If you’re new to Canada, getting a vehicle and then insuring it is likely high on your list of things to do – or perhaps you’ve already bought your vehicle and you’re wondering whether your insurance premiums are likely to keep going up.

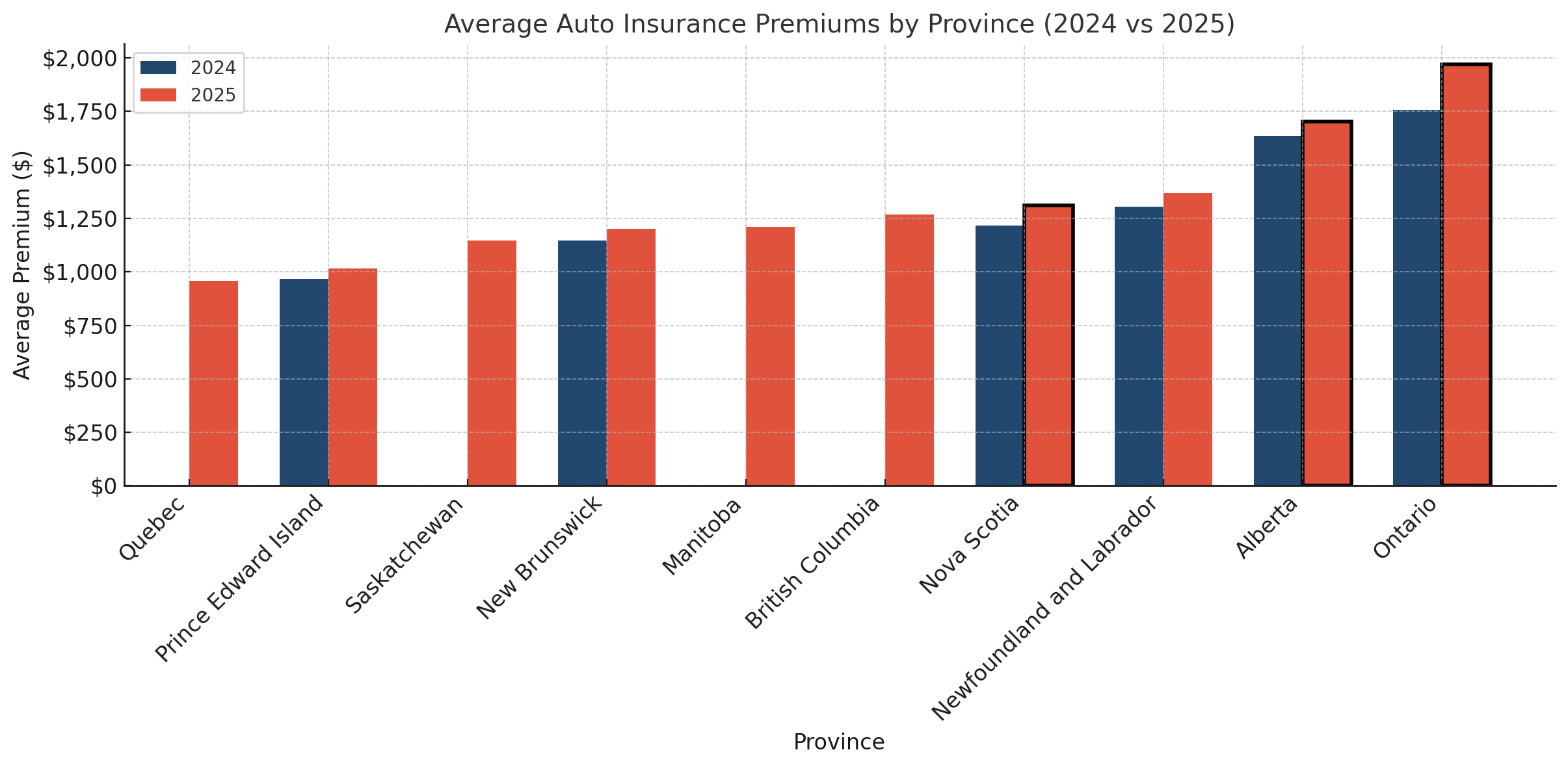

We are currently seeing the steepest increases in auto insurance costs in over a decade. In dollar terms, the average Ontarian saw an increase of $220 from 2024 to 2025, while Albertans saw a $170 annual increase. Newfoundland and Labrador also saw a notable increase of $70 annually.

