Updated on May 20, 2026

This content is sponsored by Scotiabank. The views, opinions, and information expressed in this piece are those of Moving2Canada and do not reflect those of Scotiabank. Scotiabank is not responsible for the content, accuracy, or any representations made herein.

Many Americans have the impression that taxes in Canada are extremely high. But, how do the two countries actually compare?

We decided to find out by comparing mandatory withholdings in both countries. And the results might surprise you.

Before we dig in, we do want to note that tax rates vary widely across Canada and the US, so the results may vary, depending on where you live. This comparison is designed to be very broad and to compare Canadian provinces with similarities to US states.

Interested in moving to Canada from the US? Check out our webinar:

Similarities and Differences Between American and Canadian Income Taxes

There are quite a few striking similarities between the US and Canadian income tax systems, which means that those who move from the US to Canada will be somewhat familiar with what shows up on their pay slip.

Some of the key similarities are:

- Most US states and all Canadian provinces charge additional income taxes beyond the federal tax rates. These state/provincial taxes vary across the countries, with some states/provinces offering lower taxes while others charge higher rates.

- Canadian and American workers both pay for ‘Social Security’ (called the Canada Pension Plan across most of Canada and the Quebec Pension Plan in Quebec) alongside income taxes.

- Both Canada and the US have tax-advantaged retirement accounts that can be used to reduce overall tax liabilities.

Some of the key differences are:

- US residents pay a Medicaid deduction at the federal level. Healthcare is largely funded publicly in Canada so Canadians do not pay into healthcare federally (at least not directly).

- Canada does not have any ‘state-tax-free’ jurisdictions. All Canadian resident earners pay income taxes at the federal and provincial/territorial level.

- Canada does not allow ‘joint’ tax filing. Everyone files individually (and Quebec residents file twice), though you need to state your marital status when you file and declare your partner, if you have one.

- Canadian workers also pay for “Employment Insurance” (EI) through their pay cheques. EI provides temporary financial assistance to eligible individuals who lose their jobs or face specific life events, such as illness or parenthood. This is how things like unemployment benefits and maternity/paternity leave are funded in Canada.

Who Earns More on Average: Americans or Canadians?

Americans are the winner here. While figures vary for the average employment income for US residents, it hovers between $66,000–$68,000 USD. Canada’s average wage in 2024, in USD, was around $51,100 (or $68,832 CAD).

Note that we’ve used a historic currency conversion rate of 1 USD to 1.35 CAD for the purposes of this article. The USD is historically strong against the Canadian dollar at the time of publishing, so we’ve relied on an average for accuracy.

Do Americans or Canadians Pay More Income Tax?

Everyone’s favorite answer: it depends. It depends on where you live and how much you earn.

Federal Income Taxes in Canada vs in the USA

Let’s look at the federal tax rates in Canada (including a USD conversion) to the US federal rates:

| Canada - 2025 Federal Tax Rates | ||

|---|---|---|

| Tax Rate | Taxable Income (CAD) | Approx. USD |

| 15% | Up to $57,375 | Up to $42,500 |

| 20.5% | $57,375 to $114,750 | $42,500 to $85,000 |

| 26% | $114,750 to $177,882 | $85,000 to $131,000 |

| 29% | $177,882 to $253,414 | $131,000 to $188,000 |

| 33% | Over $253,414 | Over $188,000 |

| US - 2025 Federal Tax Rates | ||

| Tax Rate | Taxable Income (USD) | |

| 10% | Up to $11,925 | |

| 12% | $11,925 to $48,475 | |

| 22% | $48,475 to $103,350 | |

| 24% | $103,350 to $197,300 | |

| 32% | $197,300 to $250,525 | |

| 35% | Over $250,525 |

So, those with an income of $48,475-$85,000 USD would pay less federal tax in Canada than in the USA. Outside of those brackets, those in the US pay less in federal taxes. It’s worth noting that the average US wage falls into the range that would be lower in Canada than the US.

Income Taxes at the State/Provincial Level

There’s no doubt about it, very high earners pay more taxes in certain Canadian provinces than in any US state. British Columbia’s highest tax rate is 20.50% for earnings above $259,829 CAD in 2025. People in this tax bracket would also pay 33% taxes at the federal level. This means individual high earners in Canada pay a marginal tax rate of 53.50%. The highest marginal tax rate in the US appears to be in New York City, where high earners may pay a marginal rate of 49.8%.

What’s a Marginal Tax Rate?

A marginal tax rate is the rate you pay on each additional dollar of income you earn. In a progressive tax system, each “slice” of your income is taxed at a different rate, and the marginal rate applies to the top “slice.” For example, if you fall into a bracket that taxes income over $50,000 at 25%, you would pay 25% only on the portion of your income above $50,000.

What’s an Average Tax Rate?

An average tax rate, on the other hand, reflects the overall percentage of your total income that goes toward taxes. You arrive at it by dividing the total amount of taxes you pay by your total income. This rate is always lower than your marginal rate in a progressive tax system because some of your income is taxed at lower rates in the lower brackets.

So, Do Canadians Pay More Income Taxes Than Americans Overall?

This doesn’t mean that every Canadian pays more income taxes than every American. In fact, in many provinces, income taxes for average earnings look fairly similar to taxes in certain US states.

