Updated on April 15, 2026

This content is sponsored by Scotiabank. The views, opinions, and information expressed in this piece are those of Moving2Canada and do not reflect those of Scotiabank. Scotiabank is not responsible for the content, accuracy, or any representations made herein.

You’ve likely heard someone say that you should be saving money. In fact, you might even feel shame that you aren’t saving more.

‘Savings guilt’ is extremely common in Canada, with 63% of Canadian residents avoiding dealing with their finances due to the shame they feel.

We hope to help change that, starting with this framework for managing savings guilt.

This article covers the different types of savings in Canada, as well as how you can approach funding each one to build financial security over time. It’s the first in a series of three that will guide you from saving your first dollar to saving to build security right through to saving for retirement.

Key Takeaways

- The term ‘savings’ is often used to describe any money you set aside from your income to use later, instead of spending it right away.

- There are many different types of savings, and understanding the difference between them can help you better manage your finances.

- Some of the different types of savings include your emergency fund, long-term goals savings, and retirement savings.

- Research shows many Canadian residents feel savings guilt and shame around money. Getting a better grasp on saving money can help you overcome those feelings.

- Finding the right fit when it comes to banking in Canada can help you get settled in and saving faster and more effectively. Learn more about the Scotiabank StartRight® Program.

Before we dig in, we want to quickly talk about financial shame, particularly savings guilt.

In our experience, we see many people (including newcomers) trying to do too much at once. They want to save for a down payment, while also paying off student loans and credit card debt aggressively and starting to fund retirement.

While everyone’s journey and feelings around money are unique (that’s why it’s called personal finance), it is helpful to focus on realistic goals that take your current stage of life and income into account.

That said, a good rule of thumb is the 50/30/20 rule.