Premiums dipped during the COVID-19 pandemic when many Canadian residents stopped driving altogether, but that relief was short-lived. As of December 2024, premiums had not only rebounded but were higher than pre-pandemic levels in most provinces. And those costs have continued climbing into 2025. Ontario and Alberta are currently home to the highest auto insurance rates in Canada.

Average insurance rates by province, with data from the AIRB mid-year trends reporting.

Our Partner

Live in Ontario? Try Roam

Roam makes driving accessible and hassle-free for newcomers. Their flexible monthly car subscription is designed to include everything you need to drive stress-free: insurance, routine maintenance, and emergency roadside assistance. Plus, Roam provides a driving certificate at the end of your subscription, making it easier to secure your own car and insurance when the time is right.

Drive Now

What’s driving auto insurance costs up?

Higher repair costs and vehicles are major contributors

From 2019 to 2024, the cost of vehicle parts, maintenance, and repairs increased by 22.3%. At the same time, the price of new and used vehicles skyrocketed—up 61.5% and 82.2% respectively. These jumps are tied to supply chain delays and pandemic-related production slowdowns that continue to ripple through the market.

You can find this Statistics Canada data here.

More expensive claims mean higher premiums

While the number of insurance claims has increased slightly, the real issue is how much each claim now costs. Whether it’s a fender bender or full vehicle replacement, the financial impact is significantly greater than it was just a few years ago.

Vehicle theft and climate change are also driving up costs

Auto thefts in 2023 surpassed $1.5 billion in claims, with Ontario hit the hardest. Though theft rates fell by 17% in early 2024, insurers are still adjusting premiums to account for that risk.

Extreme weather is also a factor. Between 2020 and 2023, every year ranked among the top 10 costliest years on record. In 2024, catastrophic weather damage surpassed $8.6 billion, setting a new high.

Insurers are under pressure to stay profitable

With higher claims costs squeezing profits, insurers are relying more on consumer premiums to balance the books. Many have been operating close to or just above the break-even point, prompting further increases in what drivers are charged.

Difference In Auto Insurance Costs Across Canada

Toronto, Ontario

Auto insurance premiums: Among the highest in Canada

Toronto is ground zero for high insurance costs, largely due to high claim rates, traffic density, and car thefts. For reference, the average cost is around $2050 annually, but newcomers may expect to pay $3,000-$6,000 annually, depending on various factors.

What you can do:

- Avoid owning a car if possible. Toronto has a strong public transit system (TTC), and car-sharing services, as well as long-term rental options, including from our partner Roam.

- If you drive, park in a secure location and consider installing anti-theft devices to lower your premium (the savings options may vary depending on your insurance company).

- Use an insurance broker to compare quotes—Ontario has a very competitive market with many options.

Vancouver, British Columbia

Auto insurance premiums: Moderate to high, but highly regulated

In BC, auto insurance is offered primarily through ICBC, the public insurer. While the system is regulated, premiums are still influenced by vehicle type, driving record, and claim history. Vancouver’s weather-related risks, like heavy rain and flooding, also factor into rates.

What you can do:

- Vancouver leads the country in car-sharing infrastructure. Use it.

- TransLink is a reliable and expanding system, with SkyTrain and buses reaching most areas.

- Vancouver is also a very cycling-friendly city.

Calgary, Alberta

Auto insurance premiums: High and climbing

Alberta has seen sharp increases in recent years. Calgary drivers face elevated premiums due to a higher rate of weather-related claims (hailstorms, icy roads) and ongoing theft concerns. Alberta’s privatized insurance market has also led to greater price volatility.

What you can do:

- Join a car share.

- Choose your vehicle wisely. Pick a model with lower repair costs and less appeal to thieves.

- Maintain a clean driving record—even speeding tickets can raise your premium here.

Montreal, Quebec

Auto insurance premiums: Among the lowest in Canada

Quebec consistently reports the lowest auto insurance rates in the country. A public-private hybrid model, low accident rates, and widespread use of public transit keep costs down.

