Updated on May 6, 2026

This content is sponsored by Scotiabank. The views, opinions, and information expressed in this piece are those of Moving2Canada and do not reflect those of Scotiabank. Scotiabank is not responsible for the content, accuracy, or any representations made herein.

From getting your first bank account to navigating high rental costs to working towards retirement, newcomers have a lot to learn when it comes to managing finances in Canada. But with the right information and a plan, you can thrive financially.

Preparing For The Cost Of Living In Canada

Planning for the costs of living is one of the most important tasks to do before you arrive in Canada. Many areas of Canada are expensive to live in – some of the most expensive cities in the world are in Canada. Since the costs of living can be high, you need to research, plan and save in advance.

Your Emergency Fund

An emergency fund is money that’s set aside in case of financial hardship (like losing a job) or to cover unforeseen expenses. It is essential for your move to Canada, since you’ll be adjusting to a new life in a new place, and you won’t want to be under extra financial stress in this transition period. It can also help you avoid unmanageable debt levels and help you achieve your goals faster in Canada.

Building An Emergency Fund

Steps you can take to increase your emergency fund before moving to Canada include:

- Create your budget and work out how much money you can set aside every month. The longer you plan for, the less money you will have to put aside each month to build your emergency fund.

- Save any bonuses, pay rises, or tax refunds directly into your emergency fund to reach your goals more quickly.

- If you need to build your fund quickly, work additional shifts or create an online side hustle (bonus: it’s possible this work can move with you to Canada).

- Sell personal items you don’t plan to bring to Canada and you won’t need to replace.

How Much Of An Emergency Fund Do You Need?

The size of your emergency fund can vary depending on your risk tolerance and personal circumstances. Those who work in stable, in-demand industries in lower cost of living areas are more likely to be secure with a three month emergency fund. Anyone who owns an older home, has children, lives in a high cost of living area, or may have trouble finding work should consider saving for six months. Given you’re moving to a new country (with a new economy and potentially higher costs of living), it’s often best to plan for a six month emergency fund during your move.

For reference, here’s what a ballpark six month emergency fund looks like on average in Canada in 2024:

Emergency fund for a single person: $17,100 (with rent of $1,400 monthly)

Emergency fund for a family of four: $44,500 (with rent of $2,200 monthly)

If you plan on living in Vancouver, Toronto, or other high cost of living areas, you may want to save more than this.

Pre-Arrival Financial Success Checklist

- Research immigration costs, the cost of living in your planned destination in Canada, and learn about your job prospects/wage growth.

- Set a budget for your move to Canada. Scotiabank’s Money Finder is a great option for this.

- Save enough money for your move to Canada plus at least three months living expenses (ideally six months).

- Explore pre-arrival bank accounts before you arrive in Canada.

- Learn more about transferring money internationally from your home country to Canada through Scotiabank.

There are three distinct stages in the newcomer journey, each with their own financial milestones. We will dig into each stage and share checklists identifying exactly what you need as you find your financial feet in Canada.

- If you want more information about the top five banking challenges in Canada, start here.

The Three Financial Stages In The Newcomer Journey

- Pre-Arrival: Research, Budgeting, and Saving.

- Settling In: Establish Your Financial Foundations.

- Wealth Building: Grow Financial Security In Your New Home.

Let’s learn more about each stage:

Pre-Arrival: Research, Budgeting, and Saving

Every newcomer’s journey before arriving in Canada looks different. Some plan for months or even years to come to Canada. Others are offered a job and moved quite quickly. Whatever your pre-arrival plan looks like, it’s important to give plenty of careful thought to your finances before you move.

There’s a lot to manage at the pre-arrival stage: immigration, saving for your move, choosing where to live, learning about Canada’s banking system, and understanding the costs of living to start.

Want to get a head start on budgeting? Moving2Canada’s Budget Calculator is an interactive budgeting tool that helps you plan for Canada’s cost of living.

Settling In: Establish Your Financial Foundations

You’ve landed in Canada, found a home to rent, and you’ve started working. Now it’s time to establish your financial foundations and start working towards your dream life in Canada.

There are two major components in establishing your financial foundations: one is to master the basics, the other is to start dreaming about your future.

In terms of the basics, opening a bank account, getting a regular paycheck, and saving up for your first few milestones in Canada is a great start. But learning to flex your budgeting muscles are key for long-term financial success.

The 50-30-20 framework is a simple method of managing your money at (almost) any income level. This framework says that you should spend 50% of your take home pay on ‘needs’, 30% on wants, and 20% on savings and investments.

Keep in mind that this is just a framework; there are several budgeting methods we recommend for newcomers, and you can easily modify it to fit your current situation.For example, if you have large expenses coming up (such as paying an immigration consultant or lawyer) or if you want to save more aggressively for a house or retirement, you can bump up the savings and investments to 30% for a time.

Financial Foundations Checklist: Settling In Canada

Here are the checklist items many newcomers work towards in their first year in Canada:

- Open a bank account in your first week in Canada.