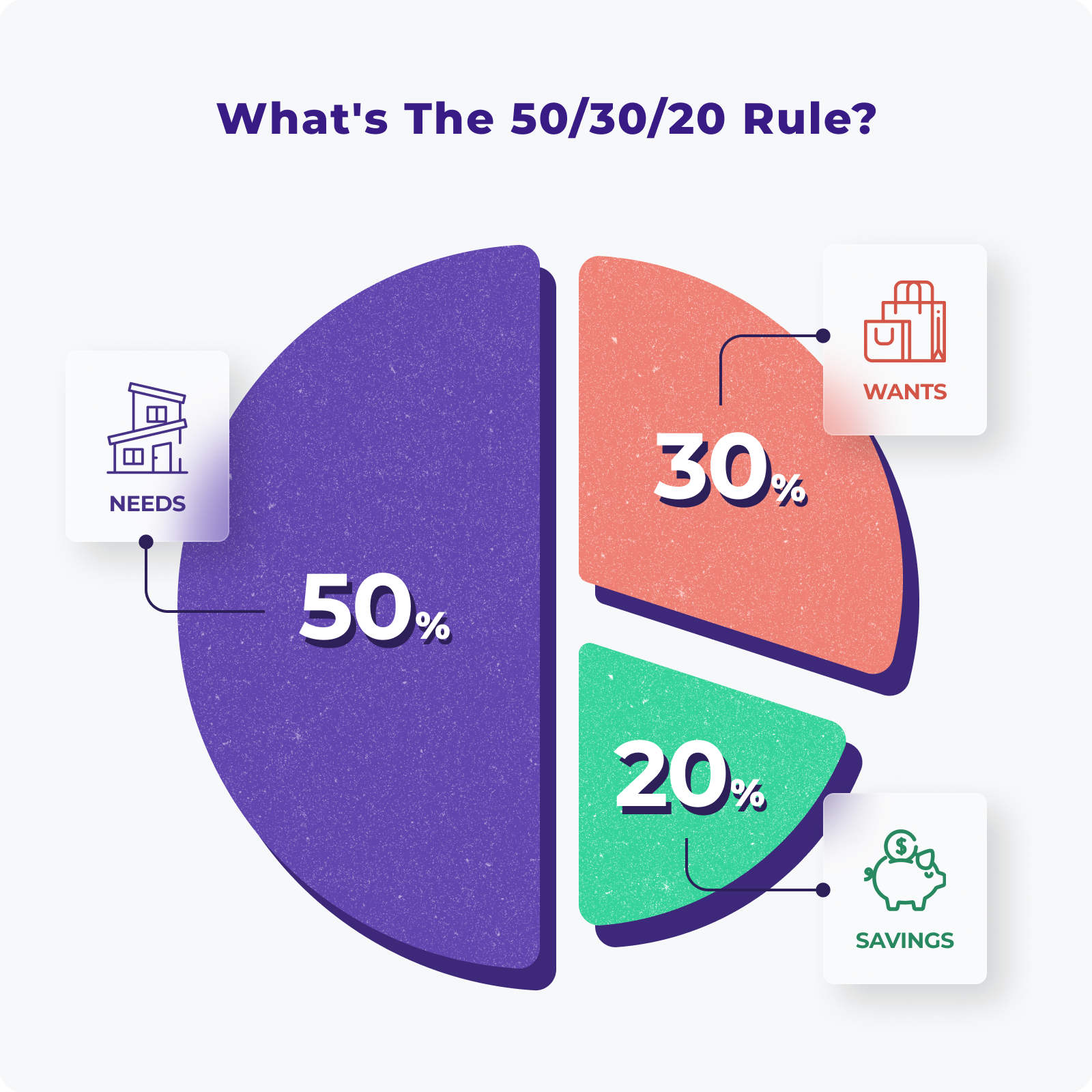

What’s The 50/30/20 Rule?

The 50/30/20 rule is a simple rule of thumb that provides a framework for you to manage your budget. It suggests dividing your after-tax income into three parts: 50% for needs, 30% for wants, and 20% for savings and debt repayment. To be clear, your after-tax income is the amount of money you take home after paying taxes and other deductions.

It’s not perfect for everyone, but it gives a clear starting point to help you stay balanced. Generally, greater balance means that the approach is more sustainable. Plus, this is a helpful framework because it works across all income levels.

Your needs include essentials like rent, groceries, utilities, and transportation. Your wants are things like eating out, Netflix, or vacations. The final 20% goes toward building savings, investing, or paying down debt like student loans or credit cards. It’s about making room for today and tomorrow.

What’s a Good Savings Rate?

If you follow the 50/30/20 rule, your savings rate may be 20%.

But, we believe that the best savings rate is the savings rate you can stick to. If you’re in a stage of life that is really expensive, like if you just bought your first home in Canada or if you have two children in daycare, it’s possible that you won’t be able to save 20%. Whereas if you’re splitting costs of a home with a roommate or sharing a room with your partner, you may be able to save a higher percentage of your paycheck.

We suggest routinely reviewing your finances, including your current savings rate. At these reviews you should ask yourself the following:

- Am I meeting my savings rate goals? If not, what would need to happen for me to consistently meet that savings rate goal? What changes could I make today?

- Is it possible to save more during this stage of my life, to make things easier for my future self? If so, based on the savings I have today, would that be a good idea?

The Savings Hierarchy: From Survival to Security to Success

Savings is a really broad term, which people generally use to mean any money that is set aside for the future instead of spent in the short term.

We have developed this savings hierarchy to help you understand the different types of savings accounts, and where they may fit into your overall budget and plans for your money. You can use it to pinpoint exactly where the money you save goes each month to achieve your goals more quickly.

There are two approaches we often use. If you think that either of these approaches align with your goals and suit your personality, you’re welcome to use them in your personal finance journey:

- Throw everything at one goal. This is really targeted and can help you achieve that one goal much faster. This is good for anyone who gets a lot of satisfaction from checking a to-do item off a list.

- Allocate your savings efforts towards 2-3 goals and work towards them simultaneously. We don’t usually recommend working towards more than 3 goals at one time, because progress at that point could be slow and likely demotivating.

Short-Term Savings Goals

We suggest tackling these two shorter-term savings goals before moving onto your mid- and long-term savings goals because having funds saved for now means you’re less likely to ‘raid’ your long-terms savings accounts.

Cover Your Living Expenses Using Your Chequing Account

Building up your chequing account balance is a good place to start if you’re currently living paycheck to paycheck. A good goal is to have 1-2 months of living expenses sitting in your chequing account so that you can automate your bill payments and avoid overdraft fees.

One quick tip for this stage is to use debit cards instead of credit cards for a few months to get used to managing your living expenses as they arise.

Type of Account for this goal: Chequing Account

What to look for: Some banks in Canada offer banking packages tailored to newcomers, including chequing accounts. One option, Scotiabank StartRight® Program‡ is built to help newcomers feel more at home, faster. It comes with no-fee international money transfers1, cashback perks, and no-monthly fee chequing for the first 12 months2. Learn more.

Build an Emergency Fund

With your daily living expenses covered, it’s often a good idea to build an emergency fund that contains 3-6 months of living expenses – or even up to 12 months if you work in a volatile industry or you have children.

This is your financial airbag in case of the unexpected – like a job loss, sudden travel out-of-country to see a sick loved one, or to cover an unexpected car repair following an accident.