What you can do:

- Use public transit (STM), biking, or walking. Montreal is built for people, not just cars.

- If you do buy a car, avoid luxury or rare models—repair costs are a key pricing factor in Quebec.

Halifax, Nova Scotia

Auto insurance premiums: Moderate, with room to save

While not as high as Ontario or Alberta, premiums in Halifax are still rising. As the city grows, more traffic and weather-related claims are starting to affect rates.

What you can do:

- Use car-shares or long-term rentals if you only need a car seasonally or for trips outside the city.

- Walk, bike, or bus. Halifax is compact and increasingly transit friendly.

- Work with a local insurance broker who understands regional discounts and programs for safe drivers.

How to Navigate Rising Auto Insurance Costs in Canada

Skip car ownership entirely: It’s a smarter move than you think

If you’re new to Canada and living in a city with a car share program, owning a car might not be necessary. Car-sharing platforms (which vary between cities) offer flexible access to vehicles without the burden of ownership. You pay only when you need to drive—and insurance, gas, and maintenance are usually included.

This approach helps you avoid the big-ticket costs that come with car ownership: insurance premiums, routine maintenance, surprise repairs, and even parking fees. It’s a simpler, more predictable way to get around, especially if you only drive occasionally.

Consider long-term rentals instead of buying

If you need a car for a few months—for work, relocation, or personal reasons—a long-term rental could save you both money and hassle. These rentals often include comprehensive coverage and roadside assistance, making them ideal for short-term needs without the commitment of ownership.

Rentals also offer peace of mind. You won’t have to worry about depreciation, servicing, or whether your car will pass a winter tire inspection. Just return it when you’re done and move on.

Our partner Roam offers long-term vehicle rentals to newcomers in Toronto. They offer competitive rental rates for a modern fleet of vehicles, which you can use for one week, one month, one quarter – or even longer.

Other quick tips to lower your auto insurance costs

Compare quotes from multiple providers

Prices vary widely between insurers. Don’t settle for the first quote—use online tools, like Ratehub or ThinkInsure, to compare options and ask about newcomer-specific discounts.

Choose your vehicle wisely

Cars that are expensive to repair, commonly stolen, or built for performance will usually cost more to insure. Look for a reliable, low-risk model to keep costs down.

Build your Canadian driving history

The longer you drive safely in Canada, the more you save. Insurers reward clean driving records with lower premiums over time.

Our partner Roam provides a driving certificate at the end of your subscription, which can help to build your driving history. This may make it easier to secure your own car and insurance when the time is right.

Consider a defensive driving course

Approved safety courses can show insurers you’re a responsible driver and may help reduce your premium.

Increase your deductible

Raising your deductible can lower your monthly payments—but be sure you’re financially ready to cover it if you need to file a claim.

Final thoughts: You have more control than you think

Auto insurance costs are rising—but you don’t have to face those increases head-on. Whether you decide to ditch car ownership entirely or find smart ways to lower your premium, you’ve got options. Choosing flexibility over ownership isn’t just a financial win—it can make life in Canada simpler, safer, and a lot less stressful.

About the author

Stephanie Ford

She/Her

Finance, Law and Immigration Writer

Stephanie is a content creator who writes on legal and personal finance topics, specializing in immigration and legal topics. She earned a Bachelor of Laws and a Diploma in Financial Planning in Australia. Stephanie is now a permanent resident of Canada and a full-time writer at Moving2Canada.

Read more about Stephanie Ford

Citation

Ford, Stephanie.

"As a Newcomer, Can You Afford Auto Insurance in Canada in 2026?."

Moving2Canada.

Last modified February 11, 2026.

https://moving2canada.com/news-and-features/features/living/finances/can-you-afford-auto-insurance-in-canada-in-2025/.

Copy for Citation

Featured Stories

Work • May 29, 2026

New Spousal Work Permit Exemption for Foreign Health Workers in Quebec with Shorter Work Permits

Read more

Immigration • May 28, 2026

Mark Carney Immigration Policy Tracker

Read more

Express Entry • May 28, 2026

May 28 French Express Entry Draw Invites 4,500 Candidates

Read more

Study • May 27, 2026

IRCC Clarifies How Off-Campus Work Hours Are Counted for International Students in Gig Work

Read more