Updated on July 6, 2026

This content is sponsored by Scotiabank. The views, opinions, and information expressed in this piece are those of Moving2Canada and do not reflect those of Scotiabank. Scotiabank is not responsible for the content, accuracy, or any representations made herein.

The right budget can help you navigate your finances in Canada with confidence. But the challenge is that there is no single budgeting approach that is right for everyone. People budget in different ways depending on their circumstances, priorities, and their personal preferences for tracking expenses.

That’s why we’ve created this article outlining some of the different types of budgeting. We share information about how each method works and the benefits and drawbacks of each. But remember, this information is provided for general educational purposes only and is not intended as financial, legal, or tax advice.

Key Takeaways

- A budget isn’t a spreadsheet or a particular tool. It’s a plan for your money for a set period of time.

- Some of the more common types of budgets include zero-dollar budgets, percentage-based budgets, and envelope budgets. We cover these in detail in this article.

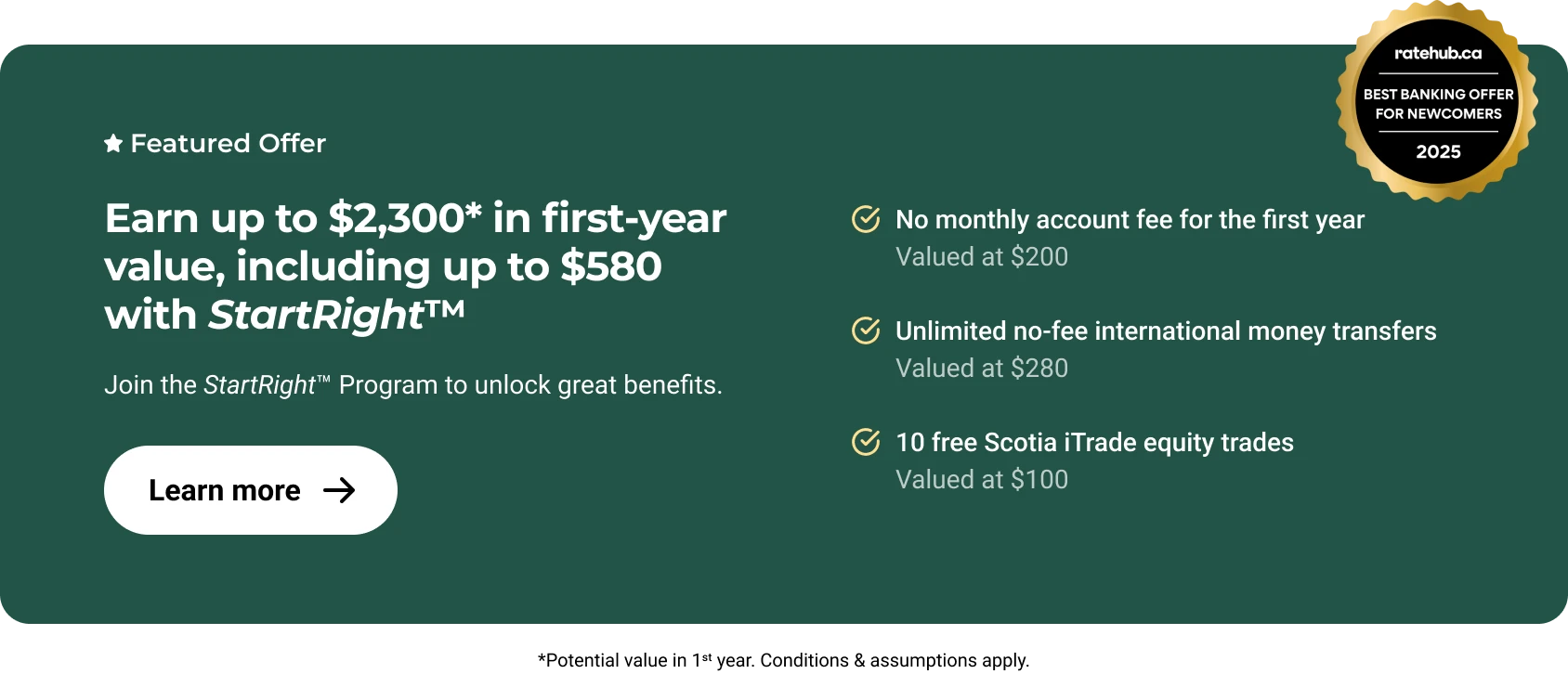

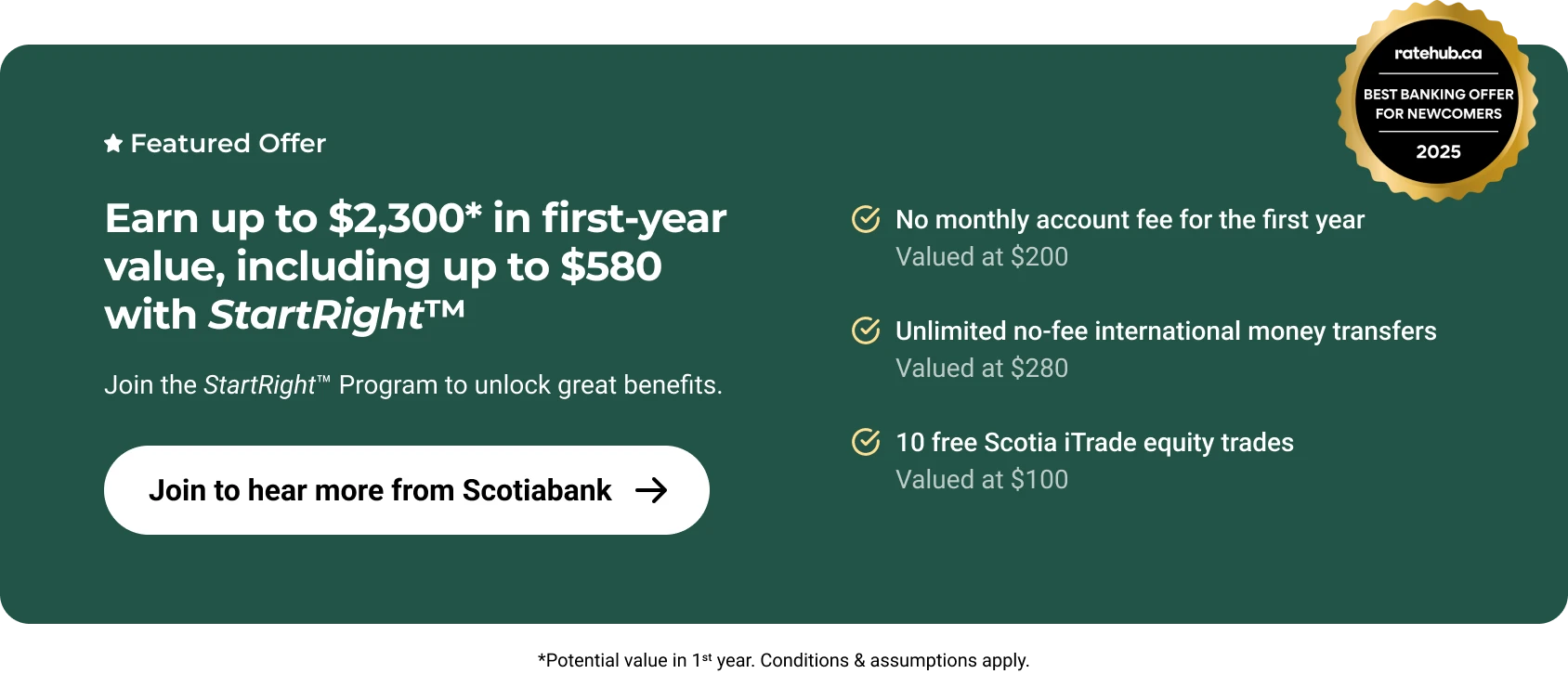

- Together with our bank sponsor, Scotiabank, we have created a Budget Planner tool for newcomers to Canada.

- Scotiabank offers its customers a range of tools that can help with budgeting, including Scotia Smart Money and the Scotiabank Money Finder Calculator. Getting started with Scotiabank is easy.

What is a Budget?

A budget is a plan for your money over a specific period – usually a month. The plan is usually based on what you expect to earn and how you expect to spend or save that money.

We received some really helpful advice from an article published by Scotiabank about budgeting approaches before we wrote this article. They note:

