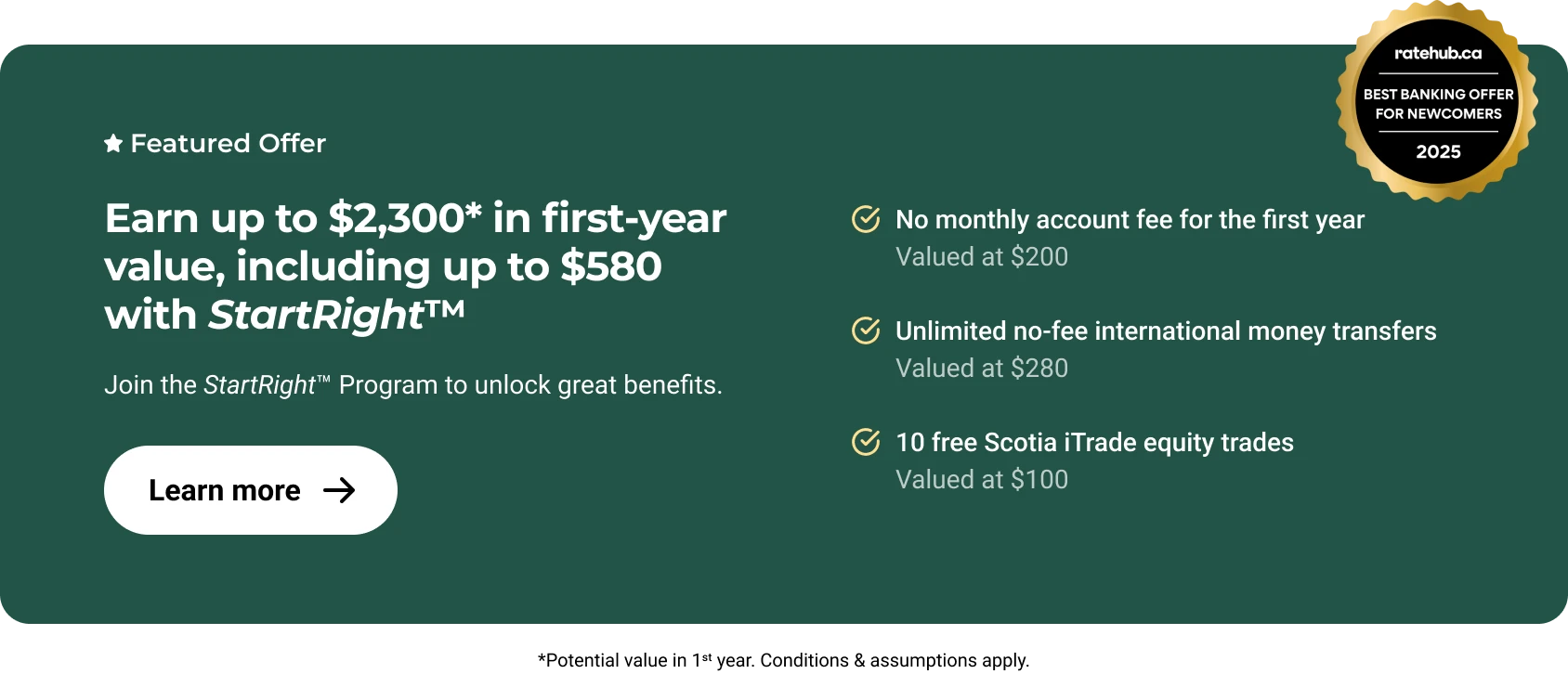

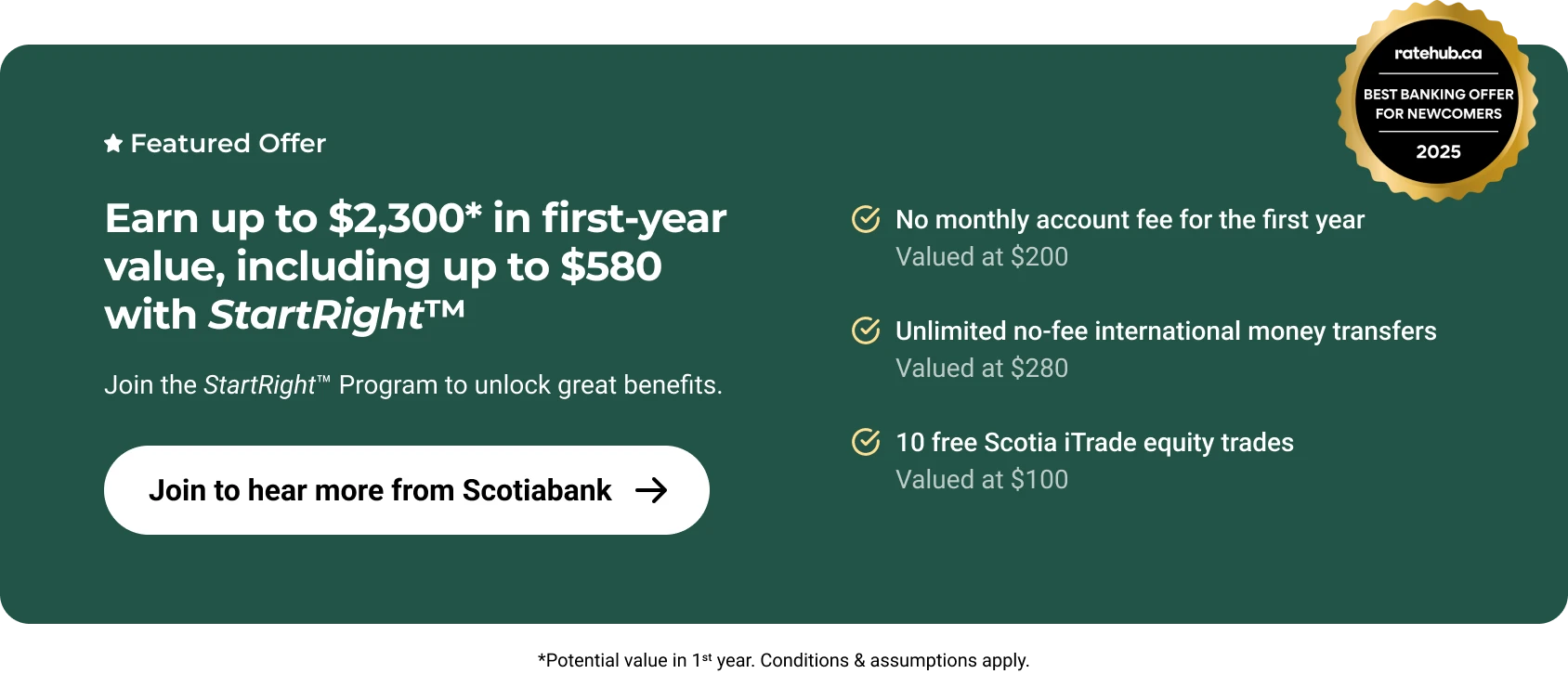

Soft checks, on the other hand, don’t impact your credit. You can safely use certain apps and platforms that keep an eye on your credit score and history without risking your score. For example, if you are a Scotiabank client, you can use the Scotiabank app or online platform to check your score through the TransUnion Credit Score1 tool for no additional cost.

Myth: Carrying A Balance On Your Credit Card Helps Increase Your Score

Fact: It’s important to understand how credit utilization affects your credit score

A common myth is that carrying a balance on your credit card will help improve your credit score. What actually matters is your ‘credit utilization’. Keeping your credit utilization below 30% is generally recommended, as carrying higher levels can negatively impact your credit score.

Credit utilization is the ratio of your current credit card balances to your total credit limits. So, paying off your balance in full helps to keep your credit utilization low and you avoid interest and payment penalties too.

Myth: Increasing Your Credit Limit Hurts Your Score

Fact: Your credit limit doesn’t directly affect your credit score.