- Receive your first paycheck.

- Get a credit card to start building your credit history.

- Buy your first vehicle.

- Rent your first home.

- Buy your first insurance policies. You may need auto insurance, tenant insurance, and potentially life, disability and/or critical illness insurance.

- Build and maintain a three-to-six-month emergency fund.

- Start learning about Canada’s tax-advantaged accounts.

Start Living Your Dream

Your first years in Canada should also include time spent reflecting on how far you’ve come and where you want to go, financially speaking. Ask yourself (and your partner or family, if you have one) what your ideal future looks like and whether your finances are helping you achieve your dreams:

- Have you established a budget you can stick to?

- What level of savings makes you feel most secure? Do you prefer a three month emergency fund or does a six month fund help you feel safe?

- Are you building your credit score and developing a credit history?

- Are you managing your debt effectively and responsibly?

- Do you want to own a home in the future? If so, where is it located and what type of home is it? What does your savings plan look like for the down payment?

- Is your current job meeting your financial needs? If not, what needs to be true for you to earn more?

- Would consulting with a financial advisor make sense at this point?

Wealth Building: Grow Financial Security In Your New Home

At the wealth building stage, you’ve likely been in Canada for a year or more (though it could be a shorter period of time if you started working professionally shortly after arriving). You’ve learned a little about tax-advantaged accounts in Canada, like a TFSA, RRSP, and/or FHSA. Perhaps you’ve even opened these accounts yourself.

Wealth Building Toolkit

The wealth building stage is all about putting your income in the right place to earn and grow while you save for your goals.

- Buy adequate insurance.

- Understand Canada’s tax-advantaged accounts.

- Save a down payment for your first home in Canada.

- Plan and start saving for your retirement.

- Start saving for your child’s education.

It’s important at this stage to have a clear understanding of your goals, and your family’s goals (if applicable). You will need to balance the power of compounding interest on a secure retirement against your goal of owning a home in the near term.

Working with a banking advisor can be beneficial at this point. Scotia advisors are available in every branch, and they can help you gain confidence, plan for the future, and remain on track for your financial goals.