“There are lots of ways to create a budget – the best one for you is the one you can stick with.” — Scotiabank Advice+ Team.

Some budgeting approaches have you tracking every dollar, others focus on spending within broader categories without granular tracking. Then, there are budgets aimed at helping people aggressively pay down debt for the short-term, while other approaches advocate for sustainable spending to promote long-term financial planning. In other words, there isn’t one type of budget. There are different strategies you can use to create a budget, and a diverse range of spreadsheets and apps available too – like the Scotiabank Money Finder Calculator.

Some people find this helpful because it means there’s flexibility and different options. But, some may find it overwhelming to get started budgeting if they don’t know where to start.

The Different Types of Budgeting

This is where budgeting can get overwhelming – choosing the type of budget that you like (or at least want to try out). Each type of budget has critics and fans, alongside a list of perks and drawbacks.

Zero-based budgets

Zero-based budgets mean that you assign every single dollar of your income until your leftover is $0. To be clear, this doesn’t mean that you spend all of your money. It only means that the number of dollars that you don’t assign to a ‘job’ each month is $0.

‘Jobs’ that you may assign your money to using a zero-based budget include things like:

- Savings, including short-term savings for things like emergency funds or a vacation,

or long-term savings for retirement or larger purchases. - Paying down debt, including making payments above your monthly minimums.

Benefits and drawbacks of zero-based budgets

Zero-based budgets can be helpful for those who want a clear plan or to tightly control their spending. It can also be particularly useful for those who want to aggressively tackle a goal, like paying down debt or saving for a vacation or car repair.