Type of Account for this goal: High interest savings account

What to look for: A savings account that lets you make the most of your money! Effortlessly build your balance with our smart savings tools; Pay Yourself First and Savings Finder. Scotiabank’s Money Master Account can help you reach your savings goals by automatically moving money between your eligible Scotia chequing account and your Money Master Savings Account based on your income, spending, and the targets you set.3,4

Saving For Your Future Self: Mid- To Long-Term Savings Goals

With your emergency fund built and your chequing account in check, here’s where your savings can go next:

Big-Ticket Goals – Car or House Down Payment

Saving for those big-ticket items, like a down payment for a home or a new car, can feel really good — as long as you’re realistic.

Let’s say you want to save $25,000 for one of those bigger ticket items:

Allocating $1041.67 per month over the course of two years is required. Alternatively, saving $416.67 per month over five years is needed (assuming no interest is earned).

Best Type of Savings Account:

For the 2–5-year savings horizon, you may be best off in a high-interest savings account.

If your goal extends beyond five years, you can start to consider investment options. We’ll dig into these in more detail below.

Also, at this stage, you may want to think about using your tax-advantages savings vehicles, like your Tax-Free Savings Account, to save for a car purchase, education, or any other big-ticket items. If you’re saving for a down payment for a home, consider a First Home Savings Account or a Registered Retirement Savings Plan. (Just remember, you still need to put the money into a high-interest savings account or towards an investment within your TFSA, RRSP or FHSA. It’s not automatically invested!)

Retirement Savings – Paying Your Future Self

Starting early to save for your retirement is honestly like having a superpower. The amount of compound growth your money can earn if you start saving for retirement in your twenties or thirties is remarkable. If you’ve paid down high interest consumer debt and have an emergency fund, putting 10% towards your retirement savings early in life can offer a big boost later.

Which account is the best account for your retirement savings?

Your RRSP and TFSA are great vehicles for retirement savings based on individual needs and financial circumstances.

FAQs About Saving Money in Canada – Shame-Free

How does this framework help with savings guilt?

The reality is that we all only have a limited amount of money to save. Saving all your income isn’t practical; for most, even saving over 20% is unrealistic. So the 50/30/20 rule can help to take the pressure off and reduce any feelings of guilt or shame, if you’re experiencing those (like reporting shows many Canadians are).

Is it better to pay off debt or save money?

There are two answers here: one is mathematical and the other has to do with managing your feelings — each is valid.

Mathematically, it usually makes sense to pay your high interest consumer debt first. This is debt like credit card debt, some student loans, personal loans, lines of credit, and it can include car loans.

However, if paying down debt at the cost of saving any money doesn’t ‘feel’ right – that can be valid. And for you, it may be worth reducing your debt repayments to build a little more financial security – like a higher balance in your chequing account or a partial emergency fund.

You can find more tips to get out of debt in this Scotiabank Advice+ article, or speak with a Scotiabank Advisor for tailored guidance and a solution that is best for you.

How do I save 20% of my income?

This starts with a budget. Budgeting lets you look at the big picture, which can then guide your priorities and identify areas you might need to change some things to meet your goals.

There are various methods to start your budget. Take your time to find the approach that feels right for you, ensuring you begin your journey on the right foot.

How to Start Saving Money?

If you’re not sure where to start, Scotiabank offers banking products with newcomers to Canada in mind. From the StartRight™ Program with newcomer-focused benefits like a chequing account with no monthly fees for the first year, to the Money Master Savings Account, Scotiabank is great for newcomers.

Start saving with the Scotiabank StartRight® Program

And if you need individual guidance to build a brighter financial future in Canada, a Scotiabank Advisor can help. Book your appointment to get started.

This article is provided for information purposes only. It is not to be relied upon as financial, tax or investment advice or guarantees about the future, nor should it be considered a recommendation to buy or sell. Information contained in this article, including information relating to interest rates, market conditions, tax rules, and other investment factors are subject to change without notice and The Bank of Nova Scotia is not responsible to update this information. References to any third party product or service, opinion or statement, or the use of any trade, firm or corporation name does not constitute endorsement, recommendation, or approval by The Bank of Nova Scotia of any of the products, services or opinions of the third party. All third party sources are believed to be accurate and reliable as of the date of publication and The Bank of Nova Scotia does not guarantee its accuracy or reliability. Readers should consult their own professional advisor for specific financial, investment and/or tax advice tailored to their needs to ensure that individual circumstances are considered properly and action is taken based on the latest available information.

Commissions, trailing commissions, management fees and expenses may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed or insured by the Canada Deposit Insurance Corporation or any other government deposit insurer, their values change frequently and past performance may not be repeated.

Legal

About the author