Updated on July 7, 2026

Studying in Canada is incredibly rewarding, and it promises a lifetime of opportunities, friends, and adventure. But, navigating your finances as a student is challenging no matter where you live – and the costs of studying abroad in Canada are often higher than the costs of studying in your home country. Therefore, if you want to fully reap the benefits of studying in Canada, you will need to learn the art and science of budgeting as an international student in Canada.

Being a student comes with many new challenges: living on your own (often for the first time), managing classes, fitting in with new people, and managing money. For international students, these challenges are amplified: you’re not just away from home, but in a whole new country and culture. Handling your money on top of everything else may feel like a lot, but it comes down to three very simple steps:

- Knowing what money is coming in;

- Deciding what money (and how much) will go out;

- Balancing your priorities from there.

In this post, we will outline some tips and tricks we’ve learned to help you manage your finances and keep to a budget as an international student.

Key Takeaways About Budgeting As An International Student

- You must accurately document what money you’ll have access to throughout your study period.

- You will need to plan and prioritize how you will spend that money so you don’t go into unplanned debt during your study period.

- Saving on your biggest expenses (tuition, food, and accommodation) can really help to reduce your financial outlays while studying.

International Student Budgeting 101: Understanding and Managing The Money Coming Into Your Accounts

International students in Canada need to show access to adequate financial resources to get their study permit. This means that it’s likely you have a sum saved somewhere that will (hopefully) get you through your study period in Canada.

Some international students get this money from scholarships or bursaries, others work and save for a few years, while others receive money from their parents or extended family members.

Wherever the money comes from, international students do need to know and understand what money is coming in through the year, and what’s going out.

Here are some tried and true tricks for understanding and managing the money coming into your accounts as an international student:

Document The Money You Have Available

Step 1: Document all the money you have available at the start of your year as an international student. This includes:

- Student loans.

- Money in your savings account.

- Funds invested in a Guaranteed Investment Certificate (GIC).

- Gifts from your family.

Earning Money As An International Student

You should also consider whether you will work as an international student in Canada. International students who are enrolled full-time at a Designated Learning Institution can work off campus without a work permit for up to 20 hours per week during the school term and full-time on study breaks. You can learn more about working while studying, including any special measures that may allow you to work additional hours, on our dedicated page.

If you’re eligible and you want to work, you should work out approximately how much you’ll earn per hour and how many hours you will be able to work per week while also managing your study obligations.

Many international students will earn minimum wage for working while studying, which varies from province to province.

| Province/Territory | Minimum Wage (CAD) |

|---|---|

| Alberta | $15.00 |

| British Columbia | $17.85 |

| Manitoba | $16.00 |

| New Brunswick | $15.65 |

| Newfoundland and Labrador | $16.00 |

| Northwest Territories | $16.95 |

| Nova Scotia | $16.50 |

| Nunavut | $19.75 |

| Ontario | $17.60 |

| Prince Edward Island | $16.50 |

| Quebec | $16.10 |

| Saskatchewan | $15.35 |

| Yukon | $17.94 |

| Federal (for federally regulated industries) | $17.75 |

Often, this totals around $20,000 – $30,000 per year, including full-time work during study breaks.

Look For Financial Aid

A helpful first step for ‘finding’ additional money while you study is to start with the financial aid office at your school. These advisors are trained to help students afford their studies. They’re in the best place to suggest scholarships, bursaries, loans, and other financial aid. You should book an appointment with an advisor as soon as possible.

Are you ready for Canada?

Budgeting For Your Expenses As An International Student

Moving to a new country can be expensive. There are rental deposits to pay, transit passes and books to buy, and it’s inevitable that you’ll make some mistakes along the way as you learn to navigate your new surroundings.

We’ve highlighted some of the more impactful measures you can take to stick to your budget as an international student:

Look For Opportunities To Save on Your Biggest Expenses

Some students are notoriously good at finding creative ways to save money while studying. These are some of the best ways to save on some of your biggest expenses: meals and housing.

Seek a Dormitory Supervisor Position

Dormitory supervisor roles are some of the most coveted positions on campus, so it’s best to start looking for these as soon as possible. Often, these positions include free rent and/or meal plans, resulting in huge cost savings.

Consider Housesitting or Homestays

There are other opportunities for getting cheap or very free rent, including housesitting and homestays. Participating in housesitting or homestays will require a lot more flexibility than finding long-term student accommodation, but that’s the tradeoff you’ll need to make to get free or very cheap rent.

Get Creative About Meals

Food costs have increased substantially in Canada in recent years, so shopping around or getting creative when it comes to your meals can save quite a bit of money. Consider attending catered conferences or guest lectures, wine and cheese evenings, or student society events.

You might also want to arrange meal swaps with your friends, where you cook one evening per week in exchange for them providing food on other nights. Often, it can be cheaper to buy ingredients in bulk so buying ingredients for one meal and sharing is usually more cost-effective than planning five different meals each week.

Managing Your Lifestyle Expenses

As a student, there will always be opportunities for new adventures in Canada: extracurricular clubs to join, late-night library study sessions, and parties to attend. The key to making the most of your college or university experience is finding balance.