The exception being those who live in the states in the US that do not charge an income tax. Canada does not have any provinces or territories that do not require residents to pay income taxes.

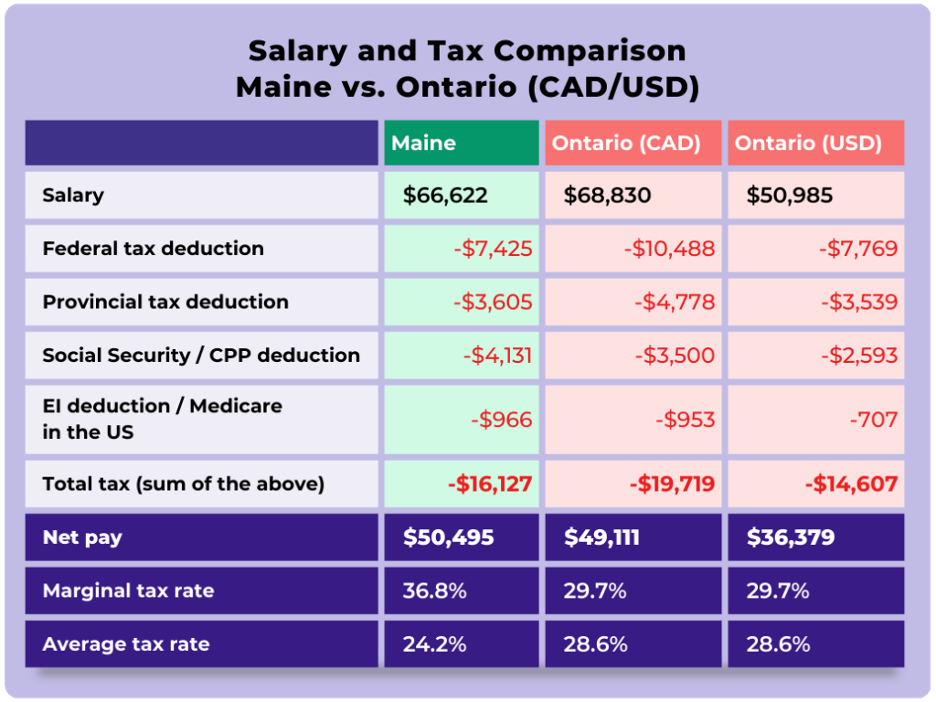

Let’s take a look at a hypothetical person considering moving from Maine in the USA to Ontario, Canada:

| Maine (Average in US) | Ontario (CAD) (Average in Canada) | Ontario (USD Conversion) | |

|---|---|---|---|

| Salary | $66,622 | $68,830 | $50,985 |

| Federal tax deduction | -$7,425 | -$10,488 | -$7,769 |

| Provincial tax deduction | -$3,605 | -$4,778 | -$3,539 |

| Social Security/CPP deduction | -$4,131 | -$3,500 | -$2,593 |

| EI deduction / Medicare in the US | -$966 | -$953 | -$707 |

| Total tax (sum of above) | -$16,127 | -$19,719 | -$14,607 |

| Net pay | * $50,495 | $49,111 | $36,379 |

| Marginal tax rate | 36.80% | 29.70% | 29.70% |

| Average tax rate | 24.20% | 28.60% | 28.60% |

The table above shows publicly available government data as of January 2025 and is subject to change.

It’s worth remembering that Canada’s universal public healthcare system is largely funded at the provincial level in Canada – with around 78% of healthcare being funded at the provincial level, mostly through taxes.

So, while this person pays more provincial taxes, they can access the publicly-funded healthcare system in Canada, and health insurance is optional and less expensive than in the US.

And if they have children, they may feel a real return on their taxes through subsidised childcare facilities and the Canada child benefit, among other benefits, payments, and credits.

It’s also interesting digging into Employment Insurance a little more deeply. While employers in the US pay the unemployment tax, Canada’s system is much more robust. Workers are entitled to up to 66% of their earnings if they’re laid off or fired without cause, assuming they meet certain eligibility requirements. Canada’s parental leave is also a standout compared to the US. In the US, there’s no paid leave entitlement from the government. In Canada, the birth parent is entitled to up to 15 weeks of paid maternity leave, and then there’s paid parental leave of up to 40 weeks, which can be shared between the parents. These periods of leave vary in the province of Quebec, where paternity leave is distinct from maternity and parental leave, and where the percentage of earnings paid out is higher than in the rest of Canada (but income taxes are higher too).

Interested in Moving To Canada from the US? Consider Scotiabank

Getting started in Canada may not always be easy, but figuring out your finances and navigating the Canadian banking system should be.

Scotiabank’s StartRight® program simplifies your banking in Canada. It offers banking services and products designed for you, plus you can get up to $2,300* in value the first year as a newcomer including up to $580 with StartRightTM.

Scotiabank is committed to helping to ease the financial challenges newcomers like you face when you move to Canada. We do that by providing solutions and advice to help you achieve your financial goals – including credit products that don’t exclude you just because you don’t have a credit score in Canada yet.

Ready to get your finances on track for your future? Come in and speak to a Scotiabank advisor.

Legal Disclaimer

About the author