Updated on July 18, 2026

This content is sponsored by Scotiabank. The views, opinions, and information expressed in this piece are those of Moving2Canada and do not reflect those of Scotiabank. Scotiabank is not responsible for the content, accuracy, or any representations made herein.

Saving for long-term financial goals and your retirement can take serious discipline over a long period of time. To successfully save for your future, you’ll need to take some time to understand the Canadian landscape.

This post, which is the third in our three-part savings series, walks you through the ins and outs of long-term wealth building and saving for your retirement.

Key Takeaways

- Part one of this series highlights the savings hierarchy, and the types of accounts you’ll likely use across the various stages of saving.

- Part two discusses how you can save to build financial security in Canada.

- This piece, part three, explains some important concepts to help you build long-term wealth and a retirement plan.

- This Scotiabank Advice+ piece covering How to save and invest when you’re new to Canada is a can’t miss resource on this topic.

How to Build Wealth for Your Future, including Retirement

The old adage ‘slow and steady wins the race’ can be applied for building wealth over time and saving for retirement. Building up your retirement savings may feel like a huge task, so chipping away at it over a longer time can make it more manageable.

One element of saving for your retirement over time that you might consider is investing. There are many different ways to invest, including real-estate or buying any of the many types of investment products. Some of the various types of investment products you might consider for your retirement because of the longer-term timespan include (but aren’t limited to) mutual funds, Guaranteed Investment Certificates (GICs), or Exchange Traded Funds (ETFs).

Benefits of Investing

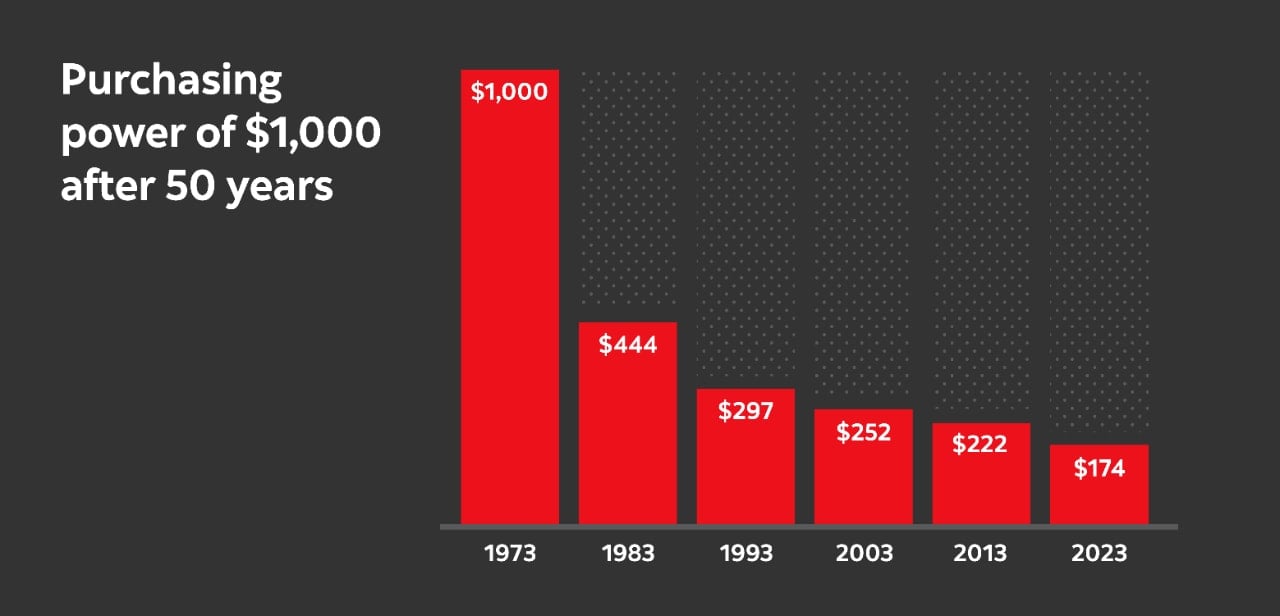

Inflation refers to rising prices over time for goods and services, which can erode the purchasing power of money. The graphic below shows how $1,000 in 1973 would buy just $174 worth of goods or services in 2023. It’s based on data from Statistics Canada, using the Core Canadian Consumer Price Index from December 31, 1973 to December 31, 2023.

For illustrative purposes only. From the Scotiabank Advice+ article Inflation vs Deflation: What’s the difference?

One of the potential benefits of investing is that the growth in the money you invest may outpace inflation (depending on the performance of the investments you choose over time). Investing involves risk, including the potential loss of the money you invest, though diversification may help reduce some of the risk in investing. A well-diversified portfolio of investments may also help you grow your money over time at a rate that equals or even exceeds inflation. So, you may want to work with a qualified investment advisor when investing your money.

Another benefit to investing is that you may earn extra income through interest or dividends from the investment products you buy. Some companies (but not all) share part of their profits with investors on a regular basis, in the form of dividends. Similarly, you may receive interest payments if you purchase a GIC.

How Much Money Should I Have Saved By Age 30? Or 40? Or 50?

As a newcomer to Canada, you’ve likely had some major financial milestones to pay for – your immigration application, an international move, and perhaps international tuition. Plus, you’ve possibly worked in some lower-paying roles during your studies or your first few years in Canada.