Increasing your credit limit only hurts your score if you max out the card and then make only minimum payments – due to the credit utilization impact (see that topic above). As set out above under the credit utilization section , If you have a high credit limit but only use a small amount of it, this can actually help to increase your credit score.

You should always try to avoid maxing out your credit cards. If you notice your credit balance is getting towards your credit limit, it may help if you pay off the balance (or part of that balance) sooner than later.

Myth: No Debt = A Good Credit Score

Fact: You can have a low credit score if you have no debt.

Credit scores are designed to reflect how well you manage credit. So if you have never used credit, there is no history for lenders to evaluate, which means your credit score may be quite low – even if you’re good with money.

This is really common for newcomers, since you usually would not have used credit products in Canada to build a good credit history. It also means that you can have a bad credit score even if you are good with money.

Having some credit activity, such as a credit card or a small loan, and managing it responsibly by not missing payments or using too much of it is important.

Myth: High Income = A Good Credit Score

Fact: Your credit score is not directly related to your income.

Credit scores are based on your credit activity, such as payment history, amounts owed, length of credit history, new credit, and types of credit used. Your income isn’t a factor used to determine your credit score.

That said, a higher income can help you manage your debts and qualify for credit. As a result, a higher income can have an indirect influence on your score.

Myth: You Only Have One Credit Score

Fact: There are two credit bureaus in Canada and you may have a credit score with each.

In Canada, you typically have two credit scores—one from Equifax and one from TransUnion. These credit bureaus may use different information and scoring models, so your scores can (and often do) vary between them. It’s a good idea to check both scores to get a complete picture.

If you are a Scotiabank client, you have access to the TransUnion Credit Tool, you can get your TransUnion credit score at no additional cost whenever you want. You can also read more about getting your Equifax credit score (at no additional cost).

Myth: Paying Bills On Time Guarantees A Good Score

Fact: Your credit score is based on a number of factors, including your payment history.

Your payment history makes up one part of your credit score, but it’s not everything. The length of your credit history, your credit utilization, and the types of credit you carry also impact your score.

Steps You Can Take To Improve Your Credit Score

With all those myths busted, here are some steps you can consider taking to help improve your credit score. Before we dig in, remember that increasing your score is a long-term plan. Be very wary of anyone who tells you that something can help or have a big positive impact on your score in the short-term, it’s not always that easy.

Factors That Affect Your Credit Score

It’s also helpful to understand what factors affect your credit score.

The things that may have a positive impact on your credit score include:

- Paying your bills on time

- A mix of credit

- Your credit history.

These factors could have a negative impact on your credit score:

- Late payments

- Overspending to a point that your credit utilization is high

- Outstanding overdue debt, especially debt that has gone to collections.

With that in mind, take the following steps to improve your credit score over time:

Don’t Miss Payments

While payments aren’t the only factor your credit score considers, it is the factor that credit scores weigh the most heavily. So, it’s important to not miss payments you’ve signed up for wherever possible.

If you do miss a payment, note that they are typically reported late to credit bureaus after 30 days. So you should contact your lender as soon as possible and make your payment as soon as you can to prevent the late payment from appearing on your credit report.

Pay For Your Monthly Expenses On Credit, But Make Sure You Pay It Off Every Month

If you make purchases each month on your credit card and pay the balance when it’s due, this shows responsible credit use and helps to grow your credit score over time. Many credit card companies allow you to set up automatic payments so you’ll never miss a payment.

Tip: When you call your credit card company to set up automatic payments, they will likely ask you if you want to pay the minimum or the full balance. It’s best to pay off the full amount each month if you can.

Access the TransUnion Credit Tool

Your TransUnion Credit Tool can help you monitor your credit score, catch any surprises relating to your credit before they come, and move to a great credit score and better financial health.

Work With Your Bank On Your Financial Health

Scotiabank is here to support you through your financial journey in Canada. We are here to help you:

- Understand banking basics

- Improve your credit score

- Find the right advisor

- Set financial goals and more.

With a Scotiabank personal account, you can register for the TransUnion Credit Tool1 for no additional cost and start building your credit score today

Legal Disclaimer

About the author