As far as your finances are concerned, you can only find balance if you understand both the money you’ve got coming in and the money you’ve got going out. Here are our top tips for managing expenses:

Understand the difference between needs and wants

Do you need to buy a foamy latte every morning? If you buy a $4.00 coffee every weekday for a year it adds up to more than $1,000! (Side note: don’t underestimate the power of investing this sort of sum, as compounding interest really adds up over time. We’ve created a whole separate guide on investing as a newcomer in Canada here.)

If you can understand the difference between the things you really need and the things you want, you’ll save yourself a ton of money over the year — even just through cutting back on smaller purchases, like meals, clothes, and 2 a.m. tequila shots (trust us: you will always regret 2 a.m. tequila shots, and not just financially).

That being said, try to allow some space in your budget for “wants.” Get that latte on Fridays, but bring your own coffee other mornings. Treat yourself to a dinner out after a big exam, but don’t eat out multiple times each week. Find your balance!

If you use credit cards, spend wisely and always make your monthly payments

Credit cards are common in Canada. They allow you to make purchases on credit, “borrowing” money from the credit card issuer. You must pay back the money over time with a mandatory minimum payment each month. Credit cards can be convenient, allowing you to automate monthly payments, make online purchases, and, most importantly.

But — be careful! Don’t spend more on your credit card than you’ll be able to pay back, and always be sure to make your minimum payment each month. Failing to miss a payment — yes, even just one! — can negatively impact your credit score.

Read more: How to start building a good credit score

Shop second-hand to cut your expenses

Look for opportunities to buy used items, whenever possible. Move into a new apartment and need to get furniture? Check with friends, classmates, and online buy-and-sell groups to see if anyone is selling furniture.

This trick also works with textbooks. New books can be hugely expensive. See if you can buy used versions of your books from students who took the class before you. Resell the books at the end of the course and you’ll be saving a ton of money on books alone.

Save for Canadian expenses

You’re going to school in Canada — and Canada has its own unique expenses to consider.

One big Canadian consideration: winter. Winter is a big deal. You’re going to want good quality winter boots, jacket, hat, scarf, and gloves. This is one area where you don’t want to sacrifice quality or you’ll be left out in the cold (literally). If you pay to heat your home, you should also plan to pay a lot more during the winter months.

Balancing Your Money In and Money Out

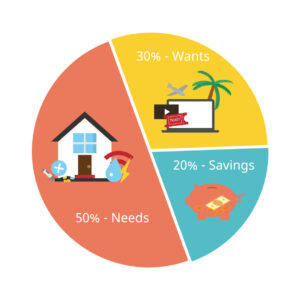

A common method used to balance your budget (while still having a life) is the 50/30/20 rule. This rule suggests that you should spend about 50% of your money in on your needs, 30% on your wants, and 20% on savings (including investments).

To implement this, the absolute first step in balancing your budget as an international student is to allocate your ‘lump sums’ for the year. Given that you will likely start the year with large sums of money, either in your savings account or a GIC, or via student loans the like, it is critical that you allocate these so they will last the entire year.

Consider saving that cash in a separate savings account that isn’t linked to a card. Then pay yourself an allowance out of this account over the course of the year, like what you would get if it were a regular paycheck. Try to live within your means so you don’t need to draw additional funds from this lump sum amount.

To work out how much to pay yourself, use the figures you calculated above:

- Add up all the money you have available initially and how much you will earn throughout the year, then

- Work out your likely expenses per month, plus any lump sum expenses you’ll need to pay (like tuition).

- Add a portion for spending on your ‘wants’ (ideally, 30% of your monthly income).

- And tuck some away for savings!

What If Your Study-Related Expenses Are Higher Than Your Income?

Ideally, the amount of money you have available will be more than your likely expenses.

If not, make some adjustments to decrease the amount you’re spending – or, alternatively, increase the amount you are earning. (Make sure the changes are realistic! It’s not realistic, for example, to live on $50 per month for groceries, no matter how much you like ramen noodles.)

Finally, set up a recurring payment for the amount you can spend each month.

Then, regularly review your spending habits to be sure your plan aligns with your budget. If not, it’s time to make some more adjustments!

Struggling to save—and kinda feeling bad about it?

You’re definitely not the only one. The good news? Saving doesn’t have to be stressful (or boring). Read further resources to master Budgeting and Savings in Canada.

- Start with the basics by mastering the different types of savings in Canada and take your first step toward saving with confidence—no guilt needed.

- Learn about the multiple methods newcomers use for budgeting during their first few months.

Are you ready to study in Canada?

Related Content

Immigrants Start Behind Financially, But Many Catch Up Within a Decade, StatCan Finds

Read more

New Worker and Student Arrival Numbers from May 2026 Show Decline

Read more

New Canada Child Benefit Payment Arrives July 20. How Much Will Families Receive?

Read more

New Canada Groceries and Essentials Benefit (CGEB) Payments Start July 3. Who Qualifies?

Read more

About the author