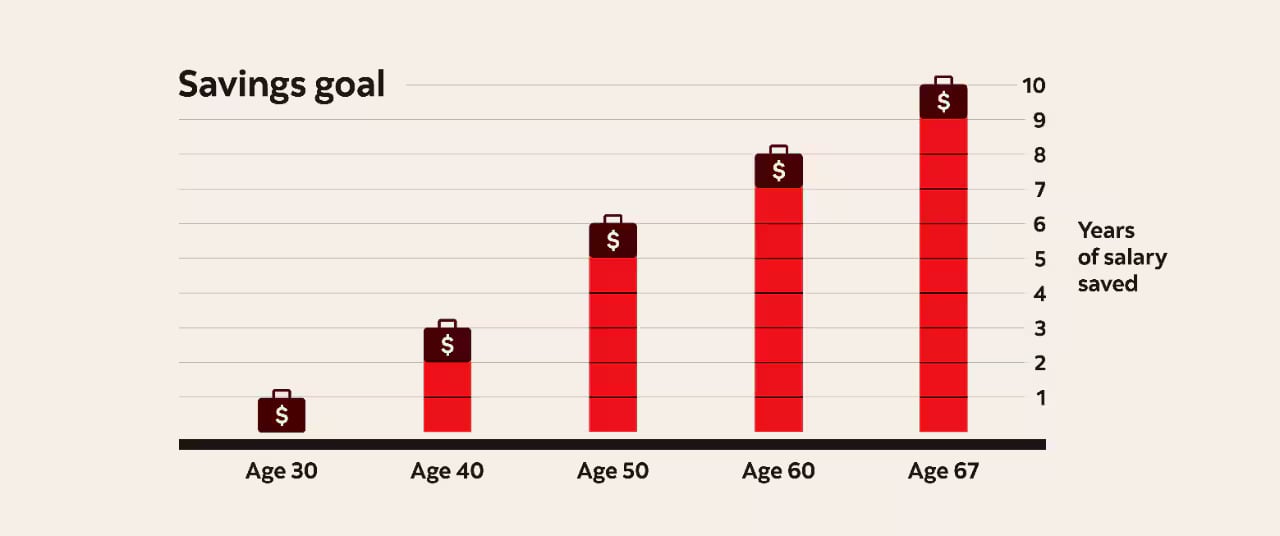

With that said, here are some broad goals for retirement savings amounts across age groups:

- By age 30: 1 year of your salary

- By age 40: 3 years of salary

- By age 50: 6 years of salary

- By age 60: 8 years of salary

- By age 67: 10 years of salary

This graphic is from Scotiabank’s Advice+ article How much should I have in savings?

Planning For Your Retirement Can Be Powerful

Now you know some ‘averages’ and ‘benchmarks’ for retirement saving, we’re going to let you in on the real secret sauce behind saving for retirement — a personalized plan.

A plan that considers how much you and your family will need and what it takes to get there can help you build your retirement savings over time. However, actually building that personalized plan can be quite a complex task.

For one thing, inflation over time means that the money you save today may be worth less in the future. So, it can be tricky to estimate exactly how much money you will need each year during retirement.

Then, there’s the challenge of knowing what your living costs and lifestyle expenses will look like in the future.

But, there are some tools and rules that can help you and some questions to ask yourself to work out how much you need to retire.

Questions to Ask Yourself About Your Retirement

One important question you can ask yourself about your retirement is “how can I start saving for my retirement today”.

Then, you should consider which accounts best suit your goals for retirement. In Canada, there are tax-advantaged accounts that can be helpful. A TFSA, for example, lets you set aside a certain amount of money each year for tax-free growth, while a RRSP offers a tax deduction today and tax-free growth on funds while they’re in the account.

It’s also important to think about what you want your lifestyle to look like in retirement. As a starting point, there’s a general rule of thumb that says to aim for around 70% of your pre-retirement income. But it’s important to think about your personal needs, so you can save the right amount for your unique situation.

Here are some questions to ask yourself:

- At what age do I want to retire? Is this realistic?

- Will I receive any income in retirement (from a workplace pension, the Canada Pension Plan, Old Age Security, my investments, a side hustle, part-time, employment, or an investment property)?

- Where do I want to live in retirement? And, if I own that property, will I owe any money on it?

- What might my monthly expenses look like?

- What major expenses will I have in retirement? (Education expenses for yourself or other family members, major home repairs or a renovation, etc.)

- Do I want to travel or buy luxury goods? If so, how often?

- Will I need to financially support anyone in your retirement? (A partner, a disabled or dependent relative, etc.)

With those answers in mind, you can use Scotiabank’s retirement savings calculator tool as a starting point for planning how much you may need (in today’s dollars) to retire.

Preparing for retirement must also include a plan for your health in retirement. We have prepared a full article about this planning here: “What Are Your Options for Health Insurance in Retirement?”

When To Get Professional Help Developing Your Retirement Plan

As you can tell, planning for retirement is no small feat. There are so many moving parts, it can feel overwhelming. It can also feel stressful to not know whether you’re on the right path, and what else you could be doing to build a brighter financial future.

If you feel uncertain about your retirement or you’d like professional guidance to make sure you’re on the right path, speaking with an advisor can help.

A Scotiabank Advisor can build a customized financial plan suited to your retirement goals. Plus, they’re there for the long term to help you build a financial plan that evolves with you.

Legal

About the author