However, it can be time intensive to use a zero-based budgeting approach. So, some people find that it feels like they’re spending more time making and adjusting the plan than they’d like. It can also be a little tricky to manage if you have irregular income.

Percentage-based budgets

A percentage budget suggests splitting your after-tax income into broad buckets andsticking within those margins. The 50/30/20 framework is common, but you can adjust the percentages to suit your needs.

The 50/30/20 approach suggests putting 50% of your income towards your needs, 30% towards your wants, and 20% towards savings and debt repayment. You can learn more about this approach from the account of one of our team members, who shared their 50/30/20 budget, and from our dedicated piece covering building savings in Canada.

Benefits and drawbacks of percentage-based budgets

Percentage-based budgets tend to be quite flexible and quick to maintain. When coupled with financial tools like an automatic savings plan, that automates your monthly savings amounts and other recurring transfers, a percentage-based budget can be followed with relatively low amounts of effort. That can make it appealing to people who dislike line-by-line tracking.

Unfortunately, percentage-based budgets don’t work for everyone. This style of budgeting can be frustrating to follow if your ‘needs’ exceed the 50-60% each month mark. It may also not be precise enough for those looking to address overspending in certain areas.

Finally, percentage-based budgets may also under-address goals like aggressive debt payoff or saving for large purchases.

Envelope budgets

An envelope system means allocating money into ‘envelopes’ across set categories, often for needs like groceries, fuel, restaurants and entertainment, rent/housing, and expenses for children. This can be literal cash stored in envelopes or a digital equivalent.

In some ways, it’s similar to a zero-based budget, in that you’re allocating spending amounts in advance. But, you don’t necessarily need to have every dollar accounted for before the month starts using an envelope budget, so it is slightly different.

Benefits and drawbacks of envelope budgeting

This system can be helpful for some people who want to stop overspending on certain categories. Plus, it can also make the trade-offs of overspending more obvious. For example, if your restaurant and entertainment envelope is empty but you want take out, you will need to choose which ‘envelope’ you take money from – which can highlight the impact of your spending on your overall financial goals.

In terms of drawbacks, this system can feel inconvenient – especially if some spending is automated, such as automated credit card payments. The envelope system also requires those using it to regularly categorize spending and check balances of specific accounts or envelopes. Finally, it can also be challenging to account for irregular expenses, such as car repairs or annual pet insurance, using an envelope budget.

Reverse budgeting

Reverse budgeting means starting with the monthly goal and then spending whatever is left without heavy category rules. In practice, this might look like first paying $1,500 towards debt or saving it for an emergency fund. Then, with your goal hit, spending the rest of your income that month flexibly.

Benefits and drawbacks of envelope budgeting

Reverse budgeting can offer a good balance between structured saving and freedom, since it doesn’t take much time to set up or manage. However, some people who try this method find that “whatever remains” disappears too quickly.

If this happens, they may need to pull some money from savings or pay for things using debt. This can slow down progress, which can be frustrating or disheartening. Plus, this approach still requires accurate knowledge of fixed and irregular expenses. So it may not be as ‘low maintenance’ as it may seem.

Which budgeting method is best?

As with many things in personal finance, the budgeting method that is best for you is a personal choice. No approach is better or worse than the others. In fact, each approach likely has people who are enthusiastic fans and strong critics.

So, as the Advice+ Team at Scotiabank said, the best budgeting method is the one that you’ll use and stick to.

5 quick tips for budgeting successfully

In terms of creating and sticking to a budget, here are some quick tips that may help you:

- It’s important to be realistic and honest when tracking your income and expenses each month. Budgets are often less useful when the numbers aren’t accurate.

- Having clear and realistic money goals or a vision for your future can help you make decisions when it comes to short-term spending.

- Just because one type of budgeting didn’t work for you doesn’t mean that you’re a bad budgeter. Try different approaches to see if you like them more!

- Even lower-maintenance approaches to budgeting aren’t static. It may be helpful to check your spending against your plan from time-to-time, and make adjustments

where you need to. - Lastly, seek help with budgeting if you need to.

Our bank sponsor, Scotiabank, offers its customers a range of tools that can help with budgeting, including:

Getting started with Scotiabank is easy. You can open an account online to access these tools and support your budgeting goals.

Plus, Scotiabank customers have access to meet with an advisor. Scotiabank also offers a no-obligations meeting with an advisor to newcomers of Canada.

This article is provided for information purposes only. It is not to be relied upon as financial, tax or investment advice or guarantees about the future, nor should it be considered a recommendation to buy or sell. Information contained in this article, including information relating to interest rates, market conditions, tax rules, and other investment factors are subject to change without notice and The Bank of Nova Scotia is not responsible to update this information. All third-party sources are believed to be accurate and reliable as of the date of publication and The Bank of Nova Scotia does not guarantee its accuracy or reliability. Readers should consult their own professional advisor for specific financial, investment and/or tax advice tailored to their needs to ensure that individual circumstances are considered properly, and action is taken based on the latest available information.

About the author