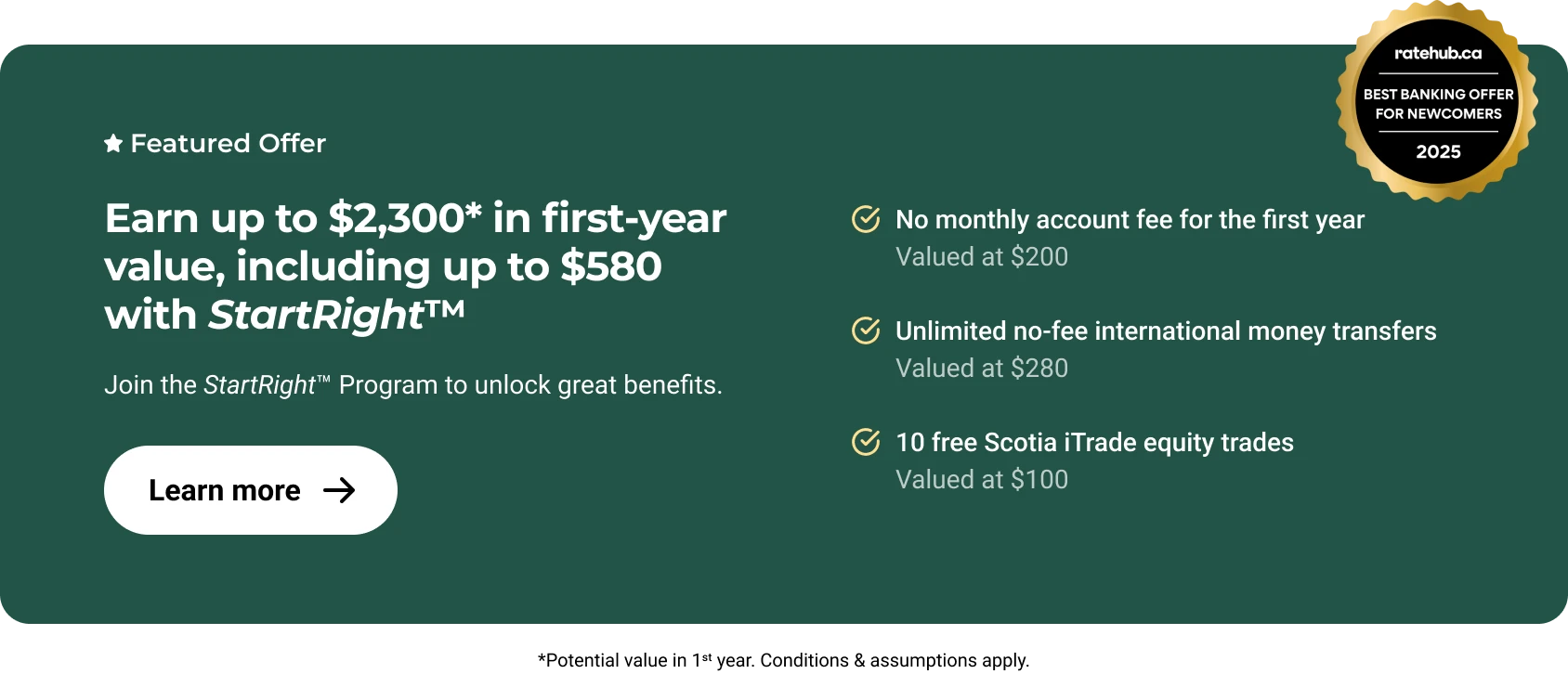

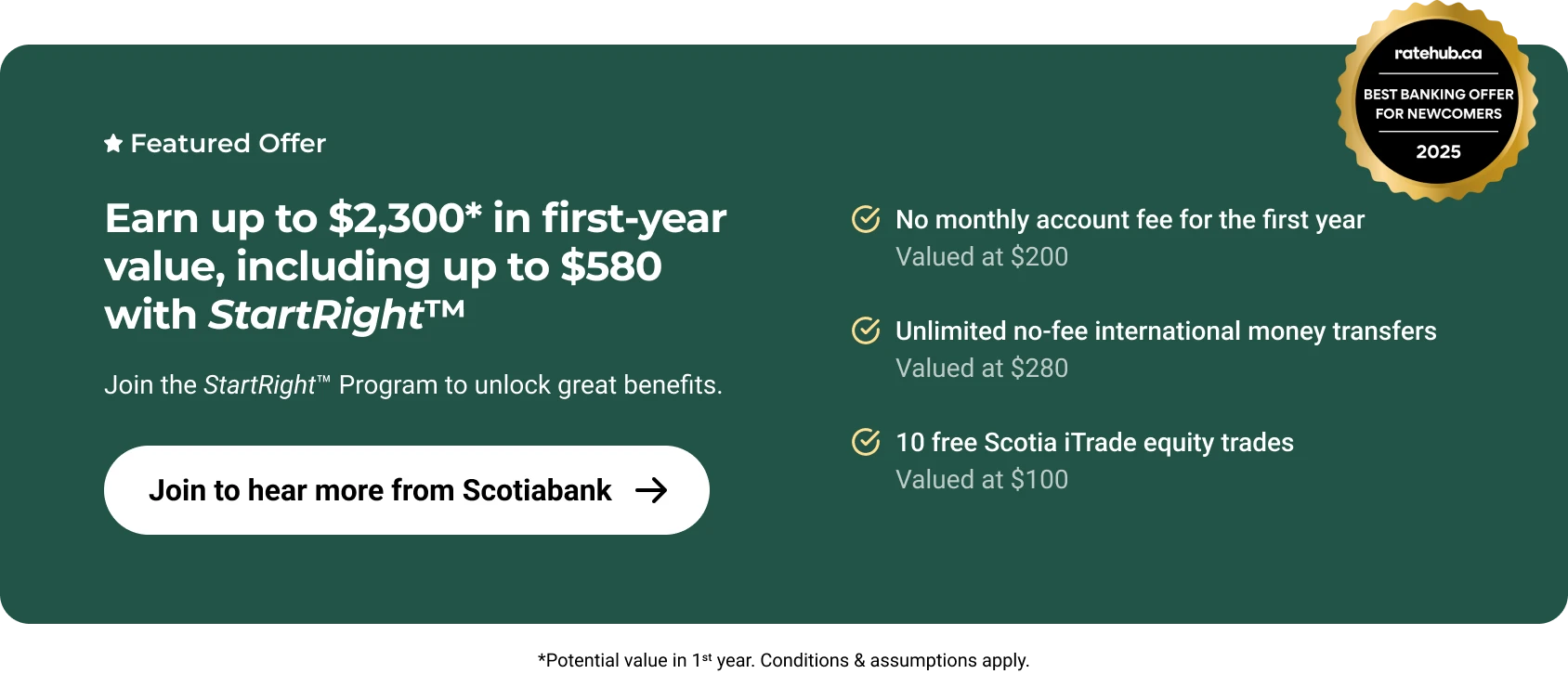

StartRightTM With Scotiabank

Scotiabank is here to support you through your journey. From understanding banking basics, finding the right advisor, setting financial goals and more — the StartRightTM Program will help make banking in Canada easier.

Scotiabank provides banking packages and products suitable for newcomers. Newcomers can also receive access to credit, no-fee international money transfers, and tailored guidance from Scotiabank Advisors as part of the StartRightTM Program.

Learn more about banking with Scotiabank

Related articles

New Canada Child Benefit Payment Arrives July 20. How Much Will Families Receive?

Read more

New Canada Groceries and Essentials Benefit (CGEB) Payments Start July 3. Who Qualifies?

Read more

CRA Benefit Payments Coming in July 2026: What Newcomers Could Get

Read more

Next BoC Interest Rate Decision on June 10 as Canada Enters Technical Recession

Read more

About the author